| September 07, 2015 Shri R. Gandhi

Chairman

Deposit Insurance and Credit Guarantee Corporation

Mumbai Dear Sir, Submission of Committee’s Report We have pleasure in submitting the Report of the Committee on Differential Premium System for Banks in India. On behalf of the members of the Committee, and on my personal behalf, I sincerely thank you for entrusting this responsibility to us. With kind regards Yours Sincerely Jasbir Singh

Chairman | | | | | | Meena Hemachandra

Member | Rajesh Mokashi

Member | Suma Varma

Member | Sudarshan Sen

Member | | | | | | Malvika Sinha

Member | S. Rajagopal

Member | A.R. Joshi

Member | Sonjoy Sethee

Member | | | Jaya Mohanty

Secretary |

Chapter 1

Introductory 1.1 Deposit Insurance protects depositors against the loss of their deposits in case a deposit institution is not able to meet its obligation to the insured depositors. On the flip side, the parties to the deposit insurance viz. a bank and its insured depositors get an incentive to take more risk because the costs of risk, in whole or in part, are borne by others, generally a deposit insurance agency, e.g. Deposit Insuarance and Credit Guarantee Corporation (DICGC) in India. This behaviour of the parties is termed as moral hazard. The financial crisis of 2008 has, alongwith the other issues concerning regulation and supervision, brought the debate on the moral hazard aspect of Deposit Insurance back to the table. The IADI (International Association of Deposit Insurers) Core Principles for Effective Deposit Insurance Systems (2014) have elaborated in detail on this issue. Flat rate versus Risk based premium 1.2 The Deposit Insurance Systems around the world have evolved over time by reforms adopted by various jurisdictions based on experience, international developments, guidance from supra national bodies like IMF, IADI and other environmnetal changes from time to time. These reforms also included efforts to reduce the moral hazard, for example, through limited coverage levels and scope; differential premium systems (DPSs); and timely intervention and resolution by the deposit insurer or other participants with such powers in the financial system safety-net. Most deposit insurance systems initially adopt an ex-ante flat-rate premium system because they are relatively simple to design, implement and administer. However, these systems were open to criticism in that they do not reflect the level of risk that banks pose to the deposit insurance system. Flat-rate premium systems have also been viewed as being unfair as “low-risk” banks are required to pay the same premium as “higher-risk” banks. With no inbuilt incentive for “higher risk” banks to improve their risk profile, a flat rate system would accentuate the moral hazard problem. Therefore the primary objective of most differential premium systems has been to provide incentives for banks to avoid excessive risk taking, minimise moral hazard and introduce more fairness into the premium assessment process. Introducing fairness into the system bolsters industry support for deposit insurance. 1.3 Keeping this perspective in mind, there has been an increasing recognition among the deposit insurance agencies around the world about the need for introduction of a DPS based on the risk profile of banks, also often referred to as Risk Based Premium (RBP). Keeping in view the challenges involved in devising a rating model and other related issues, the IADI prepared a note detailing General Guidance for Developing Differential Premium Systems (2011) for the Deposit Insurance Agencies (DIAs), which intended to switchover to RBP. 1.4 The Federal Deposit Insurance Corporation (FIDC), US, made a beginning in 1993 by introducing RBP. Since then, 26 of the 75 member jurisdictions of the IADI have adopted risk-based premium as on December 31, 2013. Risk Based Premium in India 1.5 In India, the commercial banks, Regional Rural Banks (RRBS), Local Area Banks (LABs) and co-operative banks are covered by deposit insurance with the premium being charged at a flat rate of 10 paisa for Rs. 100. Historically, deposit insurance claims on the DICGC have generally originated on account of failure of co-operative banks, as these institutions have been more susceptible to frequent failures due to a number of factors. It is worth mentioning that the last claim settled in respect of a commercial bank was way back in 2002. As a result, a perception of cross-subsidisation in operation of the deposit insurance system has gained currency. 1.6 DICGC Act 1961 enables the Corporation to charge the premium at different rates for different categories of the insured banks. Various Committees constituted by the Government of India, Reserve Bank of India (RBI) and DICGC in the past have made recommendations for the introduction of risk-based premium for banks. The Narasimham Committee Report on the Banking Sector Reforms (1998), while focusing on the structural issues, recommended introduction of risk based premium system in lieu of the flat rate premium system. This view was echoed by the Capoor Committee on ‘Reforms in Deposit Insurance in India’ (1999). The Committee on Credit Risk Model (2006) constituted by the DICGC also recommended the introduction of risk based premium, to begin with, for Scheduled Commercial Banks (SCBs) and Urban Co-operative Banks (UCBs). Notwithstanding the recommendations of these committees in the past, the implementation of risk-based premium could not be operationalised, inter alia, due to co-operative and regional rural banks (forming over 90 per cent of insured banks) being under restructuring until recently, absence of robust supervisory rating for all insured banks especially co-operative banks, etc. 1.7 In India, there has been a persistent demand from stakeholders and public representatives in the recent past for a hike in deposit insurance cover from the current level of Rs.0.1 million. A hike in cover without calibrating the premium rates to the risk profile of the insured banks only exacerbates the moral hazard. Recognising this, it has been felt that introduction of RBP may be taken up to make ground for considering raising the insurance cover from the present ceiling of Rs 0.1 million. 1.8 Accordingly, a Committee on Differential Premium System for Banks in India (Chairman: Shri Jasbir Singh) was constituted vide Notification dated 31 March 2015 (copy annexed) to make recommendations for the introduction of risk based premium in India. Composition of the Committee 1.9 The Composition of the Committee was as follows: | 1. Shri Jasbir Singh | Executive Director | Chairperson | | 2. Smt. Meena Hemachandra | Executive Director, Reserve Bank of India | Member | | 3. Shri. Rajesh Mokashi | Deputy Managing Director, CARE Ratings | Member | | 4. Smt. Suma Varma | PCGM, DCBR | Member | | 5. Shri. Sudarshan Sen | PCGM, DBR | Member | | 6. Smt. Malvika Sinha | PCGM, DCBS | Member | | 7. Dr. S. Rajagopal | CGM, FSU | Member | | 8. Dr.A.R. Joshi | Adviser, DSIM | Member | | 9. Shri. Sonjoy Sethee | CFO, DICGC | Member | | 10. Smt. Jaya Mohanty | Adviser, DICGC | Secretary | The Terms of Reference 1.10 The terms of reference of the Committee were as under: -

To devise and recommend a model of risk assessment for banks, both commercial and co-operative. -

To make recommendations for adapting the model of risk assessment so derived to the calculation of premium to be paid to DICGC. -

To study international methodology of risk based premium to ensure that the rating system developed is in tandem with international best practices. -

To make recommendation for institutionalising the flow of information between the supervisory Departments of RBI, insured banks and the DICGC at appropriate frequencies to facilitate the calculation of the risk rating. -

To recommend a matrix of premium rates corresponding to risk-ratings in a manner that there is least disturbance to the existing premium inflows. -

To make recommendations for frequency and timing of revision in premium rates and relating the timing of revision to appropriate risk-rating reference date. Approach of the Committee 1.11 Given the terms of reference and coverage of the wide spectrum of banking systems, viz commercial and co-operative banks, RRBs and LABs, the Committee deliberated on the following aspects in developing an appropriate framework for the rating model and the various other facets of risk-based premium. -

A robust and simple model with qualitative and quantitative inputs appropriately weighted, with a good predictive power -

Simulating the model for rating the banks into groups for risks and therby assigning premiums as per the risk ratings -

The data issues like frequency, quality, and intergrity. -

Issues connected with confidentiality of ratings, sharing of ratings with the banks, etc. -

Frequency of setting/resetting premium rates with appropriate reference dates -

The transition path The Committee held three meetings on April 17, May 19 and on August 27, 2015 to crystallise its thoughts on the above issues. Structure of the Report 1.12 The report is organised into five Chapters including the Introductory chapter. Chapter 2 provides the practice and experience on risk-based rating and methodologies adopted by some deposit insurance agencies in advanced and emerging market economies. Chapter 3 provides an analysis of key considerations in developing a rating model for the introduction of risk-based premium, while the Chapter 4 presents the model. Chapter 5 summarises the key recommendations of the Committee. Acknowledgments 1.13 The Committee benefitted from the fruitful discussions and deliberations by the Members of the Committee. The Committee wishes to thank officials of CARE Ltd., viz., Shri Arun Kumar, Shri Anuj Jain, and Shri Pankaj Naik for technical inputs in the provision of a rating model. The Committee places on record its appreciation for painstaking efforts put in by Dr. Pradip Bhuyan, Director, Banking Studies and Risk Modelling Division, DSIM in conduct of an elaborate simulation exercise and helping firm up the various ingredients of the model. Shri Aloke Chatterjee, Shri R. Ravikumar, Shri Navin Nambiar and Shri D.P. Singh of Department of Banking Supervision and Shri Bhaskar Birajdar and Shri S.M. Mane of Department of Co-operative Banking Supervision were extremely helpful in providing data on various parameters relating to scheduled commercial banks and urban co-operative banks. Thanks are due to officials of NABARD Smt. Vijaya Lakshmi and Shri S.H. Khemchandani for provision of data relating to RRBs, and State and District Central Co-operative Banks. The officials of Reserve Bank of India, viz., Shri Ajay Kumar Sinha, Smt. Kumudini Hajra, Smt. Nimmi Kaul, Smt. Reeny Ajith were helpful in providing inputs to the deliberations of the meetings. The Committee would like to thank the officers of the Corporation Shri B.K. Panda and Shri M. Ramaiah for their support in the preparation of the Report. Ms. Darshana Naik and Ms. P. Pinto of DICGC deserve thanks for secretarial services.

Chapter 2

Risk Based Premium - Cross-Country Practices and Experience 2.1 Deposit insurers collecting premiums from member financial institutions choose between adopting a flat-rate premium system or a system that seeks to differentiate premiums on the basis of individual bank risk profiles. Although flat-rate premium systems have the advantage of being relatively easy to understand and administer, they do not take into account the level of risk that a bank poses to the deposit insurance system and can be perceived as unfair in that the same premium rate is charged to all banks regardless of their risk profile (IADI, 2011). 2.2 The deposit insurance, like any other insurance product, has an inherent problem of moral hazard. The moral hazard theory in deposit insurance argues that deposit insurance creates a strong incentive for the management of banks to choose a high leverage and for the customers of banks to loosen their monitoring the activities of their banks. The presence of moral hazard is more pronounced when the premium of deposit insurance does not properly reflect the effective underlying risk associated with the activities of the banks. 2.3 However, moral hazard could be partially mitigated by introducing appropriate design features to the Deposit Insurance System that would generate incentives for the banks to improve their risk profile. Besides limited coverage levels and scope, and provisioning for timely intervention and resolution by the deposit insurer or other participants with such powers in the financial system safety-net, the design could also provide for collecting a risk-adjusted premium from member banks. 2.4 For these reasons primarily, beginning with the US in 1993, a number of countries adopted risk based premium in their jurisdictions in lieu of flat rate one. Since that time, the number of systems adopting risk based premium has grown steadily, currently estimated to be twenty-six countries, including: Argentina, Canada, Colombia, Finland, France, Germany, Kazakhstan, Malaysia, Peru, Portugal, Romania, Taiwan, Turkey and Uruguay, to name some. 2.5 A brief account of the practices and operations of risk based premium system in some jurisdictions is given in the following paragraphs. United States 2.6 In the case of Federal Deposit Insurance Corporation (FDIC), the premium rate was set by statute and could be changed only by action of the U.S. Congress. The premium rate was expressed as a percent of assessable deposits. Till 1993, it charged flat-rate deposit insurance premiums from all insured banks. The incresing bank failures in the 1980s and early 1990s, raised the concerns and legislation was passed that required the FDIC to establish a system of risk-based premiums. The FDIC based its risk based schedule of premium rates on a combination of objective criteria: (1) capital ratios1 based on financial reports that insured institutions were required to file quarterly with the regulatory agencies; and (2) subjective criteria namely CAMELS ratings2 derived from on-site examinations. 2.7 The risk-based premium rate schedule sought to achieve the following objectives: -

Be fair, easily understood, and not unduly burdensome for weak banks; -

Produce sufficient revenue within 15 years to recapitalise deposit insurance funds that had been depleted by the large costs of failure of the 1980s; -

Increase incentives for insured institutions to operate safely; and -

Provide a transition from flat-rate premiums to a “permanent” risk-based system. 2.8 The FDIC implemented the differential premium system effective January 1, 1993, and it began computing risk-based premiums according to a nine-cell matrix using capital ratios and supervisory ratings. (Table 1). | Table 1: Rating Matrix | | Capital category | Supervisory rating | | A | B | C | | 1. Well capitalized | | | | | 2. Adequately capitalised | | | | | 3. Undercapitalized | | | | 2.9 Institutions in column A had the highest supervisory ratings, while those in column C had the lowest. While the supervisory ratings were based essentially on CAMELS ratings assigned by the primary regulators, the institutions were assigned to capital categories on the basis of a number of capital ratios. The minimum premium rate of 23 basis points was mandated by law and corresponded to the rate paid by all institutions prior to the adoption of the risk-related premium system. 2.10 The FDIC had a Target Fund Ratio (a ratio of deposit insurance fund divided by the insured deposits) of 1.25%. When a deposit insurance fund fell below the target ratio of 1.25 percent of insured deposits, the FDIC was required to charge premium rates that would restore the fund to the target ratio within one year, or charge an average premium of at least 23 basis points. Beginning in 1996, the FDIC was prohibited by law from charging well-managed and well-capitalised institutions (those in the 1A cell in the table 1 above) for deposit insurance when the fund's reserve ratio was expected to remain at or above 1.25 percent. Reform of the FDIC Risk-Related Premium System 2.11 While, the risk-related premium system implemented in 1993 was an improvement over the flat rate system it replaced, some provisions of the system and the governing statutes had unforeseen consequences that required corrective action. 2.12 The establishment of a “hard target” for the ratio of 1.25 percent of insured deposits was intended to ensure that the cost of deposit insurance would be borne by the industry and not by taxpayers. However, because the FDIC was required to restore the fund within one year or charge an average premium of 23 basis points if the fund fell below the target, a sharp rise in premiums proved counter cyclical as the rise could occur in a weak economy when the industry could least afford it. On the other hand, when the Reserve Fund Ratio was at 1.25% or above, the FDIC could not collect premium from institutions in category 1A, though they too posed some risk. Therefore as part of reform process, the Federal Deposit Insurance Reform Act of 2005, established a range within which the Board could set a target reserve ratio (and thus the size of the fund), and provided substantial flexibility for the Board to manage the size of the fund. 2.13 Significant refinements to the risk-related premium system were implemented pursuant to financial reform legislation enacted in 2010. Modifications included redefining the assessment base as average consolidated total assets minus average tangible equity (rather than total domestic deposits, the assessment base that had been in place since inception), revising the system for small bank risk assessment, and substantially redesigning the pricing framework for large institutions. Risk differentiation for small institutions 2.14 In developing the new pricing framework for small institutions - generally those with lower than $10 billion in assets - the FDIC decided to continue to rely on supervisory evaluations and capital levels as a basis for risk differentiation. As the FDIC found that the number of institutions in several of the risk categories were low and the historical five-year failure rates for some of risk categories were similar, the FDIC consolidated the nine existing categories into four. The four new risk categories are referred to as risk categories I, II, III, and IV (Table 2) | Table 2: Risk Categories | | Capital Group | Supervisory Group | | A | B | C | | Well | I | II | III | | Adequate | II | II | III | | Under | III | III | IV | Risk differentiation for large institutions 2.15 From 2007 through 2011, the FDIC used a combination of risk measures, namely, CAMELS ratings, and the forward looking financial measures of risk to differentiate large banks according to risk. Based upon its experience during the most recent banking crisis (which started in 2008), in 2011 the FDIC adopted a risk-differentiation scheme for all large institutions that eliminates risk categories and attempts to predict risk much farther in the future using measures that were associated with risk during the crisis. 2.16 For large institutions, two scorecards are used: one for most large institutions, and a second for very large institutions that are structurally and operationally complex or that pose unique challenges and risks in case of failure (“highly complex institutions”). Both scorecards combine CAMELS ratings and forward-looking financial measures to assess the risk a large institution poses to the Deposit Insurance Fund (DIF). Each assesses certain risk measures to produce a performance score and a loss severity measure that are combined and converted into an initial assessment rate. For large institutions, it provided for adjustment in the premium rates by giving credit for long term debt (i.e. adjusting the base premium rate downward) and levying a charge for brokered deposits, adding to the base premium rate. Canada 2.17 In 1995, Canada amended the Canada Deposit Insurance Corporation (CDIC) Act to replace CDIC's flat rate premium system with a system which would classify member institutions into different risk categories, in large part reflecting the risks posed to CDIC, and charging varying premium rates based on these categories. The design, development and consultation process associated with CDIC's Differential Premium System underwent an elaborate process during a three year period spanning 1996 to 1999. 2.18 In developing a differential premium system, CDIC examined a number of possible approaches that would enable it to classify member institutions into different categories for differential premium rating purposes. These included single quantitative and qualitative factor systems and a range of combined quantitative and qualitative factor systems – including the risk-based premium approach used by the Federal Deposit Insurance Corporation (FDIC) in the United States, the Bank of England TRAM model and the methodologies used by rating agencies. CDIC also took into account the feedback from regulators of CDIC member institutions, other supervisory agencies and a committee of senior executives from representative CDIC member institutions. 2.19 The Corporation introduced the new system commencing 1999. CDIC's differential premium system in use, scores members over quantitative and qualitative fatcors. The transition period provided for the bonus markups over the actual score during the first two years by 20% and 10% points respectively to enable the member institutions to adapt to the risk based premium system. 2.20 The CDIC as part of its periodic review exercise, has revisted the rating model, reviewed these quantitative and qualitative criteria recently and refined it marginally. A distinction between non-DSIBs (Domestic Systemically Important Banks) and D-SIBs has been introduced through one parameter having a weight of 5%. The quantitative factors are grouped into three broad categories: capital adequacy, other quantitative measures – earnings capacity, efficiency, and asset growth and asset concentraion/encumberance; all together carrying a weight of 60%. The qualitative measures include supervisory rating (35%) and other information (5%). The new rating matrix is in Table 3: | Table 3: Summary of Criteria or Factors and Scores | | Criteria or Factors | Maximum Score | | Quantitative: | | Capital Adequacy | 20 | | Other Quantitative | | | Return on Risk-Weighted Assets | 5 | | Mean Adjusted Net Income Volatility | 5 | | Stress Tested Net Income | 5 | | Efficiency Ratio | 5 | | Net Impaired Total Capital | 5 | | Three-Year Moving Average Asset Growth | 5 | | Real Estate Asset Concentration* | 5 | | Asset Encumbrance Measure** | 5 | | Aggregate Commercial Loan Concentration Ratio | 5 | | Sub-total: Quantitative Score | 60 | | Qualitative: | | Examiner’s Rating | 35 | | Other Information | 5 | | Sub-total: Qualitative Score | 40 | | Total Score | 100 | *Every member institution that is not a domestic systemically important bank (DSIB) must complete this form ** Only a member institution that is a domestic systemically important bank must complete this item. 2.21 The CDIC considers regulatory capital as a cushion against adverse changes in a members’ asset quality and earnings. This incorpration of other quantitative factors are intended to assess the ability of a member institution to sustain its capital. Premium Categories 2.22 CDIC has put into practice a four-category system appropriate for its financial system. The premium categories and related scores are set out in the Table 4. | Table 4: Score and Premium Categories | | Score | Premium category insured deposits | | >= 80 | 1 | | >= 65 but < 80 | 2 | | >= 50 but < 65 | 3 | | < 50 | 4 | 2.23 Premium rates set accross the categories rise in gemetric progression along the rating scale, which are so set with an eye on providing substantial incentive to the member institutions to improve their ranking from lower to higher grades. The setting of premium rates, besides being directionally related to the ratings, has also been guided by the revenue needs of the Corporation and accordingly the premium rates have seen revisions on both in the upward and downward directions. 2.24 The CDIC shares the assigned premium category with each member with a rider that the member institution is prohibited from disclosing the category/premium rate or any other information relating to rating provided to the member institution. European Union 2.25 The practices in the European Union (EU) nations suggest that the key financial ratios currently applied across member states are quite heterogeneous and the variables taken into account to define them are not identical. They are arrived at in terms of ratios using balance sheet data, financial statement data or other types of account data. For example, France uses solvency, risk diversification, operational profitability and maturity transformation as input variables, while German BVR (Protection scheme of German Cooperative Banks) model incorporates information on capital structure, income structure and risk structure. The indicators used in the models can be broadly grouped into three main classes, each related to one particular aspect of bank activities. The first class reflects their capital structure and solvency profile; the second class measures the riskiness and exposure of the banks; and finally the third set of indicators being the profitability/income. 2.26 As part of reforms, the EU issued a new Directive 2014/49 on the Deposit Guarantee Schemes (DGSs). The directive prescribes achieving a minimum harmonisation such as uniform protection to depositors, and each EU member state to reach a target fund of 0.8% of covered deposits by 2024. While the directive prescribes that collection of premium be based on the amount of deposit covered and risk profile of the member institution, it leaves the measures of risk to the wisdom of member institutions with a broad guidance such as low risk sectors regulated under national laws may provide lower contributions and risk measures may take into consideration capital adequacy, asset quality and liquidity; etc. Colombia 2.27 Colombian Deposit Insurance Agency FOGAFIN which was set up in 1985, charged a flat rate premium to all its member banks prior to 1998. In the year 1998, FOGAFIN introduced an element of risk based component of premium, based on the ratings from the credit rating agencies, as mark up over the flat (base) premium rate. The risk- rating was replaced by CAMEL score arrived at by the Financial Supervisory Authority. Subsequently, FOGAFIN established its own CAMEL scoring system in 2009. Presently, FOGAFIN has a hybrid premium scheme comprising of a flat rate premium and a variable premium component based on the risk profile of the member institution. While the flat rate premium is paid by the member institutions quarterly through the year, risk based component is evaluated at monthly frequencies, based on CAMEL model which gives a score between 1 (the institutions with the highest risk profile) and 5 (the institutions with the lowest risk profile). The key elements of CAMEL evaluation are furnished in Table 5. | Table 5: CAMEL Model | | | Weight | Ranges | Score | | Capital | Solvency | 25% | < 8% | 1 | | > = 8% y <9 % | 2 | | > = 9% y <10 % | 3 | | > = 10% y <12 % | 4 | | > 12 % | 5 | | Asset: | Non-performing Loans/Total Loans | 20% | > 8% | 1 | | > 6% y < = 8 % | 2 | | > 4% y < = 6 % | 3 | | > 3 % y < = 4 % | 4 | | < = 3 % | 5 | | Management | Operational expenses / Gross financial margin | 20% | > 80% o < 0 % | 1 | | > = 70% y < = 80 % | 2 | | > = 60% y < 70 % | 3 | | > = 50% y < 60 % | 4 | | <50 % | 5 | | Earnings | Return on Assets | 20% | < 0% | 1 | | > = 0% y < 1 % | 2 | | > = 1% y < 2 % | 3 | | > = 2% y < 3 % | 4 | | > = 3 % | 5 | | Liquidity | (current assets - current liabilities)/ total deposits | 20% | <= -10% | 1 | | > = -10 % y < = 4 % | 2 | | > 4% y < = 6 % | 3 | | > 6 % y < = 15 % | 4 | | < = 15 % | 5 | 2.28 The CAMEL score is the key differentiating factor for the member institutions and for setting the differential premium. While there are incentives provided to high rated banks, in the form of refund of premium paid in previous year, ranging up to 50% depending upon the rating, a lower rated institution similarly is required to pay additional premium rising upto 50% of the premium paid in the previous year. Therefore there are strong inbuilt incentives for the institutions to improve their risk profile. Malaysia 2.29 Since the introduction of the deposit insurance system in September 2005, Malaysia had adopted an ex ante funding approach where the premiums charged to the member institutions had been based on a flat-rate premium system. Under this system, the annual premium rate of 0.06% was applied to all members. The Malaysia Deposit Insurance Corporation (MDIC) Act 2005 enables MDIC for the establishment of Differential Premium System (DPS). Accordingly, Malaysia switched over to the DPS in 2008 by replacing the flat-rate system. Since then, Malaysia has revisited and reviewed its premium system in 2011 and recently in 2015 and has improved it further. 2.30 The Malaysian differential premium system has continued to nurture throughout, four key objectives namely, (a) to differentiate banks according to their risk profiles; (b) to provide incentives for banks to adopt sound risk management practices; (c) to introduce greater fairness into the premium assessment process; and (d) to contribute to stability of the financial system via the overall improvement in risk management practices of banks. 2.31 MDIC uses a combination of quantitative and qualitative inputs in scoring individual banks. The quantitative factors which account for a score of 60 out of 100 include capital adequacy, profitability, asset quality, asset concentration, asset growth, loan concentration, and funding profile, etc. The remaining score of 40 accounts for the qualitative criteria which include supervisory rating (35) and other information (5). Premium categories 2.32 Member institutions are classified into one of four premium categories based on their DPS scores, 1 representing the best, and 4 the lowest. The score ranges and corresponding premium categories are set out in Table 6. | Table 6: Scores and Premium Categories | | Score | Premium Category | | ≥ 85 | 1 | | ≥ 65 but < 85 | 2 | | ≥ 50 but < 65 | 3 | | < 50 | 4 | Taiwan 2.33 The Central Deposit Insurance Corporation, Taiwan established in 1985 followed a flat rate premium system until mid-1999 when it switched over to risk based premium. Under the Risk-based Premium System, premium rate for individual insured institution is set based on each insured institution's risk level. The risk level is determined on the basis of two risk indicators: capital adequacy ratio (CAR) and Composite Score of the Risk-based Premium Rating System (CSRPRS) based on Financial Early Warning System. The CAR and CSRPRS are both divided into three risk grades: -

CAR grades: Well Capitalized (12% and above), Adequately Capitalized (8% and above and below 12%), Undercapitalized (below 8%) -

CSRPRS grades: Grade A (composite scores of 65 and over), Grade B (50 to under 65), Grade C (less than 50) 2.34 Based on the above, the Corporation places all banks in five different risk groups. Deposit Insurance Premium Rates 2.35 Five-tiered premium rates are set based on the risk groups of the insured institutions. -

For domestic banks and local branches of foreign and Mainland Chinese banks in Taiwan, premium rates are 0.05%, 0.06%, 0.08%, 0.11%, 0.15% of covered deposits. Eligible deposits in excess of coverage limit are applied a flat rate of 0.005%. -

For credit cooperatives, premium rates are 0.04%, 0.05%, 0.07%, 0.10% and 0.14% of covered deposits. Eligible deposits in excess of coverage limit are applied a flat rate of 0.005%. -

For credit departments of farmers' and fishermen's associations, premium rates are 0.02%, 0.03%, 0.04%, 0.05%, and 0.06% of covered deposits. Eligible deposits in excess of coverage limit are applied a flat rate of 0.0025%. Conclusions 2.36 This study of a few deposit insurance systems as above, throws out some very useful insights in the context of risk based premium systems. The key insights obtained from the study are as under: -

There is wide acceptance of the fact that differnetial premium system is more fair and incentivises the performance and sound risk management systems. -

Premium differentiation exercise generally is aimed at devising a system for differentiating one bank from another for the purposes of grouping into premium categories and does not seek to measure the exact risk, except perhaps the US, where FDIC uses forward looking risk measures for large institutions. -

Based on the individual scores obtained under ratings process, banks have been categorised generally into four or five risk and thus, premium categories. For small banks, US reduced the number of categories from 9 to 4 based on its experience that historically, in some of the categories, the number of banks remained consistently low. The argument against having large number of categories is that it results in a less visible distinction among the member institutions and less incentive for moving from a lower category to higher category. -

The risk rating process ranges from fairly simple like that of Colombia, Turkey, and Kazakhstan to a complex one as in US which has a risk based one through forward looking risk measures for large institutions. -

In some jurisdictions, supervisory rating is used as an input into the rating model with about one-third weight in the aggregate maximum possible score (Malaysia, Canada, Turkey). The supervisory rating is being provided to deposit insurance agencies as part of the information sharing and cooperation arrangement among the safety net participants. -

Transition period from the flat rate system to the differential rating based one has been fairly liberal (e.g. 3 years in Canada). -

The composite score intervals for categorisation purposes differ from accross jurisdictions. For example, highest rated category has a score of 85 (out of 100) upward in Malaysia (in four category matrix) and Kazakhstan (in five category matrix), 80 upward in Canada and Turkey (in four Category Matrix). -

The rating models are being consistently reviewed in the context of evolving regulatory and general financial system environment – internal as well global. References -

DICGC (2006), ‘Report of the Committee on Credit Risk Model’. -

European Commission (2008), ‘Risk-based Contributions in EU Deposit Guarantee Schemes: Current Practices’, Joint Research Centre. -

International Association of Deposit Insurers (2011), ‘General Guidance for Developing Differential Premium Systems’, October. -

www.cdic.gov.tw -

www.cdic.ca -

www.ec.europa.eu -

www.pidm.gov.my

Chapter 3

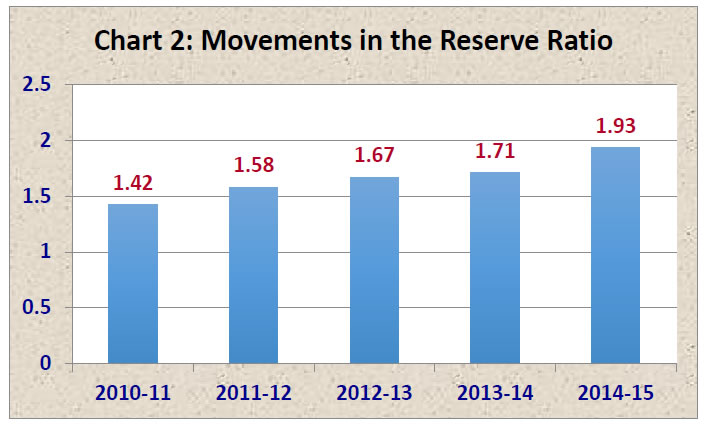

Developing a Rating System – Key Considerations Introduction 3.1 The Committee recognised that the introduction of differential premium system (DPS) for deposit insurance is a proposal with far reaching consequences for both the insured banks and the DICGC. A perusal of the developments in some of the other deposit insurance systems, as presented elsewhere in Chapter 2 of the Report highlights the challenges involved in the designing, introducing and operating of a DPS. Being conscious of this, the Committee systematically outlined the key considerations in this regard, discussed them in detail by taking into account various perspectives and trade-offs, to arrive at a consensus on a pragmatic approach, suited for the Indian environment. Approaches for differentiating banks 3.2 A good DPS should attempt to achieve (a) differentiating banks into different risk categories, (b) be forward-looking in assessment, (c) utilise and access a variety of information and (d) find acceptability among the insured member banks. International literature on deposit insurance indicates various methodologies for differentiating banks based on their risk profile. The methodologies could be highly objective using only quantitative parameters or somewhat subjective evaluating qualitative aspects of a bank. Quantitative aspects may include meeting the regulatory capital requirements, asset portfolio diversification, earnings and profitability, asset quality, liquidity, etc. At advanced level, the quantitative evaluation may also be done through the “expected loss” method. For example, Merton compared deposit insurance to the equivalent of a put option on the insured institution’s assets and the value of these assets therefore could be calculated by using Black-Scholes option pricing model. Later Marcus and Shaked (1984) and Ronn and Verma (1986) applied option-pricing model for discovering individual institution’s premium rate1. The Committee on Credit Risk Model (2006) set up by the Corporation had recommended option-pricing model for India. Although theoretically appealing, use of an option-pricing model is a data intensive exercise and poses serious challenges, given the banking environment of India. 3.3 Qualitative criteria use a number of factors such as management quality, governance standards, and quality of internal controls and processes, which not only indicate the current state but also have a predictive power about at least the near future state of the insured institution. Qualitative evaluation requires instituting an appropriate examination system of the insured institutions for collecting soft information and assessing the quality. 3.4 Jurisdictions like US, Canada, Malaysia and Turkey combine the quantitative and qualitative parameters in their risk assessment exercise. The Qualitative parameters essentially include supervisory rating by way of weights in the over all model. For large institutions, FDIC combines CAMELS rating and forward looking financial measures through which the FDIC attempts to predict the future risk. The advantage of using a combination of qualitative and quantitative parameters is that risk assessment system becomes a comprehensive and effective one with forward-looking risk profiling. Adoption of such a system assumes the existence of an appropriate set up for gathering qualitative information, which can be achieved through onsite assessment of the institutions or information sharing arrangement with the supervisory agencies. Universe of Insured Banks and Model Selection 3.5 After having discussed the various approaches to the rating exercise, the Committee recognised that a rating model would need to take into consideration the characteristics of the banks it would address the model to. The members recognised the diversity in membership of the Corporation. The membership constituted of public sector and private sector banks, domestic and foreign banks, special category banks like Regional Rural Banks (RRBs), Local Area Banks (LABs) and Cooperative Banks. These classes of banks differed in size and nature of operations, level of sophistication, levels of technology adoption, governance characteristics and standards of data management. The Committee noted that the number of insured banks as on March 31, 2015 aggregated to 2,129 including 92 commercial banks, 1,977 Cooperative banks, 56 RRBs, and 4 LABs. The category-wise share of assessable deposits (i.e. the deposits subjected to premium collection), correspondingly was 90.3%, 7.0%, 2.7%, and the LABs’ share wasnegligible. The Committee debated upon the magnitude of task likely to devolve on the Corporation in finalising the rating process and the heterogeneity in the different classes of banks in the context of their adaptive capabilities. It was felt that the model should be a simple and easy to understand but robust one, capturing key risk parameters. (Recommendation 1) 3.6 The Committee additionally appreciated the status of public sector banks – perceived to have implicit government guarantee or backing. The Committee considered that internationally a preponderant view is that all safety-net tools should apply uniformly across all classes of institutions and the taxpayers’ money should not be used in resolving any institution. In the similar vein, implicit guarantees in the form of government ownership should not be given weightage in risk profiling of institutions. The Committee also took note of the fact that over the time, the government ownership of public sector banks may be diluted substantially. The committee therefore recommended that in all fairness, the rating system should, as far as possible, be ownership neutral. Number of Rating Categories 3.7 The Committee considered the question of number of categories into which the banks could be grouped based on the assigned scores. The Committee felt that while across the scale, there is a possibility of any number of ratings, the argument against several is that more categories result in a less visible distinction among them along the scale, and there is less incentive for moving from a lower to a higher category because gains from moving a step up may not be very material. FDIC, which had categorised small banks into nine categories at some stage, on a review, had concluded that number of institutions in several categories had remained consistently low and had therefore reduced the categories to four. A review of practices in some jurisdictions revealed that number of rating categories ranged from 3 to 5. The Committee also referred to the IADI Core Principle relating to the differential premium system, which inter alia envisaged that premium categories should be significantly differentiated. The consensus view, therefore, was that number of rating categories for assigning premium rates should be limited to four or five. (Recommendation 2) Model Input Variables 3.8 The Committee was of the opinion that in assessing a bank for its risk, besides the balance sheet data that would essentially mean quantitative; qualitative information such as management quality, governance and systems and control should be considered for the completeness of the exercise. The Committee discussed about the ways to source qualitative inputs for the rating exercise. The Committee observed that rating models of Malaysia, Turkey and Canada had the supervisory ratings as one input parameter, carrying a weight of about 35%. The Deposit Insurance Agencies in these jurisdictions have access to the supervisory rating under an arrangement formalised through law and/or information sharing arrangement between the DIAs and the supervisors. Accordingly, the Committee felt that inputs from supervisors for respective banking sectors, based on their annual inspections could be provided to the Corporation. Considering, the inspection schedules of the supervisors and the corresponding lags in availability of the qualitative findings, accessing supervisors’ inputs were not considered feasible at this stage. Other alternative considered was that the Corporation could have its own set up for bank visits to assess the qualitative indicators. The Committee however was of the opinion that given the number of banks insured, such an exercise would require the Corporation to have massive manpower resources which weighed against such an arrangement in the medium term. The Committee therefore came to the view that the input variables could be designed based on the annual audited/published data of the individual banks for a large part say weighing upto 90% in the overall score. The Committee also drew comfort from the fact that many of the items in the balance sheet and profit and loss account intuitively were reflective of the quality of soft parameters such as internal controls and processes, personnel skills and governance. ‘Other information’ like conduct of a member in dealings with the Corporation, eligibility for access to Reserve Bank’s liquidity window, regulatory penalties, adoption of IT and other soft information may constitute remaining 10%. (Recommendation 3) Predictive Power of the Model 3.9 The Committee observed that the Corporation, like any insurance system, was insuring the depositors’ risk for a prospective period. Hence any model to be used for rating should have the power to predict the risk of insured banks in the near future. The Committee felt that such an assurance could be derived only from forward looking inputs into the model; qualitative indicators, being some of them. Risk based inspection format adopted by the supervisors was indicated to have predictive power for the risk direction but complete implementation thereof across the entire universe of insured banks was still far away. The Committee was of the view that following the practice of quite a few jurisdictions (Canada, Malaysia, Turkey, US) in which supervisor’s rating is an important input, the Corporation and Supervisors may initiate a dialogue to consider entering into a formal arrangement under which the supervisors could share their ratings with the Corporation under appropriate safeguards of confidentiality and usage, in due course of time by which the supervisors would have subjected all the banks to the forward looking risk assessment. Corporation then can use supervisory rating as an additional input in the rating process to refine the model. (Recommendation 4) Data source, Data Quality, Quality Assurance and Frequency 3.10 Sourcing of quality data is a key in development of risk rating. The Committee, accordingly, deliberated on the sources of data for the model. The Committee members from the regulatory and supervisory departments were requested to inform the Committee whether they could assist in providing the requisite data on a regular basis at desired frequencies. The members concerned observed that while the data pertaining to commercial banks was fairly current and sufficiently exhaustive at any point of time, there were apprehensions about the quality and timeliness in getting the data from cooperative banks particularly, the non-scheduled ones, which were substantial in number. Notwithstanding the above, the Committee decided to use the data presently available with the regulator/supervisor for a limited purpose of simulation exercise for developing the rating model. For operationalization of the rating system, the Committee felt that the Corporation could institute its own MIS for the member banks and tag it to the half yearly Deposit Insurance (DI) returns being presently received from the banks. (Recommendation 5) 3.11 For ensuring the integrity of the data, the committee viewed the importance of sample verification of the data submitted, by accessing the primary source at banks’ site. It was informed to the Committee that the Corporation is currently utilising the services of supervisors for feedback collected during the course of their inspections, on the correctness of compilation of returns submitted to the Corporation. The Committee desired that during the course of their inspection as and when taken up, the supervisors could extend the checking to the information to be submitted by the banks in the context of rating also for the feedback to the Corporation. (Recommendation 6) 3.12 The Corporation could also utilise the supplementary information available from sources easily accessible, to upgrade its market intelligence about general well being of the member banks and also to use this information to validate the Corporation’s assessment of banks. For example, in the case of commercial banks and scheduled UCBs, the peer reviews being prepared by regulatory/supervisory departments would provide a good indication about banks’ current state and the likely future. The Committee also suggests obtaining appropriate periodic inputs from NABARD in respect of RRBs, and State/District Central Cooperative Banks. (Recommendation 7) 3.13 The Committee stressed that timely receipt of the data from member banks was crucial for the rating exercise. It was appreciated that there was no case for forbearance in this respect, because late submission or non-submission could also be with an intention of beating the rating process particularly when bank could have deteriorated in its performance. The Committee felt that non-receipt of data in time from a bank should earn it a straight downgrade of rating by a notch and accordingly a higher premium be charged at the corresponding rate. (Recommendation 8) Rating of New Members and Merged entities 3.14 As per the Section 11 of the DICGC Act 1961, it is mandatory for the Corporation to admit any new bank as its member under deposit insurance system soon after it is granted license under Section 22 of the Banking Regulation Act, 1949. A bank, which has just been licensed, will not have financial history required for rating it for deposit insurance premium purposes. The Committee therefore decided that such a bank may be assigned a premium category corresponding to a ‘base premium rate’ (delineated in paragraph 3.17 below) till it produces its first annual financial accounts at the first annual accounting date (i.e. 31 March) after the commencement of operations. (Recommendation 9) 3.15 There are also instances when an existing member entity merges with another bank and loses its own identity. As per the current deposit insurance regulations, the merging entity is required to clear its premium liability upto the date of its deregistration and thereafter the bank taking over owes the insurance premium liability on the deposits of the merged bank. With the flat rate premium, the application of premium rates, pre and post merger, would not raise any issue. Under Differential Premium System however, it is likely that the two entities may be subject to application of different premium rates. In this situation, the Committee recommends that while the merging entity will discharge its liability upto he date of deregistration at the premium rates applicable to it, post merger the bank taking over would continue to pay the premium at a rate as applicable to it (till the next reset). (Recommendation 10) Building in the Incentives 3.16 The Committee recognised the role of a rating system as a tool for incentivising the good performance and as an instrument to encourage lower rated banks to strive towards improving their ratings. For building incentives in favour of better rating and dis-incentivising worse rating, Committee’s view was that the premium rates should move along the rating ladder in geometric/curvilinear progression rather than arithmetic/linear progression. (Recommendation 11) 3.17 The Committee also looked two possible approaches to scale the premium rates along the rating ladder. One process could be to assign the premium rates as a multiple of a base premium rate - multiples changing as per the rating; and the other to assign the absolute premium rates differentiated based on the rating of banks. It was felt that either of the systems would have same results. For operationalizing, the Committee felt that the Corporation could have a “base premium rate” and the effective premium rate might be derived by multiplying the base rate by a multiple (a Multiplicative Factor) representing rating. For example, the base premium rate could be 10 paise (the current premium rate per annum per hundred of Indian Rupees) and multiple for a top category bank could be .95, resulting in effective premium of 9.5 paise. While the multiples may remain unchanged, the revisions in the effective premium rates could be achieved through the variations in the base premium rate. The effective premium rate would progress along the rating scale on a convex curve, as presented in Chart 1: Chart 1: Relationship between the Risk Rating and the Premium Rate Discovering Premium Rates Across the Rating Scale 3.18 A Deposit Insurance Agency requires funds to be accumulated in a fund account usually referred to as Deposit insurance Fund, to meet its insurance obligations to the insured depositors in the event of bank failure. Identifying the funding requirements for meeting insurance obligations and instituting a sound funding arrangement for meeting those requirements are critical for the effectiveness of a Deposit Insurance System. The funding requirements are usually representative of the probability of a net loss on portfolio basis that a deposit insurance agency could have to suffer on account of its insurance liabilities. This requirement is termed generally as Target Reserve Ratio (Reserve Ratio is defined as the ratio of Deposit Insurance Fund (DIF) to the Insured Deposits). The DIF fund is built by way of surplus of premium payments by member banks on ex-ante basis, after meeting the operating expenses and payment of claims of depositors of insured failed banks. The Corporation, by regulation, is entitled to collect premium on ex-ante basis and is accordingly collecting the premium in advance. The Corporation has not yet set up a Target for Deposit Insurance Fund either absolute or in the form of Reserve Ratio. There are a good number of jurisdictions, which have set up Reserve Fund Targets for their deposit insurance operations, which vary from as low as 0.25% (Hong Kong) to 5% (Argentina)2. Internationally, the work is still on for refining the process of determining the size of Target Fund. IADI has set up a Sub Group under the aegies of Research and Guidance Committee for developing a Guidance Note for the IADI member institutions on setting up Target Fund. As of now, the Corporation is informally moving towards a Reserve Ratio of 2.5%. The Reserve ratio as on 31 March 2015 was 1.93%. The movement in the Reserve Ratio during the past 5 years is depicted in Chart 2.  3.19 Since the Corporation is still 57 basis points away from its informal target, in this context, one of the terms of reference of the Committee namely to recommend a matrix of premium rates for various rating categories in a manner as not to adversely affect the current premium inflows, is material. The Committee conducted a simulation exercise to discover the appropriate set of multiples of the base premium rate, at different scale points so that current premium inflows and their trends are preserved. The premium rate matrix corresponding to the different rating points is presented in Chapter 4. Frequency for resetting of rating and premium rates 3.20 The Corporation collects premium from the banks at half yearly frequencies, in advance. For example, for the insurance period of April - September of any year, the premium is collected during the April-May months with reference to the deposit base of immediate previous 31 March; and similarly for the October-March insurance period. Thus the Corporation collects the premium separately for two insured half-years based on two different deposit bases. Ideally, premium collection and risk premium assessment should go hand in hand, which would mean discovering the risk rating of each bank on a half yearly basis. The Committee deliberated on this aspect and felt that half yearly assessment of rating would be too onerous a task both for the Corporation and the member banks in terms of data submission by the banks and data collection and collation by the Corporation. Moreover, mid year data of a bank is usually audited under a limited review and therefore reliance thereon would be of limited value. The international practice too largely is that of an annual discovery. The Committee therefore decided to recommend rating assessment on an annual basis based on the annual audited data of the bank. (Recommendation 12) 3.21 The next action on hand was to decide on the correspondence between the time reference point for rating discovery and the insurance period for which the rating would be applicable. Taking a cue from the manner in which premium is collected and given the lag between the reference date for rating (i.e. 31 March) and completion of the process of rating discovery, the Committee felt that each year’s rating would apply to the prospective two half-year premium periods namely October – March and April - September. (Recommendation 13) 3.22 The Committee observed that the Corporation was collecting information for deposit insurance and premium purposes at half yearly intervals. Though the Committee had decided that rating calculation and premium reset should be an annual exercise, the Committee was not averse to obtaining information for the model’s inputs from the banks on a half yearly basis, to take advantage of the benefits accruing from tracking a bank’s performance in the context of a possible unexpected deterioration in its performance and consequent remedial action. Such an action would be of substantial value particularly in tracking the banks, which were in the lowest or second lowest rating category in the latest available rating. It therefore recommends that the MIS to be instituted for the rating purposes may have a half yearly frequency. (Recommendation 14) 3.23 The Committee also discussed the desirability of bringing in the pro-cyclicality to the premium rate reset under which, during the times of stability and growth , banks would be able to contribute to the insurance fund more liberally. Hence, the Corporation could strengthen the Insurance Fund during these times and could reduce the premium rates during the times of stress. The proposal however did not find favour for two reasons. One, determining of stressed periods and good periods for the financial sector would be subjective and hence may be subject to questioning. Second, during the good times, the devolvement of the Corporation’s liability would be less and correspondingly, net savings could improve, hence achieving the objective of strengthening the Insurance Fund during such times. The Committee therefore recommends that introduction of pro-cyclicality in the premium rates reset may not be considered. (Recommendation 15) Transparency and Confidentiality 3.24 The rating connotations can have a significant perceptive impact on the functioning and operations of a bank. Therefore, a bank is reasonably and legitimately entitled to know the rating process. The transparency also imparts credibility to the differential premium system as the transparency enhances accountability and sound management of the premium system. Further IADI Core Principle 9 recommends that differential premium should be transparent to all the participants. Therefore the balance between the confidentiality and transparency requires to be managed prudently. 3.25 The practice with different deposit insurance agencies is that at minimum a basic rating framework with input variables and their weights is disclosed to the banks at large. However a bank’s actual rating is shared with only the bank concerned, the latter being important as a disclosure of rating in public may have negative consequences for a bank such as fears of bank runs if the rating is low on the scale. 3.26 The Committee therefore was of the opinion that the Corporation should publish in public domain, the key characteristics of the rating model. (Recommendation 16) 3.27 The rating process and results, within the Corporation, would have to be managed with due care of confidentiality. In the world outside the Corporation, only the rated bank should know its rating. The Committee observed that the confidentiality safeguards adopted by the Reserve Bank with regard to their rating system could be looked at for instituting the confidentiality and usage requirements within the Corporation. (Recommendation 17) 3.28 Further, the Committee felt that the rated bank would ensure its rating’s confidentiality within the bank and that the rating is made known only to the important and key personnel within the bank. It was also indicated that the rating was for the specific purpose of assigning the premium rates and the rated bank would not use it for any other purpose, including canvassing for business or any type of capital funding. The member institutions should also be prohibited from disclosing the premium rate assigned to it, total score assigned or any score assigned to a member’s quantitative or qualitative factor(s) and any other information relating to rating the Corporation may decide to share with a member bank. (Recommendation 18) Transition to the new rating system 3.29 The transition to rating based premium, despite its immense value and benefits, could be painful not only to those banks which could fall in the high risk category and hence end with higher financial burden by way of higher premium, but also to others for fear of the possibility of being in the similar state on a future date. Therefore, success in the adoption of differential premium would depend on how well the transition is managed. The Committee deliberated on this aspect and came to a view that there should be adequate consultations on various aspects of the DPS, with the stakeholders viz. representative bodies of the member banks, supervisors and regulators and the government. Corporation would also need to draw up a clear transition plan which should explain transition objectives, responsibilities identified with the resource personnel within the Corporation and time table with deliverables and design an appropriate reporting system. The plan should also require communicating with the banks on the introduction of the differential premium, clarifying the policy rationale, explaining the benefits of such a system for the banks and giving a transition path including the lead time for preparing the banks to adopt the new system. (Recommendation 19) New Classes of Banks 3.30 Reserve Bank of India, as part of its policy to diversify the banking system and introduce banking classes with niche business models, has recently granted in principle approvals to certain entities and persons to set up ‘payment banks’. The Bank is also scrutinising applications for licenses under ‘small finance bank’ category and it is possible that some entities may be authorised to set up banks under this class too. The Corporation would need to revisit the proposed rating model for examining the format and applicability to these classes of banks as and when these banks start operating. (Recommendation 20) Periodic Review 3.31 The financial landscape is constantly evolving. The changing international and domestic regulations, supervisory practices, balance sheet compositions and banking products, and new tools of risk assessment; all lead to the changes in the risk profiles of the banks. The Committee also appreciated that capital standards for State Cooperative and District Central Cooperative Banks are still evolving. A substantive work on development of regulatory framework in response to 2008 financial crisis is still in progress. Such changes would require the premium system to be reviewed and updated in tune with the changing environment. Therefore, the Committee feels that as a good practice, the rating system be reviewed periodically, at a minimum of once in three years so that the rating system and methodology remain current and relevant. (Recommendation 21) References 1 General Guidance for Developing Differential Premium System, IADI (2011) 2 FSB Thematic Review on Deposit Insurance Systems (2012)

Chapter 4

Developing the Rating Model Introduction 4.1 As stated elsewhere in Chapter 3 of the Report, the Committee desired that the Rating Model for the banks be robust, simple and easy to understand. The important parameters based on which the banks in India have usually been subjected to rating process are both quantitative and qualitative. In Indian supervisory rating process, CAMELS approach has been used over a long period of time, which is currently being replaced by forward looking risk-based assessment in stages. Acronyms in CAMELS indicate respectively Capital Adequacy (signifying solvency), Asset Quality, Management Quality, Earnings, Liquidity and (Internal) Systems and Controls. Similar indicators have been used elsewhere in the world for rating of banks. 4.2 The Committee had a look at the sector structure of the banks insured by DICGC. The universe of insured banks in India comprise of public sector banks, private sector banks, Regional Rural Banks, Co-operative banks, local area banks and foreign banks (Chart 1). Chart 1: Sector Structure of Insured Banks in India 4.3 The banking system has three major categories of banks based on the mode of incorporation and ownership characteristics, namely, public sector banks, private sector banks and cooperative banks. The sub-categories within the major categories are closely similar. All the public sector banks, private sector banks (other than Local Area Banks (LABs)) , RRBs and State (Apex) Cooperative Banks are listed under Second schedule of the RBI Act 1934. Other banks in co-operative sector however are scheduled as well as non-scheduled. A scheduled status provides banks with certain privileges e.g. access to RBI’s liquidity window, subject to compliance with other eligibility criteria. 4.4 Indian banking sector is highly skewed. Although the number of banks with non-scheduled status far exceeds that of scheduled banks, the Indian banking sector is primarily under the domination of scheduled banks. Non-scheduled banks are small in size in terms of business, have a limited area of operation; many of them being single branch banks. Among the scheduled banks too, it is the Scheduled Commercial Banks (SCBs) i.e. other than RRBs that play the most important role. As on end March 2014, about 94 per cent of the banking business (deposits and credit) of all scheduled banks was with the SCBs. These banks therefore assume huge systemic significance for the Indian banking sector and thus for the Indian financial system. In view of the systemic importance of the SCBs in India, a brief analysis of risks assumed by these banks is presented below. The analysis is based on major financial parameters of these banks as per their audited annual accounts for the financial years ended March 2012, March 2013 and March 2014. Balance Sheet Analysis of SCBs Ownership pattern 4.5 SCBs comprise of State Bank of India and its associates (SBIA), nationalised banks (NB), private sector banks and foreign banks. SBIA and NBs are called public sector banks as major shares of these banks are held by the Government of India (GoI). A major part of the equity in private sector banks is held by private shareholders. Foreign Banks (FBs) are the branches of foreign banks having presence in India. There were 90 SCBs operating in India at end March 2014 of which 6 were SBIA, 21 were NBs, 20 private sector and 43 were FBs. Bank group wise share in major balance sheet items 4.6 NBs accounted for the majority shares in deposits and advances followed by SBIA. In respect of capital and reserves and surplus also NBs accounted for the major share followed by private sector banks. Regarding investments in government securities too, NBs accounted for the major share followed by near equal share by SBIA and private sector banks (Chart 2). Bank group Share in Income, Expenses and net Profit 4.7 NBs had major share in interest income followed by nearly equal share by SBIA and private sector banks (Chart 3). In case of other income, share of private sector banks came very close to that of NBs and remained significantly above that of SBIA and FBs. In case of expenses, SBIA and private sector banks performed almost equally well and their share in expenses remained noticeably lower to that of NBs (Chart 3). Share of private sector banks was the highest in net profit in 2013-14 and remained next to that of NBs that had the highest share in the previous two financial years. Bank group Share in NPAs 4.8 Share of NB was the highest in non-performing assets followed by SBIA (Chart 4). Adopting Risk Parameters 4.9 The Committee acknowledges that there are a myriad of parameters under which a financial institution could be evaluated for its risk. The Committee was of the view that for introduction of a Differential Premium System, it was enough to devise a protocol under which banks could be differentiated from one another for being placed in an inter-se order and to provide this as incentive for banks to avoid excessive risk taking. Therefore the model did not require a measurement and quantification of exact quantum of insurance risk in monetary value terms for each institution so as to get the DICGC compensated for that through premium. Against this background, the Committee decided to devise the rating model to be one akin to CAMELS model. As highlighted in Chapter 2, a good number of Deposit Insurance Agencies (DIAs) too have deployed some elements of CAMELS model in rating the insured institutions. Prominent elements among them are Solvency, Profitability, Asset Quality and Liquidity. Some DIAs have used additionally Supervisory Inputs to capture qualitative aspects, which have been sourced under information sharing arrangements between the DIAs and the supervisors. The Committee was aware of the limitations on the availability of supervisory ratings as an input in India. It therefore decided to propose the following parameters to be used as model inputs: -

Capital Adequacy and quality of its composition (weight 25%), -

Asset Quality (weight 25%), -

Profitability (weight 20%) -

Liquidity (weight 20%), and -

Other information (weight 10%)

(Recommendation 22) 4.10 A brief detail of the significance of each of these indicators is presented below. (a) Capital Adequacy and quality of its composition The use of capital as a primary risk differentiation measure is intended to provide greater protection for the deposit insurance fund by recognising capital’s role in cushioning against losses, and bringing in owner’s stake in ensuring sound operations. Therefore it was decided to include the following risk factors under capital adequacy viz. capital to risk weighted asset ratio (CRAR) and the presence of Tier I Capital. While, CRAR reflects the overall soundness of the bank, the level and nature of Tier I capital helps to assess the quality of the capital. The scheduled commercial banks other than RRBs have been brought under the Basel III regime under a transition arrangement (Table 1) while rest of the banks are still subjected to Basel I norms. It may be added that State and District Central Cooperative Banks are being brought under the Capital Adequacy of 9% (as applicable to other banks under Basel I) by March 2017. It is observed from the Table that the composition of Capital Ratios under Basel III is materially different from that under Basel I. While under Basel I, Tier 2 Capital cannot be more than 100% of tier I Capital, Basel III, requires the banks to have as on April 31, 2014 a Tier I share not below 6.5% points in Capital ratio of 9% points. This difference would reflect in the evaluation of the quality of capital as part of rating model. | Table 1: Transitional Arrangements under BASEL III-Scheduled Commercial Banks (excluding LABs and RRBs) | | (% of RWAs) Minimum capital ratios | April 1,

2013 | March

31, 2014 | March

31, 2015 | March

31, 2016 | March

31, 2017 | March

31, 2018 | March

31, 2019 | | Minimum Common Equity Tier 1 (CET1) | 4.5 | 5 | 5.5 | 5.5 | 5.5 | 5.5 | 5.5 | | Capital conservation buffer (CCB) | - | - | - | 0.625 | 1.25 | 1.875 | 2.5 | | Minimum CET1+ CCB | 4.5 | 5 | 5.5 | 6.125 | 6.75 | 7.375 | 8 | | Minimum Tier 1 capital | 6 | 6.5 | 7 | 7 | 7 | 7 | 7 | | Minimum Total Capital | 9 | 9 | 9 | 9 | 9 | 9 | 9 | | Minimum Total Capital +CCB | 9 | 9 | 9 | 9.625 | 10.25 | 10.875 | 11.5 | | Phase-in of all deductions from CET1 (in %) | 20 | 40 | 60 | 80 | 100 | 100 | 100 | (b) Asset Quality For asset quality, it was decided to use the following risk factors related to non-performing assets viz. the percentage of Gross NPAs to Gross Advances to reflect overall asset quality, percentage of Net NPAs to Net Advances to assess the strength of balance sheet based on the provisions made for NPAs and share of sub-standard advances in Gross NPAs which is indicative of quality of NPAs in terms of higher probability of NPA movement into standard category. (c) Liquidity For this factor, the Committee decided to have model inputs based on share of term deposits in total deposits and the ratio of liquid assets to total deposits and borrowings. The consideration for term deposits is based on the assumption that term deposits provide funding stability and technically their repayment in case of bank failure can be deferred till their maturity thus helping the Deposit Insurance Agency to manage its liquidity. Therefore higher the share of term deposit, the better from the perspective of a DIA. As regards liquidity on the balance sheet, the Committee held the view that all market assets and the assets maturing within one month would denote liquidity. The Committee accordingly decided that the liquid assets would consist of cash and bank balances (including balances with RBI), monies placed with counterparties (interbank) and maturing within one month, and investments in government securities. In a typical state of bank liquidation, these assets would generate cash more easily. Therefore, higher the share of such assets, more liquid is the balance sheet. (d) Earnings Performance under the earnings parameters provides a useful insight into a member bank’s potential to sustain its capital ratios. Under earnings, three risk factors were selected viz. Return on Assets (RoA), cost to income ratio and Net Interest Margin (NIM). RoA will be compiled as percentage ratio of profit after tax to average total assets and is indicative of the productivity of assets. Cost to income ratio, is defined as percentage ratio of operating expenses to total of net interest income plus non-interest income and reflects the degree of efficiency of expense management. Lastly the NIM depicts pricing efficiency of liabilities and assets. It also captures the adverse effect of NPAs as they generate no interest income. A higher margin reflects a better acceptance of the bank by the public and the businesses. (e) Other Information It will include such risk factors that are not covered above. These risk factors may be related to state of adoption of technology, access to Reserve Bank funding, regulatory penalties, DICGC’s own assessment of a member bank in compliance with various deposit insurance related requirements, etc. 4.11 Based on the quality/significance of the different indicators, the Committee decided to allot Reward Points (RPs) to each bank and aggregate them to arrive at the overall score. Proposing a Model Framework of the model 4.12 The Committee decided to build a model based on the risk factors proposed earlier and called it Comprehensive Risk Assessment Module (CRAM). For each risk factor, a bank is given a Reward Point based on the risk assumed in respect of that risk factor. A bank will get a higher RP for lower risk exposure. The framework of the model is presented below (Table 2). (Recommendation 23) | Table 2: Framework of the Comprehensive Risk Assessment Module (CRAM) | | Risk factors | Reward point (RP) | 1. Solvency | 0 - 25 | | of which | | | (i) CRAR (in %) | 0 -15 | | (ii) Quality of capital | 0 - 10 | | (a) For SCBs: Tier I capital ratio (other than RRBs) (%) | | | (b) For RRBs, LABs and Cooperative banks: Tier I to Tier II ratio | | | 2. Asset quality | 0 - 25 | | of which | | | (i) Ratio of Gross NPAs to Gross advances (in %) | 0 - 12 | | (ii) Ratio of net NPA to net Advances (in %) | 0 - 8 | | (iii) Ratio of Sub-standard assets to Gross NPAs (in %) | 0 - 5 | | 3. Liquidity | 0 - 20 | | (i) Liquid assets [cash in hand, balance with RBI, balances with banks, money at call & short notice, market value of government securities held (in India)] to total of deposits & borrowings (in %); | 0 - 15 | | (ii) Ratio of term deposits to total deposits (%) | 0 - 5 | | 4. Profitability | 0- 20 | | of which | | | (i) Return on Assets (PAT to Total Average Assets) (in %) | 0 -10 | | (ii) Cost to income ratio (in %) | 0 - 5 | | (iii) Net Interest Margin (in %) | 0 - 5 | | 5. Miscellaneous | 0 - 10 | | Access to RBI liquidity support, state of technology adoption, regulatory penalties, and compliance with DICGC’s various requirements, etc. | 0 - 10 | | Total | 0 - 100 | Rules for assigning reward point 4.13 The rules for assigning RP for each of the risk factors outlined with the exception of the ‘other information’ are presented below (Tables 3, 4 and 5). (Recommendation 24) | Table 3: Rules for Assigning RPs: Solvency | | 1. Solvency | | CRAR | For SCBs only | For RRBs, LABs, and Cooperative Banks only | | (i) CRAR(%) | RP | (ii) Tier 1 capital(%) | RP | (ii) Tier 1 to tier 2 ratio$ | RP | | <6 | 0 | < 5.0 | 0 | | | | ≥6 but < 7 | 6 | ≥ 5.0 but < 5.5 | 1 | ≥1.0 but <1.2 | 4 | | ≥7 but <8 | 7.5 | ≥5.5 but < 6.0 | 3 | ≥1.2 but <1.4 | 6 | | ≥8 but < 9 | 9.0 | ≥ 6.0 but < 6.5 | 5 | ≥1.4 but <1.6 | 8 | | ≥9 but <10 | 10.5 | ≥6.5 but <7.0 | 7 | ≥ 1.6 | 10 | | ≥10 but <11 | 12.0 | ≥7.0 but <7.5 | 9 | | | | ≥11 but <12 | 13.5 | ≥ 7.5 | 10 | | | | ≥12 | 15 | | | | | | $ banks can not have this ratio below 1; | It may be observed that though the minimum CRAR prescribed is 9%, a CRAR level below the minimum prescribed too has value from the solvency perspective. Therefore, the Committee considers that a CRAR below 6% maximises the risk and consequently minimises the RPs. | Table 4: Rules for Assigning RPs: Asset quality | | 2. Asset Quality | | (i) Ratio of GNPAs to Gross Advances (%)* | RP | (ii) Ratio of net NPA to net Advances (%) | RP | (iii) Ratio of Sub-standard assets to GNPAs (%) | RP | | >=8 | 0 | >= 2.7 | 0 | < 50 | 0 | | ≥7 but < 8 | 1.5 | ≥2.4 but <2.7 | 1 | ≥50 but <55 | 1 | | ≥6 but < 7 | 3 | ≥2.1 but <2.4 | 2 | ≥55 but <60 | 2 | | ≥5 but < 6 | 4.5 | ≥1.8 but < 2.1 | 3 | ≥60 but <65 | 3 | | ≥4 but < 5 | 6 | ≥1.5 but <1.8 | 4 | ≥65 but <70 | 4 | | ≥3 but < 4 | 7.5 | ≥1.2 but < 1.5 | 5 | ≥ 70 | 5 | | ≥2 but < 3 | 9 | ≥0.9 but <1.2 | 6 | | | | ≥1 but < 2 | 10.5 | ≥0.6 but < 0.9 | 7 | | | | < 1 | 12 | < 0.6 | 8 | | |