[Under Section 45ZL of the Reserve Bank of India Act, 1934] The eighth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the amended Reserve Bank of India Act, 1934, was held on December 5 and 6, 2017 at the Reserve Bank of India, Mumbai. 2. The meeting was attended by all the members - Dr. Chetan Ghate, Professor, Indian Statistical Institute; Dr. Pami Dua, Director, Delhi School of Economics; Dr. Ravindra H. Dholakia, Professor, Indian Institute of Management, Ahmedabad; Dr. Michael Debabrata Patra, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Viral V. Acharya, Deputy Governor in charge of monetary policy - and was chaired by Dr. Urjit R. Patel, Governor. 3. According to Section 45ZL of the amended Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:– -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation at its meeting today, the Monetary Policy Committee (MPC) decided to: - keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.0 per cent.

Consequently, the reverse repo rate under the LAF remains at 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 6.25 per cent. The decision of the MPC is consistent with a neutral stance of monetary policy in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment 6. Since the last meeting of the MPC in October 2017, global economic activity has been gaining momentum through the final quarter of the year, driven mainly by advanced economies (AEs). US growth remained largely resilient to hurricanes and grew at the highest pace in the past three years in Q3 of 2017, with positive contributions from private consumption, investment activity and net exports. The unemployment rate fell to 4.1 per cent in October, the lowest in the last 17 years. In the Euro area, economic activity expanded, underpinned by accommodative monetary policy and strong job gains. The Japanese economy also continued to grow in Q3, largely supported by external demand, which helped compensate for the slowing of domestic consumption. 7. Among major emerging market economies (EMEs), the services sector remained the main driver of growth in China in Q3. However, weakness in real estate and construction activity remained a drag on growth. In Brazil, incoming data suggest that the recovery gained further momentum in Q3, with unemployment touching an intra-year low in September. Business and consumer confidence rose in October. Economic activity in Russia moderated in Q3 due to weakness in industrial production. The South African economy continued to face headwinds from weak manufacturing activity, elevated levels of unemployment and political instability. 8. The latest assessment by the World Trade Organisation (WTO) for Q4 indicates a loss of momentum in global trade due to declining export orders. Crude oil prices touched a two-and-a-half-year high in early November on account of the Organisation of the Petroleum Exporting Countries’ (OPEC) efforts to rebalance the market. Bullion prices have been under some selling pressure on account of the rising US dollar. Weak non-oil commodity prices and subdued wage dynamics have kept inflation contained in many AEs, while the inflation scenario remains diverse in major EMEs. 9. Global financial markets have remained buoyant, reflecting the improving economic outlook and the gradual normalisation of monetary policy by the US Fed. Equity markets have gained on improved corporate earnings and anticipation of large tax cuts in the US. Although equity markets have made gains in EMEs in general, they faced risk aversion in some economies. While bond yields in most AEs have moved sideways in the absence of inflation pressures, they have risen across most EMEs on country-specific factors. In currency markets, the US dollar has gained, while the surge in the euro on positive economic data lost some momentum in November due to political uncertainty. Several emerging market currencies weakened due to domestic factors. Capital inflows to EMEs have been differentiating among countries, based on investor perceptions of risk-return trade-offs. 10. On the domestic front, the growth of real gross value added (GVA) accelerated sequentially in Q2 of 2017-18, after five consecutive quarters of deceleration. It was powered by a sharp acceleration in industrial activity. All the three sub-sectors of industry registered higher growth. GVA growth in the manufacturing sector – the key component of industry – accelerated sharply on improved demand and re-stocking post goods and services tax (GST) implementation. The mining sector expanded in Q2 due to higher coal and natural gas production. GVA growth in the electricity, gas, water supply and other utility services sector also strengthened on higher demand. In contrast, growth in agriculture and allied activities slackened, reflecting the lower than expected kharif harvest. Activity in the services sector decelerated, mainly on account of slowdown in financial, insurance, real estate and professional services, and in public administration, defence and other services (PADO) following the large front-loading of government expenditure in Q1. Despite some improvement, construction sector growth remained tepid due to transitory effects of the RERA and GST implementation. Growth in the trade, hotels, transport and communication sub-group remained resilient, in spite of some slowdown in growth in Q2 as compared with the previous quarter. On the expenditure side, the growth of gross fixed capital formation improved for the second successive quarter. However, growth in private final consumption expenditure – the mainstay of aggregate demand – slowed to an eight-quarter low in Q2. 11. Looking beyond Q2, rabi sowing in Q3 has so far been marginally lagging behind the acreage sown during the comparable period of the previous year. Precipitation since October has remained at around 13 per cent below the long period average (LPA). Major reservoirs, the main source of irrigation during the rabi season, were at 64 per cent of the full reservoir level vis-a-vis 67 per cent in the previous year. On the positive side, pulses sowing increased significantly as compared with a year ago, partly reflecting the impact of lifting of the export ban for all varieties of pulses. 12. Available high-frequency indicators suggest a mixed picture of industrial activity for Q3. Core industries’ growth was flat in October as all constituents barring steel and fertilisers slowed down sequentially. Coal mining, which revived strongly in Q2, slowed down too, while cement production contracted. In contrast, the Purchasing Managers’ Index (PMI) for manufacturing, which fell in October, rebounded in November, driven by output and new orders. Also, according to the Reserve Bank’s Industrial Outlook Survey (IOS), production is expected to pick up in Q3 as order books are rising. 13. Services sector activity has remained mixed in October. In the transportation sector, sales of commercial vehicles decelerated; those of passenger vehicles and two-wheeler turned into contraction mode. By contrast, domestic and international air passenger and freight traffic, and railway freight expanded robustly. The Reserve Bank’s survey suggests that sentiments on service sector activity for Q3 are upbeat and auto sales have rebounded in November. On the other hand, PMI for services moved into contraction zone in November. 14. Retail inflation measured by year-on-year change in the consumer price index (CPI) recorded a seven-month high in October, driven by a sharp uptick in momentum, tempered partly by some favourable base effects. Food inflation was volatile in the last two months – declining sharply in September and bouncing back in October – due mainly to vegetables and fruits. Milk and eggs inflation has shown an uptick, while pulses inflation remained negative for the eleventh successive month in October. Cereal inflation remained stable. Fuel group inflation, which has been on an upward trajectory since July, accelerated further due to a sharp pick-up in inflation in liquefied petroleum gas (LPG), kerosene, coke and electricity. 15. CPI inflation excluding food and fuel, which increased from July to September, remained steady in October. This reflected the softening of petroleum product prices on account of the reversal of taxes on petroleum products by the central and state governments. However, there was a hardening of housing inflation following the implementation of higher house rent allowances for central government employees under the 7th central pay commission award. 16. The Reserve Bank’s survey of households showed inflation expectations firming up in the latest round for both three months ahead and one year ahead horizons. Farm and industrial raw material costs rose in October. Firms responding to the Reserve Bank’s Industrial Outlook Survey expect to pass on the increase in input prices to their output prices. Turning to other costs, wage growth in the organised sector edged up, while rural wage growth weakened, particularly in agriculture. 17. Surplus liquidity in the system has continued to decline during October and November. Currency in circulation increased by ₹736 billion in Q3 (up to December 1, 2017) over end-September on festival demand. The Reserve Bank managed surplus liquidity through the conduct of regular variable rate reverse repo auctions of various tenors, ranging from overnight to 28 days. Net average daily absorption of liquidity under the LAF declined from ₹2,229 billion in September to ₹1,400 billion in October 2017 and further to ₹718 billion in November. The Reserve Bank conducted open market sales of ₹300 billion in October-November, taking the total absorption of durable liquidity during the financial year so far to ₹1.9 trillion, comprising ₹900 billion in the form of open market sales and ₹1 trillion of long-term treasury bills under the market stabilisation scheme. The weighted average call rate (WACR) traded 12 bps and 15 bps below the repo rate during October and November, respectively, as against 13 bps in September. 18. Merchandise exports declined by 1.1 per cent in October 2017 after showing positive growth for 14 consecutive months. A sustained increase in exports of engineering goods, petroleum products and chemicals during the month was outweighed by a sharp fall in shipments of gems and jewellery, ready-made garments, and drugs and pharmaceuticals. Imports continued to expand, though at a modest pace. Although gold imports rose sequentially in October, they moderated from their level a year ago. Consequently, the trade deficit widened again in October. Despite moderation in September, net foreign direct investment in H1 of 2017-18 was at the same level as a year ago. With the announcement of the recapitalisation plan for public sector banks, foreign portfolio inflows into equities resumed sharply in October, after recording outflows in the preceding month. India’s foreign exchange reserves were at US$ 401.94 billion on November 30, 2017. Outlook 19. The October bi-monthly statement projected inflation to rise and range between 4.2-4.6 per cent in the second half of this year, including the impact of increase in house rent allowance (HRA) by the Centre. The headline inflation outcomes have evolved broadly in line with projections. Going forward, the inflation path will be influenced by several factors. First, moderation in inflation excluding food and fuel observed in Q1 of 2017-18 has, by and large, reversed. There is a risk that this upward trajectory may continue in the near-term. Second, the impact of HRA by the Central Government is expected to peak in December. The staggered impact of HRA increases by various state governments may push up housing inflation further in 2018, with attendant second order effects. Third, the recent rise in international crude oil prices may sustain, especially on account of the OPEC’s decision to maintain production cuts through next year. In such a scenario, any adverse supply shock due to geo-political developments could push up prices even further. Despite recent increase in prices of vegetables, some seasonal moderation is expected in near months as winter arrivals kick in. Prices of pulses have continued to show a downward bias. The GST Council in its last meeting has brought several retail goods and services to lower tax brackets, which should translate into lower retail prices, going forward. On the whole, inflation is estimated in the range 4.3-4.7 per cent in Q3 and Q4 of this year, including the HRA effect of up to 35 basis points, with risks evenly balanced (Chart 1). 20. Turning to GVA projections, Q2 growth was lower than that projected in the October resolution. The recent increase in oil prices may have a negative impact on margins of firms and GVA growth. Shortfalls in kharif production and rabi sowing pose downside risks to the outlook for agriculture. On the positive side, there has been some pick up in credit growth in recent months. Recapitalisation of public sector banks may help improve credit flows further. While there has been weakness in some components of the services sector such as real estate, the Reserve Bank’s survey indicates that the services and infrastructure sectors are expecting an improvement in demand, financial conditions and the overall business situation in Q4. Taking into account the above factors, the projection of real GVA growth for 2017-18 of the October resolution at 6.7 per cent has been retained, with risks evenly balanced (Chart 2).

21. The MPC notes that the evolving trajectory needs to be carefully monitored. First, two of the key factors determining the cost of living conditions and inflation expectations, i.e., food and fuel inflation, edged up in November. Inflation expectations of households surveyed by the Reserve Bank have already firmed up and any increase in food and fuel prices may further harden these expectations. Second, rising input cost conditions as reflected in various surveys point towards higher risk of pass-through to retail prices in the near term. Third, implementation of farm loan waivers by select states, partial roll back of excise duty and VAT in the case of petroleum products, and decrease in revenue on account of reduction in GST rates for several goods and services may result in fiscal slippage with attendant implications for inflation. Fourth, global financial instability on account of the pace of/uncertainty over monetary policy normalisation in AEs and fiscal expansion in the US carry risks for inflation. The expected seasonal moderation in prices of vegetables, and fruits and the recent lowering of tax rates by the GST Council could mitigate upside pressures. Accordingly, the MPC decided to keep the policy repo rate on hold. However, keeping in mind the output gap dynamics, the MPC decided to continue with the neutral stance and watch the incoming data carefully. The MPC remains committed to keeping headline inflation close to 4 per cent on a durable basis. 22. In the MPC’s assessment, there have been several significant developments in the recent period which augur well for growth prospects, going forward. First, capital raised from the primary capital market has increased significantly after several years of sluggish activity. As the capital raised is deployed to set up new projects, it will add to demand in the short run and boost the growth potential of the economy over the medium-term. Second, the improvement in the ease of doing business ranking should help sustain foreign direct investment in the economy. Third, large distressed borrowers are being referenced to the insolvency and bankruptcy code (IBC) and public sector banks are being recapitalised, which should enhance allocative efficiency. However, the MPC notes that the impact of these factors can be buttressed by reducing the cost of domestic borrowings through improved transmission by banks of past monetary policy changes on outstanding loans. 23. Dr. Chetan Ghate, Dr. Pami Dua, Dr. Michael Debabrata Patra, Dr. Viral V. Acharya and Dr. Urjit R. Patel were in favour of the monetary policy decision, while Dr. Ravindra H. Dholakia voted for a policy rate reduction of 25 basis points. The minutes of the MPC’s meeting will be published by December 20, 2017. 24. The next meeting of the MPC is scheduled on February 6 and 7, 2018. Voting on the Resolution to keep the policy repo rate unchanged at 6.0 per cent | Dr. Chetan Ghate | Yes | | Dr. Pami Dua | Yes | | Dr. Ravindra H. Dholakia | No | | Dr. Michael Debabrata Patra | Yes | | Dr. Viral V. Acharya | Yes | | Dr. Urjit R. Patel | Yes | Statement by Dr. Chetan Ghate 25. Since the last review, headline inflation has inched up to 3.6 per cent. RBI’s quarterly projections of CPI inflation (including HRA) are based on crude prices being US $ 60 per barrel. Uncertainty because of geopolitical events could push up the price of crude higher than this value. As the Phillips Curve for the economy shifts up because of increases in crude prices, this poses an upside risk to the medium term inflation target of 4 per cent. 26. The increase in the wheat MSP by the government in October was the biggest increase in the past five years (both in absolute terms as well as percentage terms). My own research (with co-authors) shows how such procurement “shocks” can lead to a wage-price spiral ending up in generalized inflation. Separately, using the KLEMS database, I find that average annual total factor productivity (TFP) growth in agriculture in India between 1980 to 2011 is close to 1 per cent, with a very mild upward sloping (HP filtered) trend throughout the period. Stagnant agricultural productivity combined with a lopsided temporal distribution of rain like last year makes the agriculture sector continually vulnerable to price pressures that need to be carefully watched. Having said this, I am comforted by the fact that cereal inflation is lower with favourable base effects going forward. Kharif rice production is also consistent with production in the last five years. Pulses continue to face deflationary pressures, although base effects will be unfavourable in coming months. I see the 3-month and 1-year ahead inflationary expectations as stable but with an uptick. With the coming winter season, there will possibly be the usual seasonal moderation in vegetables. Inflation, excluding food, fuel, and housing till date is constant around 4.1 per cent which is somewhat comforting. 27. Compared to the last review, various risks are materializing around inflation becoming generalized and need to be watched carefully. The positive co-movement between the output gap and inflation excluding food and fuel since 2010-11 suggests that a closing output gap will generate demand-pull pressures on inflation as growth revives. The conquest of Indian inflation is certainly not a done deal! 28. As I mentioned in my last review, the weakness in growth drivers continues to worry me. While both GVA and GDP growth rebounded after sequential declines over the last 5 quarters, the growth revival lacks animal spirits. Consumption, the main stay of the Indian economy, at 54 per cent, exhibits a declining share of GDP. Consumer confidence is the lowest since September 2013. There has been a reversal of the commodity price cycle. Investment demand continues to be muted, despite a recent uptick in Q2 of 2017-18. While merchandise exports are likely to see a sustained recovery as GST disruptions fade, exports are far too volatile to be a reliable source of aggregate demand in the short term. The November 2017 PMI in services also turned into contraction mode. Various factors however bode well for the growth process (GST, favourable impact of global growth, incipient turn around in credit growth, pay commission, and bank recapitalization). More certainty on growth trends will be available in the next couple of months after the release of Advance GDP Estimates and the Union Budget, making it prudent to wait and watch. 29. Taking these considerations into account, I vote for a pause in the policy repo rate at today’s meeting of the Monetary Policy Committee. Statement by Dr. Pami Dua 30. Inflation as measured by the CPI recorded an uptick since the previous meeting of the MPC in early October 2017. This rise was driven by higher food inflation (mainly vegetables and fruits) and fuel prices. The effect of an increase in House Rent Allowance and the lingering impact of the goods and services tax (GST) also contributed towards the pressure on inflation. CPI inflation excluding food and fuel remained steady at 4.6 per cent. 31. Going forward, upside risks include expectations of high international prices of crude oil due to OPEC’s accord to extend production cuts till December 2018. The impact of House Rent Allowance and likely fiscal slippages may also continue to push inflation up. The seasonal decline in vegetable prices (especially onions and tomatoes) has also not yet materialised due to supply disruptions. Global financial instability on account of monetary policy normalisation in advanced economies also implies risks to inflation. Further, the latest round of RBI’s Households Inflation Expectations Survey shows inflation expectations firming up for both three-month- and one-year-ahead horizons. The Reserve Bank’s Industrial Outlook Survey shows that firms expect to pass on the increase in input prices to output prices. Offsetting factors include the reduction in GST rate of several commodities and services that may translate into lower retail prices for consumers, a more proactive supply management by the government, and a downward trend in prices of pulses. 32. India’s GVA growth accelerated in Q2 2017-18 after five consecutive quarters of slowing down. Although agriculture and services decelerated, there was a rebound in industrial activity, partly due to restocking after GST implementation. 33. Going forward, the Reserve Bank’s surveys indicate that performance in the services and infrastructure sectors is expected to improve in Q4 on account of increase in demand, financial conditions and the overall business situation. Further, recapitalization of public sector banks may help in sustaining the renewed credit flows. The recent reduction in GST rates may also provide a boost to the economy. The improvement in the ranking related to the ease of doing business may also provide an impetus to growth. In the coming months, downside risks to growth may arise from lower than projected sowing in the rabi season. Another major factor may be the recent increase in oil prices that will put pressure on margins of firms. The Consumer Confidence Survey conducted by RBI indicates deterioration in the outlook for the general economic situation and the employment scenario. 34. Furthermore, growth in the Economic Cycle Research Institute’s Indian Leading Index, a predictor of future economic activity, has been lacklustre in recent months. 35. Thus, in the current scenario, a wait and watch strategy is recommended, with continuous monitoring of data. Hence, I vote for status quo in the policy rate and maintenance of the neutral stance. Statement by Dr. Ravindra H. Dholakia 36. I am not in agreement with the assessment of the RBI for both the CPI inflation and the economic growth prospects in the near term. I also do not share its over-concerns for the upside risks on inflation and over-optimism on economic growth front. In my opinion, the inflation situation is under reasonable control and is likely to remain well within the acceptable range during the foreseeable future because after a couple of months favourable base effects will set in. The real cause of concern right now is the economic recovery and its slow pace. Fiscal space is more or less exhausted but the space for the monetary boost has fortunately been available now for a relatively long period. Had the policy rate been cut to 5.75 per cent in June 2017 as I had argued then, the economic recovery would have been far more rapid and we would have been in a much better position. Although we have missed the bus, it is still better late than never. In my opinion, we must cut the policy rate by at least 25 basis points to begin with if we want to be on conservative side, because enough space existed all along. The specific reasons for my recommendation are as follows: -

Although the recent most round of RBI’s household inflationary expectation survey shows an increase of about 60 basis points (bps) for inflation one year ahead, overall it shows a substantial decline of about 280 bps over the last year or so. A very consistent and more reliable result is obtained from the Indian Institute of Management Ahmedabad (IIMA) latest business expectation survey with more than 2100 responses that shows the headline CPI inflation expectation one year ahead to be 3.71 per cent – well below the RBI target of 4 per cent. The standard deviation for this estimate is also relatively low. Thus, inflationary expectations are very well anchored and inflation control does not seem to be a major issue in the near future, i.e. over next 6 to 12 months. -

On the other hand, the RBI surveys show that consumer confidence on income, employment and overall economic environment is very low and declining in recent times. Companies still lack the pricing power and experience squeeze in their profit margins. -

Better performing and financially sound companies according to the RBI surveys are investing more in financial assets than in physical assets. They behave more like savers than investors because the real rate of interest is too high to encourage long term investment. Even consumers would be discouraged to consume durable goods. It needs to be noted that the real rate of interest is the difference between nominal rate of interest and expected rate of inflation (and not the observed rate of inflation in the recent past). -

Despite the marginal economic recovery, the capacity utilization in Indian industry according to the RBI surveys continues to be at low level of 72 per cent indicating persistent existence of output gap. Service sector PMI is also declining and in the pessimist zone. -

The growth recovery expectation of RBI during the June-September quarter of 2017 turned out to be a substantial overstatement. As against RBI’s expectation of 6.4 per cent, the growth of real GVA during the quarter turned out to be only 6.1 per cent. Yet, the RBI has not revised its growth forecast from the earlier 6.7 percent for the year 2017-18. This implies that RBI now expects a higher growth of 7.0 and 7.8 per cent respectively in the third and fourth quarters of 2017-18. This is highly improbable to be achieved without any policy rate cut because fiscal space is practically non-existent and the conditions described in points (ii) to (iv) above are posing a big challenge. Expecting an unrealistically higher growth rates during the 3rd and 4th quarters creates a false hope of the output gap closing on its own in near future so as to continue with the policy inaction. -

On the contrary, since the recovery has been slow and the confidence low, I expect the growth during the year 2017-18 to be much lower at only 6.4 per cent, which implies a growth rate of 6.7 and 7.2 per cent respectively for the 3rd and 4th quarters. Moreover, unlike my colleagues on the MPC, I firmly believe that the output gap would not start narrowing unless the current growth rate exceeds 8 – 8.5 per cent. It means that, in my opinion, the output gap is going to expand till the middle of the next year. That, in itself, will put downward pressure on prices and neutralize several upside risks to inflation. Oil prices in my opinion are not likely to stay significantly higher than the current level for any longer time. Similarly, although the fiscal slippage is likely in percentage to GDP, it would not be substantial in absolute terms. The fiscal deficit as percentage of GDP may exceed the target because the nominal GDP would grow much slower than the assumed number (11.75 per cent) in the last budget on account of lower inflation and substantial slowdown in the real growth. However, the numerator that puts upward pressure on yield rates and prices is not likely to increase substantially in absolute terms and hence the inflationary impact would be limited. -

It is important to recognize that the RBI’s expectation about the headline inflation in the remaining two quarters of 2017-18 is in the range of 4.3 to 4.7 per cent. If we exclude the pure statistical effect of revisions in the house rent allowance by the 7th Pay Commission for the government employees, the range of the RBI forecasts of both the headline and CPI excluding food and fuel show the relevant inflation rate hovering around 3.9 to 4.3 per cent over the rest of the year. Thus, there is a clear space for the rate reduction of at least 25 bps even without considering the output gap. -

There are serious implications of keeping the real policy rate substantially higher than most other countries in the world. Currently, only eleven countries in the world have a positive real policy rate and several of them either are in some crisis or have recently emerged out of a crisis. Among the rest of the countries, India has the highest real rate. If the situation is not corrected soon, it has the potential to destabilize the financial markets at home by discouraging domestic investments and encouraging foreign investment in the debt market. It may involve substantial risks for future. On the other hand, by cutting the policy rate, the domestic corporate bond market, stock market and hence investment demand could be encouraged and growth can be accelerated to bridge the output gap. 37. Keeping all these points in mind, I vote for a 25 bps cut in the policy rate in December 2017. Statement by Dr. Michael Debabrata Patra 38. I vote for status quo. 39. All the upside risks to inflation cited in previous resolutions are materialising. Moreover, price pressures are no more confined to vegetables alone, as in previous readings; they are getting diffused across petroleum products, services (excluding housing, which is being pulled up independently by statistical effects of the house rent allowance for central government employees), and into underlying inflation. The risks of inflation getting generalised appear to have increased to a point where they could potentially overwhelm the softening effects of winter arrivals of vegetables and fruits. Projections indicate that inflation prints are likely to stay above target from here on. 40. Households’ inflation expectations have firmed up and are undermining consumer confidence. The pressure of input costs may soon force corporations to reflect them in selling prices as their margins get whittled down from absorbing these costs. Financial markets, especially the bond market segment, are scenting higher inflation in the air. The slosh of liquidity that marooned markets during the year so far is being steadily drained away by liquidity operations and a position of neutrality may emerge before the end of the financial year, abstracting maturing securities under the market stabilisation scheme and forex operations. 41. The current phase of accommodation in the monetary policy stance – reduction of the policy rate by 200 basis points - is one of the deepest barring the easing associated with the global financial crisis. Also, it has been more fully transmitted. In my view, this phase has matured; it is time now to signal its end and commence the withdrawal of accommodation, consistent with the evolving stance of liquidity management. 42. It is not that I am sanguine about growth; far from it. Rather than green shoots, my sense is that the upturn of Q2 occurred on the back of replenishment of inventories, and more incoming data are needed to tell us whether or not it is durable. The investment temper remains dormant, as evident in the persisting slump in the rate of capital formation. It awaits reforms that bite the bullet in terms of freeing up product and factor markets, removing barriers to entry and exit, and rekindling productivity and competitiveness all around. As growth regains solid ground, it could likely sustain inflation above the target. 43. The time has come for monetary policy to take guard and be ready to go on to the front foot. Statement by Dr. Viral V. Acharya 44. The global commodity cycle now seems to have turned with oil prices having also rebounded recently. This has created significant input cost pressures in the economy, which at some stage may get passed on to retail prices. Vegetable prices have also firmed up, creating uncertainty around the extent of seasonal winter moderation in prices. These factors have put headline inflation on a trajectory that will most likely cross the MPC target rate of 4 per cent rather soon and remain above the target in the medium term (even after excluding the HRA impact). 45. Oil price evolution remains a particular concern. The shale gas response notwithstanding, improving global demand appears to be playing an important role in shaping oil prices along with the extension of OPEC’s production cuts. This development poses difficult domestic policy challenges – countercyclical adjustment in cess would require fiscal balancing elsewhere, whereas lack of such adjustment would imply pressure on domestic inflation (temporarily latent, since the price pass-through at pumps has not been immediate). 46. The adverse change in overall terms of trade given the commodity cycle upturn has likely also weakened drivers of growth. Nevertheless, there has been some respite in the last quarter’s growth prints as well as some of the high frequency indicators of real economic activity in recent months. Our research team’s output gap estimates show some closure, attributable in part to improved credit growth and overall flow of financial resources to the commercial sector. 47. Output gap remains somewhat negative as reflected in present low capacity utilisation and high inventory. However, gradually improving credit metrics in several distressed sectors should pave way for improved investment over the next year. This process is expected to be further supported as cases referenced to Insolvency and Bankruptcy Code (IBC) resolve, facilitate consolidation, and restore pricing power. As public sector banks raise capital, receive recapitalisation from the government, and undertake reforms, credit flows to productive sectors of the economy should improve. 48. There seems little scope for accommodation or for change of stance at the present juncture. Hence, I vote to keep the repo rate at 6 per cent with neutral stance. Incoming data will be key to shape the policy going forward. I remain keen to (i) understand the impact of Goods and Services Tax (GST) on price levels as its rollout stabilises; (ii) assess in coming months the robustness of growth revival in GVA manufacturing; and (iii) track the impact of commodity prices on the Indian economy and markets. In parallel, the Reserve Bank is examining options to improve the transmission of its policy rate actions from banks to borrowers. Statement by Dr. Urjit R. Patel 49. The inflation scenario has evolved by and large along anticipated lines even as there was some unexpected firming up of food prices in October. (I say by and large because prints have been volatile throughout the year.) Inflation is now projected to be marginally higher, going forward, as the recent increase in oil prices is likely to sustain. Food inflation, led by vegetables, remains highly variable, while deflation in pulses continues. The impact of higher house rent allowance (HRA) of central government employees on housing inflation will peak in December. 50. There are several risks to the projected inflation trajectory. First, inflation expectations of households for both three-month ahead and one-year ahead periods in the latest round of the Reserve Bank’s survey moved up. The percentage of households expecting inflation to rise at a faster rate than the current level was the highest since end-2013. Second, rising input cost pressures across the board for both manufacturing and services have raised the risk of pass-through to output prices, especially because the growth momentum is projected to gain strength in the second half of the year. Third, fiscal slippage concerns linger on. Should this risk materialise, it would have implications for the inflation outlook. These risks to the inflation trajectory could, however, be alleviated to some extent by the expected seasonal moderation in vegetable prices and the pass-through of recent reduction in GST rates on certain goods and services to retail prices. 51. The acceleration in GVA growth in Q2:2017-18 (as projected in October) is comforting, especially because it was underpinned by a sharp increase in manufacturing. Growth in gross capital formation continued to recover. Going forward, lower rabi sowing and lower reservoir level pose a downside risk to agriculture activity. However, on the industrial front, the Reserve Bank’s industrial outlook survey points to an improvement in manufacturing sector business expectations in Q3. Various indicators of service sector activity, however, present a mixed picture. Financial conditions have improved significantly in the recent period as reflected in large capital raised from the primary capital market and a pick-up in bank credit growth. These perhaps may be indicating a long-awaited (modest) upturn in an investment cycle. 52. The macroeconomic situation has remained broadly unchanged since the last MPC meeting in October 2017. However, the recent upturn in crude oil prices has emerged as a source of concern. Several uncertainties, especially on the fiscal and external fronts, persist. It is, therefore, important to be vigilant. Hence, I vote for status quo in the policy rate, while maintaining the stance as neutral; this allows us the flexibility to respond appropriately to incoming data. Jose J. Kattoor

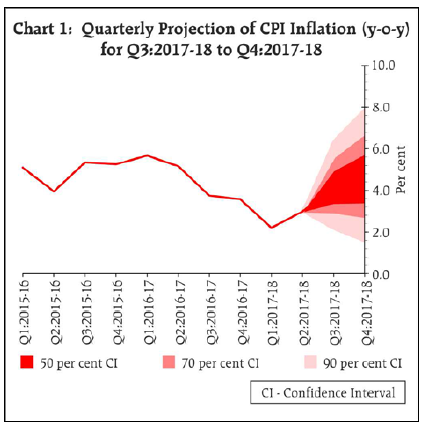

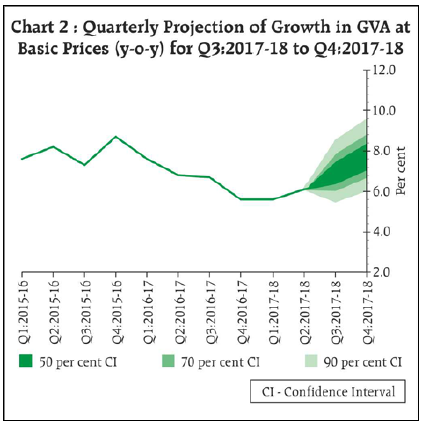

Chief General Manager Press Release : 2017-2018/1691 |