During 2020-21, scheduled commercial banks (SCBs) reported a discernible improvement in their asset quality, capital buffers and profitability, notwithstanding the disruptions of the pandemic. While credit offtake remained subdued, elevated deposit growth on the liabilities side was matched by growth in investments on the assets side. Nonetheless, incipient stress remains in the form of higher restructured advances. Banks would need to bolster their capital positions to absorb potential stress as well as to augment credit flow when policy support is phased out. 1. Introduction IV.1 During 2020-21, the banking sector navigated the disruptions caused by the pandemic and the economic downturn with resilience, cushioned by various policy measures undertaken by the Reserve Bank and the Government. Asset quality improved, partly attributable to imposition of the asset classification standstill. Public sector banks (PSBs) reported net profits after a gap of five years. More generally, the capital position of banks improved, aided by recapitalisation by the government as well as raising of funds from the market. Nonetheless, incipient stress remains in the form of increased proportion of restructured advances and the possibility of higher slippages arising from sectors that were relatively more exposed to the pandemic. Nevertheless, with the green shoots of recovery re-emerging in H1:2021-22, banks are expected to further shore up their financials. IV.2 Against this background, this chapter discusses the operations and performance of the banking sector during 2020-21 and H1:2021-22. Balance sheet developments are analysed in Section 2, followed by an assessment of their financial performance and financial soundness in Sections 3 and 4, respectively. Sections 5 to 12 address specific themes relating to sectoral deployment of credit, performance of banking stocks, ownership patterns, corporate governance and compensation practices, foreign banks’ operations in India and overseas operations of Indian banks, developments in payments systems, consumer protection and financial inclusion. Developments related to regional rural banks (RRBs), local area banks (LABs), small finance banks (SFBs) and payments banks (PBs) are analysed separately in Sections 13 to 16. The chapter concludes by bringing together major issues that emerge from the analysis and offers some perspectives on the way forward. 2. Balance Sheet Analysis IV.3 The consolidated balance sheet of scheduled commercial banks (SCBs) accelerated during 2020-21, notwithstanding the pandemic and the contraction in economic activity in the first half of the year. Deposit growth on the liabilities side was matched by investments on the assets side; however, credit offtake remained subdued (Table IV.1 and Chart IV.1). Supervisory data suggest that while nascent signs of recovery are visible in credit growth, deposit growth has slowed down in 2021-22 so far. IV.4 The share of PSBs in total advances as well as in deposits has been declining since 2010-11, while private sector banks (PVBs) have been improving their share. Table IV.1: Consolidated Balance Sheet of Scheduled Commercial Banks

(At end-March) | | (Amount in ₹ crore) | | Item | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks | Payments Banks | All SCBs | | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | | 1. Capital | 72,040 | 59,328 | 26,866 | 30,641 | 85,710 | 91,465 | 5,151 | 5,375 | 1,035 | 1,300 | 1,90,802 | 1,88,109 | | 2. Reserves and Surplus | 5,80,886 | 6,49,142 | 5,81,749 | 7,07,345 | 1,08,987 | 1,24,706 | 11,047 | 14,800 | -461 | -704 | 12,82,208 | 14,95,289 | | 3. Deposits | 90,48,420 | 99,00,766 | 41,59,044 | 48,00,646 | 6,84,239 | 7,77,173 | 82,488 | 1,09,472 | 855 | 2,543 | 1,39,75,045 | 1,55,90,600 | | 3.1. Demand Deposits | 5,71,383 | 6,84,451 | 5,47,521 | 6,82,095 | 2,17,825 | 2,37,412 | 2,381 | 3,964 | 8 | 19 | 13,39,118 | 16,07,941 | | 3.2. Savings Bank Deposits | 30,41,902 | 34,62,923 | 11,72,739 | 14,56,019 | 70,007 | 87,032 | 10,284 | 22,198 | 847 | 2,524 | 42,95,779 | 50,30,696 | | 3.3. Term Deposits | 54,35,134 | 57,53,392 | 24,38,784 | 26,62,532 | 3,96,408 | 4,52,729 | 69,823 | 83,310 | - | - | 83,40,149 | 89,51,963 | | 4. Borrowings | 7,09,780 | 7,18,850 | 8,27,575 | 6,25,683 | 1,28,761 | 1,02,331 | 30,004 | 27,828 | - | 198 | 16,96,120 | 14,74,890 | | 5. Other Liabilities and Provisions | 3,71,706 | 4,03,292 | 2,36,890 | 2,66,732 | 2,57,381 | 1,68,893 | 4,057 | 6,076 | 216 | 737 | 8,70,250 | 8,45,729 | | Total Liabilities/Assets | 1,07,82,831 | 1,17,31,378 | 58,32,123 | 64,31,048 | 12,65,079 | 12,64,567 | 1,32,747 | 1,63,552 | 1,645 | 4,072 | 1,80,14,425 | 1,95,94,617 | | | (59.9) | (59.9) | (32.4) | (32.8) | (7.0) | (6.5) | (0.7) | (0.8) | (0.0) | (0.0) | (100.0) | (100.0) | | 1. Cash and balances with RBI | 4,36,774 | 5,39,149 | 2,72,616 | 2,92,019 | 51,238 | 59,163 | 5,058 | 6,921 | 33 | 174 | 7,65,720 | 8,97,426 | | 2. Balances with banks and money at call and short-notice | 4,66,615 | 5,93,721 | 2,12,324 | 2,73,711 | 99,468 | 1,51,549 | 8,701 | 12,309 | 455 | 812 | 7,87,563 | 10,32,102 | | 3. Investments | 29,40,636 | 34,00,895 | 12,93,031 | 15,12,480 | 4,31,277 | 4,73,418 | 24,203 | 30,660 | 694 | 2,413 | 46,89,842 | 54,19,866 | | 3.1 In Government Securities (a+b) | 24,09,182 | 27,89,985 | 10,66,313 | 12,57,222 | 3,84,102 | 4,30,779 | 20,748 | 27,142 | 694 | 2,412 | 38,81,039 | 45,07,541 | | a) In India | 23,71,783 | 27,52,716 | 10,57,074 | 12,36,747 | 3,62,540 | 3,90,195 | 20,748 | 27,142 | 694 | 2,412 | 38,12,839 | 44,09,212 | | b) Outside India | 37,399 | 37,270 | 9,240 | 20,476 | 21,562 | 40,584 | - | - | - | - | 68,201 | 98,329 | | 3.2 In Other Approved Securities | 102 | 12 | - | - | - | - | - | - | - | - | 102 | 12 | | 3.3 In Non-Approved Securities | 5,31,352 | 6,10,898 | 2,26,718 | 2,55,258 | 47,175 | 42,639 | 3,455 | 3,518 | - | 1 | 8,08,700 | 9,12,313 | | 4. Loans and Advances | 61,58,112 | 63,48,758 | 36,25,154 | 39,39,292 | 4,28,076 | 4,23,546 | 90,554 | 1,08,613 | - | 0.1 | 1,03,01,897 | 1,08,20,208 | | 4.1 Bills purchased and discounted | 1,60,977 | 1,45,894 | 1,25,111 | 1,19,295 | 59,273 | 60,380 | 37 | 124 | - | - | 3,45,398 | 3,25,694 | | 4.2 Cash Credits, Overdrafts, etc. | 24,16,408 | 24,91,776 | 9,70,317 | 10,11,497 | 2,07,717 | 1,75,337 | 6,872 | 8,861 | - | - | 36,01,314 | 36,87,471 | | 4.3 Term Loans | 35,80,727 | 37,11,087 | 25,29,726 | 28,08,501 | 1,61,085 | 1,87,828 | 83,646 | 99,628 | - | 0.1 | 63,55,184 | 68,07,043 | | 5. Fixed Assets | 1,06,507 | 1,06,826 | 38,268 | 39,713 | 4,129 | 4,457 | 1,671 | 1,676 | 200 | 222 | 1,50,775 | 1,52,894 | | 6. Other Assets | 6,74,187 | 7,42,030 | 3,90,729 | 3,73,832 | 2,50,891 | 1,52,434 | 2,559 | 3,373 | 263 | 452 | 13,18,629 | 12,72,121 | Notes: 1. -: Nil/negligible.

2. Components may not add up to their respective totals due to rounding-off numbers to ₹ crore.

3. Detailed bank-wise data on annual accounts are collated and published in Statistical Tables Relating to Banks in India, available at https://www.dbie.rbi.org.in.

4. Figures in parentheses are shares in total assets/ liabilities of different bank groups in all SCBs.

Source: Annual accounts of respective banks. | 2.1 Liabilities IV.5 During 2020-21, deposit mobilisation by SCBs was the highest in seven years, mainly contributed by the low-cost current account and savings account (CASA) deposits (Chart IV.4). In H1:2021-22, there was a moderation in deposit growth with normalisation of economic activity and rising inflation. IV.6 For the last three years, private non-financial corporations have been net savers, progressively increasing their deposits with SCBs while their credit offtake has remained anaemic. Moreover, the household sector’s deposits—64 per cent of the total as at end-March 2021—also picked up pace (Chart IV.2). IV.7 With term deposit rates falling across the board, their growth moderated during 2020-21 (Chart IV.3a). Correspondingly, their distribution across interest rates shifted leftwards, with 5-6 per cent interest rate emerging as the modal class (Chart IV.3b). IV.8 Historically, PVBs have relied heavily on borrowings to supplement their deposits and fuel credit growth. On the other hand, PSBs leveraged their wide deposit base and availability of low-cost CASA deposits to fund their lending. In 2020-21, borrowings of PVBs contracted for the first time since 2016-17, while those of PSBs accelerated after contracting for two consecutive years. Despite robust CASA deposit growth, PSBs raised higher resources through borrowings than the previous year as their credit growth accelerated over the first three quarters of the year (Chart IV.5).

2.2 Assets IV.9 SCBs’ credit growth has decelerated over previous two years, largely reflecting muted demand conditions and risk aversion (Box IV.1). Signs of recovery became visible in H1:2021-22. Box IV.1: Slowdown in Credit Growth: Supply or Demand Driven? Persistent anemic credit growth in recent years has led to a vigorous debate amongst policymakers and analysts on the underlying causes. In the presence of asymmetric information, stickiness of loan interest rates leads to delays in price adjustments. In the interim, there can be disequilibrium whenever supply does not equal demand at the prevailing interest rate (Stiglitz and Weiss, 1981). The observed credit Ct is assumed to be the minimum of the estimated demand for credit (Ctd) and estimated supply for credit (Cts): The disequilibrium model is estimated by using the maximum likelihood method (MLE). The model facilitates determination of probabilities with which each observation belongs to either the demand or supply equation (Maddala and Nelson, 1974). Using monthly data for the period April 2001-March 2020, the disequilibrium model is estimated for India. The benchmark prime lending rate (BPLR) of State Bank of India is taken as a proxy for the market clearing interest rate, while the logarithm of credit is taken as dependent variable. The results suggest that the slowdown in credit is reflecting a scissors effect. Industrial activity (IIP) and investment (GFCF) constrained credit demand, while stressed balance sheets of banks2 limited credit supply (Table 1). Hence, policies aimed at boosting aggregate demand need to be supplemented with strengthening bank balance sheets to reduce stress for a sustainable boost to credit growth. | Table 1: Estimation Results | | Explanatory variables/Dependent variables | Log Credit

(Model 1) | Log Credit

(Model 2) | Explanatory variables/Dependent variables | Log Credit

(Model 1) | Log Credit

(Model 2) | | Credit Demand | Credit Supply | | Constant | 0.1339*** (0.0114) | 5.6117*** (0.036) | Constant | 0.0008 (0.0083) | -2.5247*** (0.0063) | | BPLR_lag 1 | 0.6222*** (0.0114) | 2.8388*** (0.037) | Time trend | -0.00004 (0.00002) | -0.0013*** (0.00005) | | Time trend | 0.0021 (0.0022) | -0.0004 (0.001) | SAR_lag1 | -0.0006 (0.0009) | -0.0062** (0.0029) | | GFCF_lag 1 | | 0.0253** (0.0129) | CRAR_lag2 | 0.0006 (0.0011) | | | IIP_lag 1 | 0.1488*** (0.0014) | | Log_deposit_lag 2 | | 1.4017*** (0.0124) | | IIP_lag 2 | | 0.0151 (0.019) | Cost of Fund_lag 1 | 0.0009 (0.0009) | | | Sensex growth | 0.0287 (0.0177) | | BPLR_lag 2 | 0.0008 (0.0009) | -0.1051 (0.0807) | | CPI Inflation_lag 1 | 0.9217*** (0.0003) | | AQR Dummy | 0.0020 (0.0023) | -0.0249*** (0.0077) | | BPLR_lag 2 | -0.5351*** (0.0114) | -1.4109*** (0.0373) | St. Dev. of demand equation error | 1.1380*** (0.0005) | 0.6042*** (0.0405) | | AQR dummy | | 0.6648*** (0.0065) | St. Dev. of supply equation error | 0.0073*** (0.00001) | 0.0256*** (0.0001) | | GFC Dummy | -0.2900*** (0.0002) | | Log-likelihood | 1114.16 | -658.63 | Note: 1. AQR: Asset Quality Review; GFC: Global Financial Crisis; IIP: Index of Industrial production; GFCF: Gross Fixed Capital Formation.

2. lag 1: lagged by one period; lag 2: lagged by two periods.

3. ***, **, and * indicate 1 per cent, 5 per cent and 10 per cent levels of significance, respectively.

4. Figures in parenthesis are standard errors. | References: Maddalla, G. S., and F. Nelson. 1974. Maximum Likelihood Methods for Models of Markets in Disequilibrium. Econometrica 42(6): 1013–1030. Stiglitz, Joseph E.; Weiss, Andrew (1981). Credit Rationing in Markets with Imperfect Information”. The American Economic Review. 71 (3): 393–410. Verma, R (2021). Slowdown in Credit Flow in India: Supply or Demand Driven, mimeo. | IV.10 Credit growth of PVBs decelerated from Q4: 2019-20 till Q3:2020-21 as the pandemic took its toll. Since Q4:2020-21, however, PVBs’ credit showed signs of revival (Chart IV.6). IV.11 Within population groups, the relatively higher credit growth to rural and semi-urban areas after the outbreak of COVID-19 is a bright spot (Chart IV.7). While PSBs remained the major contributor of rural lending, given their reach and accessibility, the share of PVBs has also climbed up.

IV.12 The credit-to-GDP ratio increased to a five-year high, narrowing the credit-GDP gap (Chart IV.8a). India’s credit-to-GDP ratio is still markedly lower than the G20 average (Chart IV.8b). IV.13 As the share of advances in total assets fell, that of investments increased in an environment of risk aversion and limited profitable lending avenues. This resulted in a decline in the credit-deposit (C-D) ratio and a corresponding elevation in the investment-deposit (I-D) ratio, especially in incremental terms (Chart IV.9). IV.14 Central Government and State Government securities were preferred by both PSBs and PVBs during 2020-21, indicating their preference for safer investments. Consequently, the share of other debt securities in PSBs’ total portfolio declined after increasing for three consecutive years (Chart IV.10). 2.3 Maturity Profile of Assets and Liabilities IV.15 Mismatches in the maturity of assets and liabilities are intrinsic to banking business, but they have implications for liquidity, profitability and risk exposures. During 2020-21, while the negative gap in the maturity bucket of up to one year moderated, the positive gap in the maturity bucket of more than five years turned negative as banks attracted less short-term CASA deposits and more longer-term deposits (Chart IV.11).

IV.16 In the case of borrowings, PSBs and PVBs displayed widely contrasting patterns. The share of short-term and long-term borrowings increased year-on-year in the case of PSBs, while PVBs relied more on borrowings with maturity between one and five years (Table IV.2). 2.4 International Liabilities and Assets IV.17 The total international liabilities of banks located in India expanded in 2020-21 on the back of rupee denominated deposits and equities held by non-resident Indians (NRIs) (Appendix Table IV.9). The sizeable increase in international assets, on the other hand, was led by their loans and debt securities (Appendix Table IV.10). However, international assets of banks in India (including foreign banks) were only 42 per cent compared to their international liabilities (Chart IV.12a). IV.18 During the period under review, the share of claims of Indian banks (including their domestic and foreign branches) shifted away from non-financial private institutions and favoured other banks (Appendix Table IV.11 and Chart IV.12b). The country-composition of international claims remained stable, with the share of the top five out of six countries against which Indian banks held the highest share of claims increasing further (Appendix Table IV.12). Table IV.2: Bank Group-wise Maturity Profile of Select Liabilities /Assets

(At end-March) | | (Per cent) | | Assets/Liabilities | PSBs | PVBs | FBs | SFBs | PBs | All SCBs | | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | | I. Deposits | | | | | | | | | | | | | | a) Up to 1 year | 40.4 | 36.2 | 38.1 | 34.3 | 63.9 | 62.4 | 59.6 | 53.6 | 10.0 | 13.0 | 40.9 | 37.0 | | b) Over 1 year and up to 3 years | 22.8 | 21.9 | 28.1 | 28.9 | 28.3 | 30.8 | 37.5 | 42.1 | 90.0 | 87.0 | 24.8 | 24.7 | | c) Over 3 years and up to 5 years | 10.2 | 11.3 | 8.5 | 9.2 | 7.7 | 6.7 | 0.7 | 1.7 | - | - | 9.5 | 10.3 | | d) Over 5 years | 26.6 | 30.6 | 25.3 | 27.7 | 0.0 | 0.0 | 2.2 | 2.6 | - | - | 24.7 | 28.0 | | II. Borrowings | | | | | | | | | | | | | | a) Up to 1 year | 49.2 | 54.5 | 51.7 | 41.4 | 83.4 | 83.8 | 41.1 | 46.9 | - | 100.0 | 52.9 | 50.8 | | b) Over 1 year and up to 3 years | 27.5 | 21.0 | 24.2 | 34.0 | 10.3 | 11.8 | 44.0 | 37.3 | - | - | 24.9 | 26.2 | | c) Over 3 years and up to 5 years | 13.0 | 12.8 | 11.3 | 13.9 | 2.2 | 2.0 | 11.3 | 13.8 | - | - | 11.3 | 12.5 | | d) Over 5 years | 10.2 | 11.7 | 12.8 | 10.6 | 4.2 | 2.4 | 3.6 | 2.1 | - | - | 10.9 | 10.4 | | III. Loans and Advances | | | | | | | | | | | | | | a) Up to 1 year | 25.1 | 24.8 | 32.3 | 32.2 | 61.4 | 55.4 | 38.1 | 41.8 | - | 100.0 | 29.3 | 28.9 | | b) Over 1 year and up to 3 years | 40.9 | 36.9 | 33.6 | 34.1 | 19.3 | 22.7 | 42.4 | 34.0 | - | - | 37.4 | 35.3 | | c) Over 3 years and up to 5 years | 10.9 | 14.9 | 12.7 | 12.8 | 7.1 | 9.1 | 9.0 | 11.0 | - | - | 11.4 | 13.8 | | d) Over 5 years | 23.1 | 23.5 | 21.4 | 20.9 | 12.1 | 12.8 | 10.4 | 13.2 | - | - | 21.9 | 22.0 | | IV. Investments | | | | | | | | | | | | | | a) Up to 1 year | 23.7 | 23.7 | 54.2 | 50.6 | 83.4 | 85.1 | 59.0 | 58.1 | 100.0 | 97.4 | 37.8 | 36.8 | | b) Over 1 year and up to 3 years | 13.1 | 16.6 | 15.1 | 20.7 | 11.0 | 10.3 | 26.3 | 25.4 | - | 1.9 | 13.5 | 17.3 | | c) Over 3 years and up to 5 years | 10.6 | 13.2 | 6.8 | 6.5 | 2.0 | 2.2 | 3.1 | 2.9 | - | 0.4 | 8.7 | 10.3 | | d) Over 5 years | 52.7 | 46.4 | 23.8 | 22.2 | 3.6 | 2.4 | 11.6 | 13.6 | - | 0.2 | 40.0 | 35.6 | Notes: 1. - : Nil/Negligible.

2. The sum of components may not add up to 100 due to rounding off.

Source: Annual accounts of banks. | 2.5 Off-Balance Sheet Operations IV.19 The size of contingent liabilities of all SCBs relative to their total on-balance sheet exposures declined in 2020-21, after increasing in the previous year. For PSBs, however, the share increased as their forward exchange contracts that include all admissible derivative products increased by more than 40 per cent. For FBs, while off-balance sheet exposures decreased, they remained more than nine times their total liabilities (Chart IV.13). The overall deceleration in banks’ contingent liabilities was on account of muted growth in their forward exchange contracts in line with subdued foreign exchange transactions (Appendix Table IV.2).

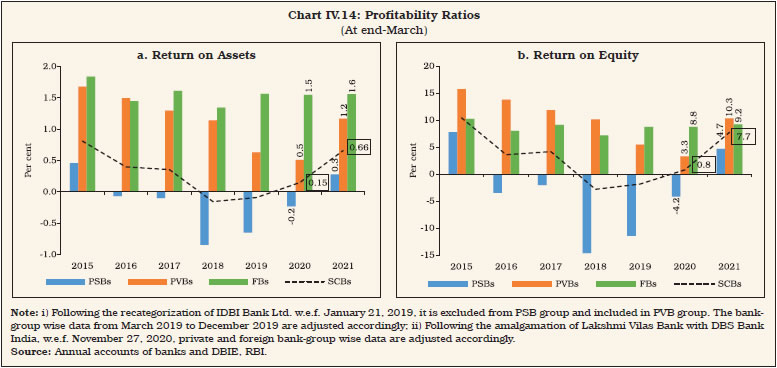

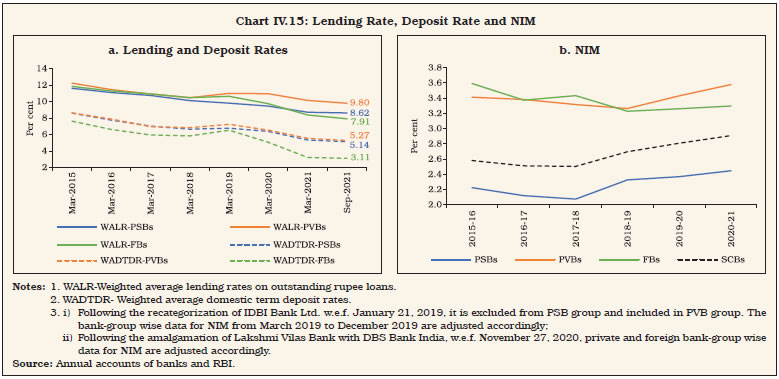

3. Financial Performance IV.20 The financial performance of SCBs in 2020-21 was marked by a discernible increase in profitability as their income remained stable but expenditure declined. This was in sharp contrast with the past five years during which PSBs incurred losses and profitability of PVBs was declining (Chart IV.14). IV.21 The total income of banks remained stable, despite a marginal decline in its largest component viz. interest income, in an environment characterised by low credit offtake and interest rates (Table IV.3). The fall was cushioned by a sizeable increase in income from investments. Income from trading also accelerated, as banks booked profits on falling G-Sec yields. IV.22 The contraction in SCBs’ expenditure was led by a decline in the interest expended on deposits and borrowings on account of moderation in interest rates and contraction in total borrowings. Across bank groups, the transmission of policy rate changes to term deposit rates was highest for FBs (Chart IV.15 a). At the system level, interest earned by banks outpaced their interest expenses, and hence the net interest margin (NIM) improved (Chart IV.15 b).

| Table IV.3: Trends in Income and Expenditure of Scheduled Commercial Banks | | (Amount in ₹ crore) | | Item | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks | Payments Banks | All SCBs | | 2019-20 | 2020-21 | 2019-20 | 2020-21 | 2019-20 | 2020-21 | 2019-20 | 2020-21 | 2019-20 | 2020-21 | 2019-20 | 2020-21 | | 1. Income | 8,34,320 | 8,31,882 | 5,46,347 | 5,45,833 | 83,223 | 82,081 | 19,219 | 22,500 | 55 | 1,004 | 14,83,164 | 14,83,301 | | | (7.6) | (-0.3) | (17.0) | (0.4) | (19.1) | (-4.3) | (76.4) | (17.1) | - | (1733.7) | (12.1) | (0.01) | | a) Interest Income | 7,16,203 | 7,07,092 | 4,49,006 | 4,51,617 | 66,673 | 63,888 | 16,948 | 19,523 | 46 | 101 | 12,48,876 | 12,42,222 | | | (5.1) | (-1.3) | (14.1) | (1.1) | (20.0) | (-7.2) | (75.0) | (15.2) | - | (120.1) | (9.5) | (-0.5) | | b) Other Income | 1,18,117 | 1,24,790 | 97,341 | 94,216 | 16,550 | 18,193 | 2,271 | 2,976 | 9 | 903 | 2,34,288 | 2,41,079 | | | (26.0) | (5.6) | (32.6) | (-2.9) | (15.5) | (7.6) | (86.7) | (31.1) | - | (9932.3) | (28.2) | (2.9) | | 2. Expenditure | 8,60,335 | 8,00,064 | 5,27,236 | 4,76,357 | 67,043 | 63,116 | 17,251 | 20,462 | 389 | 1,304 | 14,72,253 | 13,61,303 | | | (2.2) | (-7.0) | (20.0) | (-9.1) | (21.0) | (-10.4) | (75.7) | (18.6) | - | (235.5) | (9.3) | (-7.5) | | a) Interest Expended | 4,68,005 | 4,31,627 | 2,58,038 | 2,32,555 | 28,810 | 21,769 | 7,928 | 9,122 | 14 | 55 | 7,62,794 | 6,95,128 | | | (3.9) | (-7.8) | (11.6) | (-9.3) | (17.7) | (-28.8) | (74.8) | (15.1) | - | (307.7) | (7.3) | (-8.9) | | b) Operating Expenses | 1,92,720 | 2,02,879 | 1,26,663 | 1,30,456 | 21,584 | 22,318 | 7,152 | 7,549 | 488 | 1,251 | 3,48,607 | 3,64,453 | | | (10.1) | (5.3) | (15.9) | (3.6) | (15.4) | (-0.3) | (70.3) | (5.6) | - | (156.6) | (13.4) | (4.5) | | Of which : Wage Bill | 1,15,839 | 1,23,378 | 47,357 | 50,274 | 7,878 | 7,888 | 3,811 | 4,302 | 264 | 398 | 1,75,149 | 1,86,239 | | | (14.1) | (6.5) | (20.8) | (6.9) | (17.2) | (-4.0) | (79.2) | (12.9) | - | (50.6) | (17.1) | (6.3) | | c) Provision and Contingencies | 1,99,609 | 1,65,558 | 1,42,535 | 1,13,346 | 16,648 | 19,029 | 2,171 | 3,791 | -112 | -2 | 3,60,852 | 3,01,722 | | | (-7.7) | (-17.1) | (44.1) | (-20.0) | (36.2) | (8.9) | (100.8) | (74.6) | - | | (9.9) | (-16.4) | | 3. Operating Profit | 1,73,594 | 1,97,376 | 1,61,646 | 1,82,823 | 32,829 | 37,994 | 4,139 | 5,829 | -446 | -302 | 3,71,763 | 4,23,720 | | | (16.0) | (13.7) | (27.8) | (13.1) | (22.8) | (15.8) | (91.4) | (40.8) | | | (21.9) | (14.0) | | 4. Net Profit | -26,015 | 31,818 | 19,111 | 69,477 | 16,180 | 18,965 | 1,968 | 2,038 | -334 | -300 | 10,911 | 1,21,998 | | | | | (-30.8) | (248.3) | (11.5) | (23.6) | (81.9) | (3.5) | | | | (1018.1) | | 5. Net Interest Income (NII) | 2,48,198 | 2,75,465 | 1,90,968 | 2,19,063 | 37,863 | 42,119 | 9,020 | 10,401 | 32 | 45 | 4,86,082 | 5,47,094 | | | (7.5) | (11.0) | (17.6) | (15.0) | (21.8) | (10.0) | (75.3) | (15.3) | - | (40.7) | (13.2) | (12.6) | | 6. Net Interest Margin (NIM) | 2.37 | 2.45 | 3.43 | 3.58 | 3.26 | 3.30 | 8.34 | 7.02 | 1.95 | 1.58 | 2.81 | 2.91 | Notes: 1. Figures in parentheses refer to per cent variations over the previous year.

2. Following amalgamation of Lakshmi Vilas Bank with DBS Bank India, w.e.f. November 27, 2020, private and foreign bank-group wise growth rates are based on adjusted bank-group totals.

3. Percentage variations could be slightly different as absolute numbers have been rounded off to ₹ crore.

4. NIM has been defined as NII as percentage of average assets.

Source: Annual accounts of respective banks. |

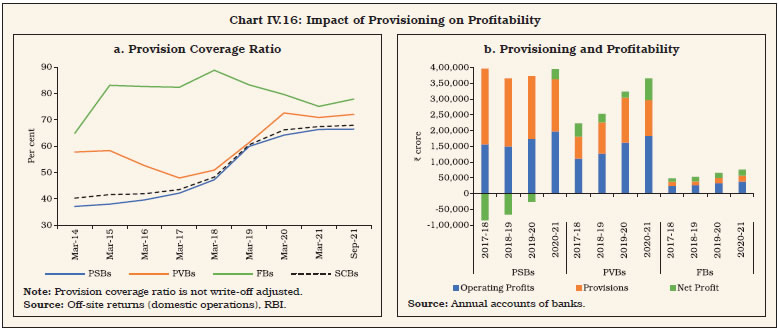

IV.23 Banks were required to maintain additional provisions of at least 10 per cent on moratorium amounts, which was allowed to be spread out across two quarters viz. Q4:2019-20 and Q1:2020-21. Most banks, especially PVBs, frontloaded the required provisions in the March 2020 quarter resulting in a higher provision coverage ratio for the year. Combined with lower slippage, this muted the provision requirements during 2020-21 which helped in boosting banks’ profitability (Chart IV.16). IV.24 Profitability of banks, measured in terms of spread between return on funds and cost of funds, improved with the decline in the latter exceeding that in the former. The improvement was especially evident in PSBs, while niche banks in the SFB and PB categories could not maintain their spreads (Table IV.4). | Table IV.4: Cost of Funds and Return on Funds | | Bank Group/ Variable | Year | Cost of Deposits | Cost of Borrowings | Cost of Funds | Return on Advances | Return on Investments | Return on Funds | Spread | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | (8-5) | | PSBs | 2019-20 | 5.0 | 4.6 | 4.9 | 8.2 | 6.9 | 7.8 | 2.8 | | | 2020-21 | 4.2 | 4.3 | 4.2 | 7.5 | 6.6 | 7.2 | 3.0 | | PVBs | 2019-20 | 5.3 | 6.2 | 5.4 | 10.1 | 6.6 | 9.2 | 3.8 | | | 2020-21 | 4.3 | 5.5 | 4.5 | 9.1 | 6.2 | 8.3 | 3.9 | | FBs | 2019-20 | 3.7 | 4.1 | 3.7 | 8.5 | 6.7 | 7.6 | 3.9 | | | 2020-21 | 2.4 | 3.4 | 2.5 | 7.1 | 6.1 | 6.5 | 4.0 | | SFBs | 2019-20 | 8.2 | 9.8 | 8.7 | 19.9 | 7.5 | 17.3 | 8.7 | | | 2020-21 | 6.8 | 8.8 | 7.3 | 17.1 | 6.8 | 14.9 | 7.6 | | PBs | 2019-20 | 1.6 | - | 1.6 | - | 3.5 | 3.5 | 1.9 | | | 2020-21 | 3.0 | 5.3 | 3.1 | 9.3 | 4.0 | 4.0 | 0.9 | | SCBs | 2019-20 | 5.0 | 5.4 | 5.0 | 8.9 | 6.8 | 8.3 | 3.2 | | | 2020-21 | 4.2 | 4.9 | 4.2 | 8.1 | 6.4 | 7.6 | 3.3 | Notes: 1. Cost of Deposits = Interest Paid on Deposits / Average of Current and Previous Years’ Deposits.

2. Cost of Borrowings = (Interest Expended - Interest on Deposits) /Average of Current and Previous Years’ Borrowings.

3. Cost of Funds = (Interest Expended) /Average of Current and Previous Years’ (Deposits + Borrowings).

4. Return on Advances = Interest Earned on Advances / Average of Current and Previous Years’ Advances.

5. Return on Investments = Interest Earned on Investments / Average of Current and Previous Years’ Investments.

6. Return on Funds = (Interest Earned on Advances + Interest Earned on Investments) /Average of Current and Previous Years’ (Advances + Investments).

7. Following the amalgamation of Lakshmi Vilas Bank with DBS Bank India, w.e.f. November 27, 2020, private and foreign bank-group wise data are adjusted accordingly.

Source: Calculated from balance sheets of respective banks. | 4. Soundness Indicators IV.25 During 2020-21, SCBs bolstered their capital positions, and also improved their asset quality, liquidity and leverage ratios, despite the pandemic. The number of banks under the Reserve Banks’s prompt corrective action (PCA) framework reduced from four at end-March 2020 to one at end-September 2021, reflecting bank-level as well as overall improvement in SCBs’ soundness indicators. 4.1 Capital Adequacy IV.26 The capital to risk-weighted assets ratio (CRAR) of SCBs has improved sequentially every quarter from end-March 2020 to reach 16.6 per cent at end-September 2021 (Table IV.5). This was essentially driven by a rise in core capital across bank groups, attributable to higher retained earnings, recapitalisation of PSBs by the government and raising of capital from the market. A slowdown in the accumulation of risk weighted assets (RWAs) of both PSBs and FBs helped to boost their capital ratios. IV.27 The number of banks breaching the regulatory minimum requirement of CRAR (including capital conservation buffer) (10.875 per cent) declined to one during 2020-21 from three in the previous year. The fatter right tails for end-March 2021 distributions as compared with those for 2019 imply that a bigger share of banks maintained higher CRAR and CET-1 ratio, with the peak between 2.5 to 5 per cent over andabove the minimum (Chart IV.17)3. Although the implementation of the last tranche of 0.625 per cent of capital conservation buffer (CCB) was deferred till October 1, 2021, banks proactively raised more capital to be in readiness for the imminent transition. IV.28 Resource mobilisation by banks through public and rights issues increased sharply in 2020-21, reflecting the follow-on public offer (FPO) of equity capital by a PVB to meet its capital requirements (Table IV.6). IV.29 In September 2020, the Parliament approved ₹20,000 crore capital infusion for PSBs which was fully disbursed by April 1, 2021. Since 2014, the government has infused ₹3.43 lakh crore in PSBs. In the Union Budget of 2021-22, the government has proposed to infuse another tranche of ₹20,000 crore into PSBs, which will help in augmenting their capital. IV.30 The resources raised by PSBs through private placement almost doubled during 2020-21. In 2021-22 so far, both PSBs and PVBs have resorted to this route for raising capital (Table IV.7). Table IV.5: Component-wise Capital Adequacy of SCBs

(At end-March) | | (Amount in ₹ crore) | | | PSBs | PVBs | FBs | SCBs | | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | | 1. Capital Funds | 6,99,872 | 7,93,971 | 6,54,772 | 7,72,389 | 1,88,665 | 2,04,433 | 15,56,686 | 17,90,330 | | i) Tier I Capital | 5,65,830 | 6,49,082 | 5,80,718 | 7,01,622 | 1,72,887 | 1,86,369 | 13,30,816 | 15,54,796 | | ii) Tier II Capital | 1,34,042 | 1,44,889 | 74,054 | 70,767 | 15,777 | 18,064 | 2,25,870 | 2,35,535 | | 2. Risk Weighted Assets | 54,46,253 | 56,56,060 | 39,56,956 | 41,92,303 | 10,65,889 | 10,49,878 | 1,05,35,311 | 1,09,86,622 | | 3. CRAR (1 as % of 2) | 12.9 | 14.0 | 16.5 | 18.4 | 17.7 | 19.5 | 14.8 | 16.3 | | Of which: Tier I | 10.4 | 11.5 | 14.7 | 16.7 | 16.2 | 17.8 | 12.6 | 14.2 | | Tier II | 2.5 | 2.6 | 1.9 | 1.7 | 1.5 | 1.7 | 2.1 | 2.1 | | Source: Off-site returns, RBI. |

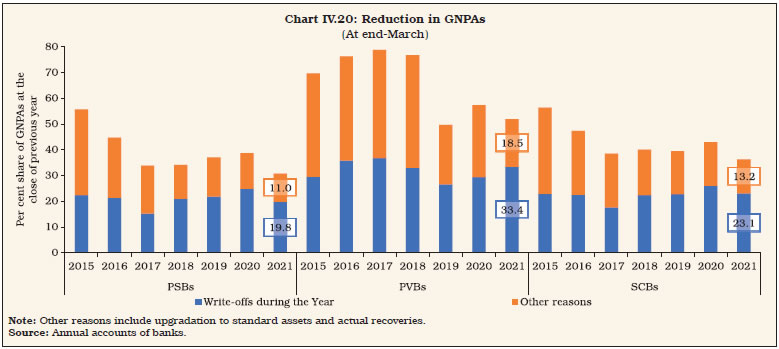

4.2 Leverage and Liquidity IV.31 The leverage ratio (LR), calculated as the ratio of tier-1 capital to total exposures, constrains the build-up of leverage by banks. Despite regulatory moderation in October 2019 requiring banks to maintain 4 and 3.5 per cent ratios for domestic systemically important banks and other banks, respectively as compared to 4.5 per cent earlier, the LR of SCBs rose for the second consecutive year during 2020-21. While the improvement was spread across all bank groups, it was led by a sharp improvement in the tier-1 capital of PVBs (Chart IV.18 a). | Table IV.6: Public and Rights Issues by the Banking Sector | | (Amount in ₹ crore) | | Year | PSBs | PVBs | Total | Grand Total | | Equity | Debt | Equity | Debt | Equity | Debt | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8= (6+7) | | 2019-20 | - | - | 410 | - | 410 | - | 410 | | 2020-21 | - | - | 15,000 | - | 15,000 | - | 15,000 | | 2021-22* | - | - | - | - | - | - | - | Note: 1. *: Up to November 2021.

2. -: Nil/Negligible.

Source: SEBI. | IV.32 The liquidity coverage ratio (LCR) - designed to help banks withstand liquidity pressures in the short-term - requires banks to maintain high quality liquid assets (HQLAs) to meet 30 days’ net outgo under stressed conditions. In March 2020, banks were allowed to avail funds under the marginal standing facility by dipping into the statutory liquidity ratio (SLR) by up to an additional one per cent of their net demand and time liabilities (NDTL) for three months. This dispensation was progressively extended up to December 31, 2021 to enable banks to meet their LCR requirements and provide comfort on their liquidity needs and will expire thereafter. Additionally, the LCR requirement for SCBs was brought down from 100 per cent to 80 per cent in April 2020 and was gradually restored in two phases by April 1, 2021. Notwithstanding the regulatory relaxation, banks continued to maintain LCR above 100 per cent: the ratio increased from 145 per cent at end-March 2020 to 158.9 per cent by end-March 2021 and 160.9 per cent by end-September 2021 (Chart IV.18 b). | Table IV.7: Resources Raised by Banks through Private Placements | | (Amount in ₹ crore) | | | 2019-20 | 2020-21 | 2021-22 (up to November) | | No. of Issues | Amount Raised | No. of Issues | Amount Raised | No. of Issues | Amount Raised | | PSBs | 20 | 29,573 | 36 | 58,697 | 16 | 32,567 | | PVBs | 8 | 23,121 | 4 | 33,878 | 5 | 17,222 | Note: Includes private placement of debt and qualified institutional placement. Data for 2021-22 are provisional.

Source: BSE, NSE and Merchant Bankers. |

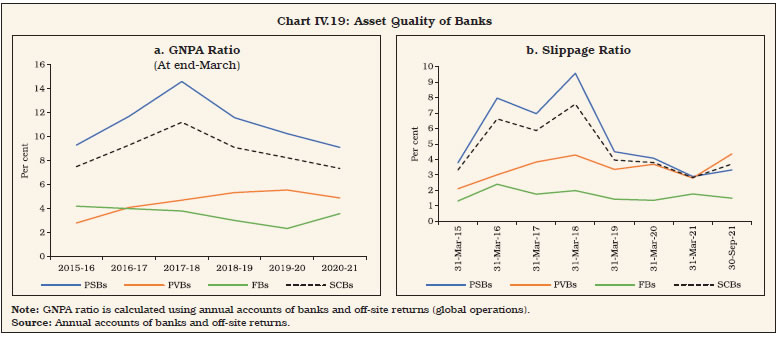

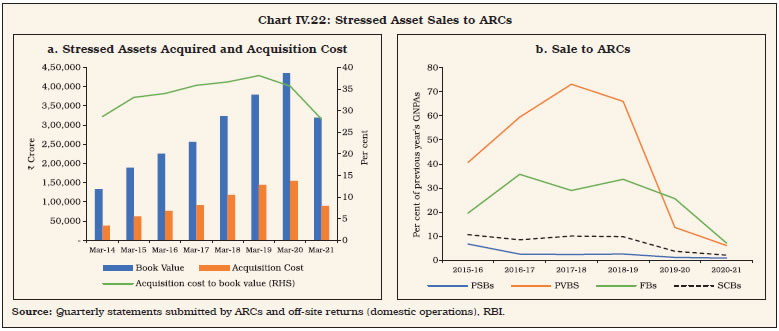

4.3 Non-Performing Assets IV.33 The moderation in GNPA ratios of banks that began in 2019-20, continued during the period under review to reach 7.3 per cent by end-March 2021. Provisional supervisory data suggest a further moderation in the ratio to 6.9 per cent by end-September 2021. During 2020-21, this improvement was driven by lower slippages, partly due to the asset classification standstill. With the decline in delinquent assets, their provision requirements also dropped and the net NPA ratio of PSBs and PVBs eased from the previous year. On the contrary, FBs reported increasing accretions to NPAs and deteriorating asset quality due to amalgamation of a troubled PVB with an FB (Chart IV.19).

| Table IV.8: Movement in Non-Performing Assets | | (Amount in ₹ crore) | | Item | PSBs | PVBs | FBs | SFBs | All SCBs | | Gross NPAs | | | | | | | Closing Balance for 2019-20 | 6,78,317 | 2,09,568 | 10,208 | 1,709 | 8,99,803 | | Opening Balance for 2020-21 | 5,46,590 | 2,05,335 | 10,208 | 1,709 | 7,63,842 | | Addition during the year 2020-21 | 2,78,711 | 1,03,625 | 12,840 | 5,470 | 4,00,646 | | Reduction during the year 2020-21 | 74,685 | 38,824 | 4,698 | 377 | 1,18,584 | | Written-off during the year 2020-21# | 1,34,000 | 69,995 | 3,307 | 832 | 2,08,134 | | Closing Balance for 2020-21 | 6,16,616 | 2,00,141 | 15,044 | 5,971 | 8,37,771 | | Gross NPAs as per cent of Gross Advances* | | | | | | | 2019-20 | 10.3 | 5.5 | 2.3 | 1.9 | 8.2 | | 2020-21 | 9.1 | 4.9 | 3.6 | 5.4 | 7.3 | | Net NPAs | | | | | | | Closing Balance for 2019-20 | 2,30,918 | 55,683 | 2,005 | 765 | 2,89,370 | | Closing Balance for 2020-21 | 1,96,451 | 55,809 | 2,987 | 2,981 | 2,58,228 | | Net NPAs as per cent of Net Advances | | | | | | | 2019-20 | 3.7 | 1.5 | 0.5 | 0.8 | 2.8 | | 2020-21 | 3.1 | 1.4 | 0.7 | 2.7 | 2.4 | Notes: 1. #: Includes prudential as well as actual write-offs.

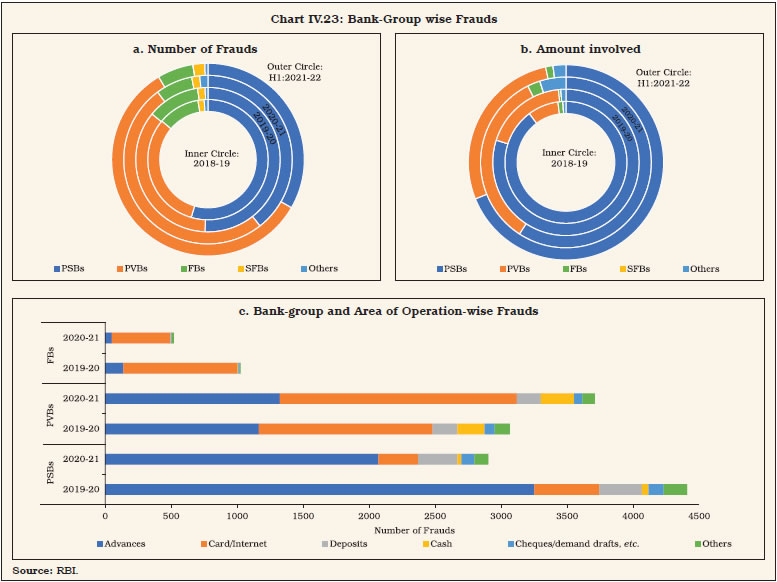

2. Closing balance for 2019-20 and opening balance for 2020-21 do not match due to amalgamation of banks. The amalgamated banks’ GNPAs are reported under ‘addition during the year’.

3. *: Calculated by taking gross NPAs from annual accounts of respective banks and gross advances from off-site returns (global operations).

Source: Annual accounts of banks and off-site returns (global operations), RBI. | IV.34 As observed since 2018, write-offs were the predominant recourse for lowering GNPAs in 2020-21 (Table IV.8 and Chart IV.20). In the case of FBs, the contribution of upgradation improved substantially, but it was not enough to offset fresh slippages. IV.35 Consistent with the improvement in asset quality, the proportion of standard assets to total advances of SCBs increased in 2020-21, largely because of the improved performance of PVBs (Table IV.9). Within standard assets, the share of restructured standard advances (RSA) increased from 0.4 per cent at end March 2020 to 0.8 per cent at end-March 2021, largely representing the onetime restructuring scheme for standard advances announced by the Reserve Bank in August 2020. The RSA further increased to 1.8 per cent at end September 2021 due to restructuring scheme 2.0 for retail loans and MSMEs which does not entail an asset classification downgrade.

| Table IV.9: Classification of Loan Assets by Bank Group | | (Amount in ₹ crore) | | Bank Group | End-March | Standard Assets | Sub-Standard Assets | Doubtful Assets | Loss Assets | | Amount | Per cent* | Amount | Per cent* | Amount | Per cent* | Amount | Per cent* | | PSBs | 2020 | 53,27,903 | 89.2 | 1,32,530 | 2.2 | 4,04,724 | 6.8 | 1,07,163 | 1.8 | | | 2021 | 55,87,450 | 90.6 | 1,03,744 | 1.7 | 3,51,014 | 5.7 | 1,22,217 | 2.0 | | PVBs | 2020 | 34,14,554 | 94.9 | 56,588 | 1.6 | 92,396 | 2.6 | 34,986 | 1.0 | | | 2021 | 37,57,240 | 95.3 | 65,363 | 1.7 | 90,228 | 2.3 | 31,350 | 0.8 | | FBs | 2020 | 4,25,857 | 97.7 | 3,273 | 0.8 | 5,775 | 1.3 | 1,161 | 0.3 | | | 2021 | 4,10,418 | 97.6 | 3,648 | 0.9 | 5,566 | 1.3 | 986 | 0.2 | | SFBs** | 2020 | 89,800 | 98.1 | 1,023 | 1.1 | 648 | 0.7 | 39 | 0.0 | | | 2021 | 1,05,619 | 94.6 | 4,965 | 4.4 | 841 | 0.8 | 165 | 0.1 | | All SCBs | 2020 | 92,58,114 | 91.7 | 1,93,413 | 1.9 | 5,03,543 | 5.0 | 1,43,349 | 1.4 | | | 2021 | 98,60,726 | 92.7 | 1,77,720 | 1.7 | 4,47,648 | 4.2 | 1,54,717 | 1.5 | Notes: 1. Constituent items may not add up to the total due to rounding off.

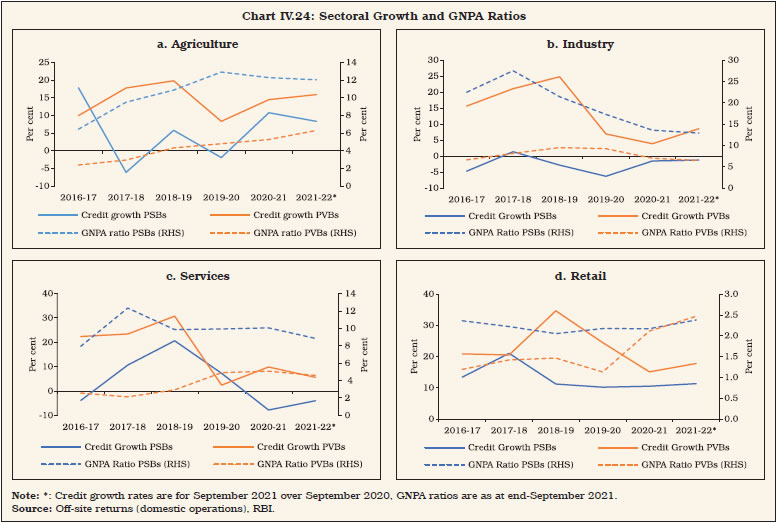

2. *: As per cent of gross advances.

3. **: Refers to scheduled SFBs.

Source: Off-site returns (domestic operations), RBI. | IV.36 The share of large borrowal accounts (exposure of ₹5 crore or more) in total advances declined to 51 per cent at end-March 2021 from 54.2 per cent a year ago. Their contribution to total NPAs also declined in tandem from 75.4 per cent to 66.2 per cent during the same period. The special mention accounts-2 (SMA-2) ratio, which signals impending stress, has risen across bank groups since the outbreak of the pandemic. The RSA ratio has also increased during the same period, partly reflecting the impact of resolution framework (RF) 1.0 and 2.0 (Chart IV.21). 4.4 Recoveries IV.37 During 2020-21, all the recovery channels, most notably Lok Adalats, witnessed a sizeable decline in the cases referred for resolution (Table IV.10). Even though initiation of fresh insolvency proceedings under the Insolvency and Bankruptcy Code (IBC) of India was suspended for a year till March 2021 and COVID-19 related debt was excluded from the definition of default, it constituted one of the major modes of recoveries in terms of amount recovered. Allowing pre-pack resolution window for MSMEs is expected to assuage the mounting pressure of pending cases before NCLTs, reducehaircuts and improve declining recovery rates4. IV.38 Another important mode of asset resolution for banks, especially PVBs, has been sale of NPAs to asset reconstruction companies (ARCs) by taking haircuts. In recent years, however, the preference of banks has shifted to alternative avenues, with asset sales declining as a proportion to outstanding GNPAs across bank groups. This was partly due to the worsening acquisition cost of ARCs as a proportion of book value of assets, reflecting higher haircuts and lower realisable values in respect of their acquired assets (Chart IV.22). IV.39 The recovery of security receipts (SRs) issued by ARCs is a critical indicator of their performance. Since 2018, the Reserve Bank has been disincentivising banks from holding SRs in excess of 10 per cent of the transaction value of sale of stressed assets through increasedprovisions.5 Consequently, the share of SRs subscribed to by banks has decreased over the years, and their share hovered around 58per cent in 2019-20 and 2020-216. The share of ARCs in SR holdings has declined over the years, with the investor base having gradually diversified with an increasing share of foreign institutional investors and other qualified buyers (Table IV.11). | Table IV.10: NPAs of SCBs Recovered through Various Channels | | (Amount in ₹ crore) | | Recovery Channel | 2019-20 | 2020-21 (P) | | No. of cases Referred | Amount Involved | Amount recovered* | Col. (4) as per cent of Col. (3) | No. of cases Referred | Amount Involved | Amount recovered* | Col. (8) as per cent of Col. (7) | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | | Lok Adalats | 59,86,790 | 67,801 | 4,211 | 6.2 | 19,49,249 | 28,084 | 1,119 | 4.0 | | DRTs | 33,139 | 2,05,032 | 9,986 | 4.9 | 28,182 | 2,25,361 | 8,113 | 3.6 | | SARFAESI Act | 1,05,523 | 1,96,582 | 34,283 | 17.4 | 57,331 | 67,510 | 27,686 | 41.0 | | IBC@ | 1,986 | 2,24,935 | 1,04,117 | 46.3 | 537 | 1,35,139 | 27,311 | 20.2 | | Total | 61,27,438 | 6,94,350 | 1,52,597 | 22.0 | 20,35,299 | 4,56,094 | 64,228 | 14.1 | Notes: 1. P: Provisional.

2. *: Refers to the amount recovered during the given year, which could be with reference to the cases referred during the given year as well as during the earlier years.

3. DRTs: Debt Recovery Tribunals.

4. @: Cases admitted by National Company Law Tribunals (NCLTs) under IBC.

5. The resolution plan of Essar Steel India Ltd. was approved in 2018-19. However, as apportionment among creditors was settled in 2019-20, the recovery is reflected in the latter year data.

Source: Off-site returns, RBI and Insolvency and Bankruptcy Board of India (IBBI). |

4.5 Frauds in the Banking Sector IV.40 Apart from eroding customer confidence, frauds present multiple challenges for the financial system in the form of reputational risk, operational risk and business risk. During 2020-21, the reported number of cases of frauds declined (Table IV.12). In terms of amount involved, a bulk of these cases occurred earlier but were reported during the year 2020-21 (Table IV.13). IV.41 In terms of area of operations, an overwhelming majority of cases reported during 2020-21 in terms of number and amount involved related to advances, while frauds concerning card or internet transactions made up 34.6 per cent of the number of cases. IV.42 In 2020-21, there was a marked increase in frauds related to PVBs, both in terms of number as well as the amount involved. During H1:2021-22, PVBs accounted for more than half of the number of reported fraud cases (Chart IV.23a). In value terms, however, the share of PSBs was higher, indicating predominance of high value frauds (Chart IV.23b). While the major share of loans-related cases pertained to PSBs, PVBs accounted for a majority of card/ internet and cash-related cases (Chart IV.23c). | Table IV.11: Details of Financial Assets Securitised by ARCs | | (Amount in ₹ crore) | | Item | Mar-19 | Mar-20 | Mar-21 | | Reporting ARCs | 18 | 23 | 21 | | 1. Book Value of the Assets acquired from banks/FIs | 1,86,770 | 2,95,097 | 3,19,838 | | Reporting ARCs | 12 | 11 | 11 | | 2. Amount of Security Receipts (SRs) issued | 14,691 | 59,347 | 69,995 | | 3. Security Receipts Subscribed to by: | | | | | a Selling Banks/ Financial Institutions | 10,659 | 34,147 | 41,076 | | b Asset Reconstruction Companies (ARCs) | 3,663 | 12,421 | 13,942 | | c FIIs | 151 | 8,750 | 9,861 | | d Others (Qualified Institutional Buyers) | 219 | 4,028 | 5,116 | | 4. Amount of SRs completely redeemed | 558 | 9,062 | 13,283 | | 5. SRs Outstanding | 13,087 | 39,618 | 42,266 | | Source: Quarterly statements submitted by ARCs. |

| Table IV.12: Frauds in Various Banking Operations Based on the Date of Reporting | | (Cases in number and amount in ₹ crore) | | Area of Operation | 2018-19 | 2019-20 | 2020-21 | 2020-21 (April-September) | 2021-22 (April-September) | | Number of frauds | Amount Involved | Number of frauds | Amount Involved | Number of frauds | Amount Involved | Number of Frauds | Amount Involved | Number of Frauds | Amount involved | | Advances | 3,603 | 64,539 | 4,608 | 1,81,942 | 3,501 | 1,37,023 | 1,669 | 63,529 | 1,802 | 35,060 | | Off-balance Sheet | 33 | 5,538 | 34 | 2,445 | 23 | 535 | 14 | 439 | 10 | 612 | | Forex Transactions | 13 | 695 | 8 | 54 | 4 | 129 | 1 | 0 | 1 | 0 | | Card/Internet | 1,866 | 71 | 2,677 | 129 | 2,545 | 119 | 1,247 | 49 | 1,532 | 60 | | Deposits | 593 | 148 | 530 | 616 | 504 | 434 | 245 | 149 | 208 | 362 | | Inter-Branch Accounts | 3 | 0 | 2 | 0 | 2 | 0 | 2 | 0 | 0 | 0 | | Cash | 274 | 56 | 371 | 63 | 329 | 39 | 132 | 22 | 245 | 51 | | Cheques/DDs, etc. | 189 | 34 | 201 | 39 | 163 | 85 | 77 | 48 | 107 | 149 | | Clearing Accounts | 24 | 209 | 22 | 7 | 14 | 4 | 4 | 1 | 9 | 1 | | Others | 200 | 244 | 250 | 173 | 278 | 54 | 108 | 25 | 157 | 47 | | Total | 6,798 | 71,534 | 8,703 | 1,85,468 | 7,363 | 1,38,422 | 3,499 | 64,261 | 4,071 | 36,342 | Notes: 1. Refers to frauds of ₹1 lakh and above.

2. The figures reported by banks and financial institutions are subject to change based on revisions filed by them.

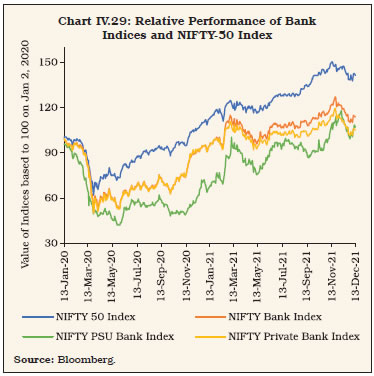

3. Frauds reported in a year could have occurred several years prior to year of reporting.

4. Amounts involved are as reported and do not reflect the amount of loss incurred. Depending on recoveries, the loss incurred gets reduced. Further, the entire amount involved in loan accounts is not necessarily diverted.

Source: RBI. |

| Table IV.13: Frauds in Various Banking Operations Based on the Date of Occurrence | | (Cases in number and amount in ₹ crore) | | Area of operation | Prior to 2018-19 | 2018-19 | 2019-20 | 2020-21 | 2021-22 (April - September) | | Number of frauds | Amount Involved | Number of frauds | Amount Involved | Number of frauds | Amount Involved | Number of frauds | Amount Involved | Number of Frauds | Amount involved | | Advances | 8,752 | 3,33,362 | 2,129 | 40,516 | 1,525 | 31,074 | 903 | 13,373 | 205 | 237 | | Off-balance Sheet | 71 | 5,817 | 19 | 2,927 | 5 | 371 | 5 | 12 | 0 | 0 | | Forex Transactions | 11 | 597 | 5 | 145 | 7 | 135 | 3 | 1 | 0 | 0 | | Card/Internet | 485 | 31 | 2,090 | 83 | 2,645 | 130 | 2,296 | 104 | 1,104 | 32 | | Deposits | 475 | 606 | 550 | 163 | 438 | 338 | 306 | 421 | 66 | 32 | | Inter-Branch Accounts | 3 | 0 | 3 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | | Cash | 95 | 40 | 275 | 64 | 381 | 37 | 336 | 45 | 132 | 21 | | Cheques/DDs, etc. | 109 | 34 | 165 | 28 | 201 | 69 | 144 | 163 | 41 | 12 | | Clearing Accounts, etc. | 17 | 9 | 26 | 206 | 13 | 2 | 9 | 3 | 4 | 0 | | Others | 289 | 277 | 201 | 58 | 144 | 132 | 206 | 35 | 45 | 18 | | Total | 10,307 | 3,40,773 | 5,463 | 44,191 | 5,359 | 32,290 | 4209 | 14,158 | 1,597 | 353 | Notes: 1. Refers to frauds of ₹1 lakh and above.

2. The figures reported by banks and financial institutions are subject to change based on revisions filed by them.

3. Data based on ‘date of occurrence’ may change for a period of time as frauds reported late but having occurred earlier would get added.

4. Data in the table pertain to cases reported from 2018-19 till September 30, 2021.

Source: RBI. |

4.6 Enforcement Actions IV.43 In order to separate enforcement action from the supervisory process and in accordance with international best practices, the Enforcement Department was created in the Reserve Bank in 2017. The department is entrusted with ensuring uniformity and consistency in enforcement of regulations and engendering compliance in the regulated entities (REs). During 2020-21, the number of instances of imposition of penalty reduced, with enforcement action being undertaken against 11 SCBs. Monetary penalties were imposed for non-compliance with provisions or contravention of certain directions issued by the Reserve Bank, including frauds classification and reporting, exposure norms and IRAC norms, interest rate on deposits and lending to MSMEs (Table IV.14). | Table IV.14: Enforcement Actions | | Regulated Entity | April 2019 to March 2020 | April 2020 to March 2021 | | Instances of imposition of penalty | Total Penalty

(₹ crore) | Instances of imposition of penalty | Total Penalty

(₹ crore) | | Public Sector Banks | 29 | 35.1 | 4 | 9.5 | | Private Sector Bank | 11 | 11.5 | 3 | 5.9 | | Cooperative Banks | 9 | 7.4 | 43 | 3.9 | | Foreign Banks | 1 | 1.0 | 3 | 8.0 | | Payments Banks | - | - | 1 | 1.0 | | Small Finance Banks | - | - | - | - | | NBFCs | 2 | 0.1 | 7 | 3.1 | | Total | 52 | 55 | 61 | 31 | | Source: RBI. | 5. Sectoral Bank Credit: Distribution and NPAs IV.44 Headline credit growth remained anaemic during 2020-21, although sectorally some bright spots appeared: agriculture credit revived from a sharp deceleration of the previous year; PVBs increased their lending to the services sector; and PSBs cushioned the deceleration in total retail credit growth, albeit partly. On the other hand, credit growth to services by PSBs and to retail by PVBs slowed down amidst rising NPA ratios (Chart IV.24). IV.45 A drill down into the data reveals that although credit to large industries contracted, their medium-sized counterparts received sharply higher credit flows, incentivised by the Emergency Credit Line Guarantee Scheme(ECLGS)7. The higher NPAs of large industrial borrowers at the end of March 2021 as compared to better asset quality of medium enterprises may also be a driving factor. Within services, credit growth to trade surpassed its pre-pandemic growth rate in 2020-21. Remarkably, its share in services sector credit also grew sharply in 2020-21. After the IL&FS event, NBFCs—especially those with lower ratings— found raising resources from the market difficult and turned to banks. SCBs’ credit to NBFCs grew in double digits during 2015-16 to 2019-20 but decelerated in 2020-21 on a high base (Table IV.15).

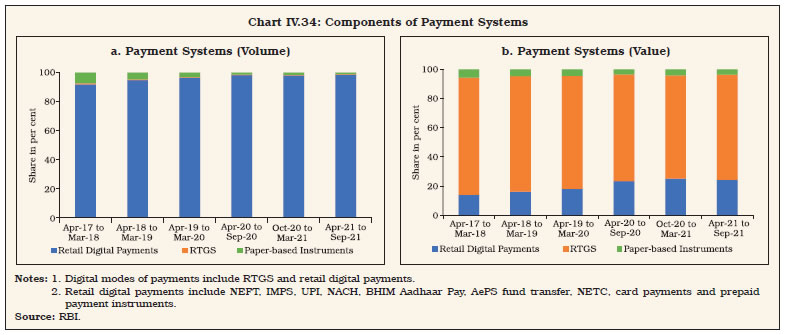

| Table IV.15: Sectoral Deployment of Gross Bank Credit | | (Amount in ₹ crore) | | Sr. No. | Item | Outstanding as on | Per cent variation (y-o-y) | | Mar-19 | Mar-20 | Mar-21 | Sep-21 | 2018-19 | 2019-20 | 2020-21 | 2021-22 (up to September)* | | 1 | Agriculture & Allied Activities | 12,17,594 | 12,39,575 | 13,84,815 | 14,30,480 | 10.0 | 1.8 | 11.7 | 10.7 | | 2 | Industry, of which | 32,93,638 | 32,52,801 | 32,53,636 | 32,34,613 | 5.2 | -1.2 | 0.03 | 3.3 | | | 2.1 Micro & Small Industries | 4,39,811 | 4,37,658 | 4,72,529 | 5,41,554 | 5.2 | -0.5 | 8.0 | 16.8 | | | 2.2 Medium | 1,23,843 | 1,12,367 | 1,87,599 | 2,06,151 | -1.7 | -9.3 | 67.0 | 47.0 | | | 2.3 Large | 26,11,567 | 26,11,377 | 24,76,702 | 23,59,112 | 6.1 | -0.01 | -5.2 | -3.4 | | 3 | Services, of which | 26,02,287 | 27,54,823 | 27,45,324 | 27,24,810 | 25.1 | 5.9 | -0.3 | 1.3 | | | 3.1 Trade | 5,83,930 | 6,28,142 | 7,14,210 | 6,75,820 | 12.4 | 7.6 | 13.7 | 3.7 | | | 3.2 Commercial Real Estate | 2,43,122 | 2,66,357 | 2,52,696 | 2,76,980 | 18.9 | 9.6 | -5.1 | 8.7 | | | 3.3 Tourism, Hotels & Restaurants | 56,194 | 60,039 | 62,722 | 61,027 | 7.9 | 6.8 | 4.5 | -2.1 | | | 3.4 Computer Software | 22,236 | 24,404 | 23,742 | 21,570 | -0.3 | 9.8 | -2.7 | -4.4 | | | 3.5 Non-Banking Financial Companies | 6,27,089 | 7,36,447 | 7,98,241 | 8,24,189 | 38.4 | 17.4 | 8.4 | 14.8 | | 4 | Retail Loans, of which | 23,04,313 | 26,59,249 | 29,86,461 | 31,10,368 | 18.6 | 15.4 | 12.3 | 14.0 | | | 4.1 Housing Loans | 12,04,362 | 13,96,444 | 15,61,913 | 15,99,395 | 19.5 | 15.9 | 11.8 | 11.2 | | | 4.2 Consumer Durables | 9,195 | 11,154 | 21,569 | 28,409 | -51.7 | 21.3 | 93.4 | 69.2 | | | 4.3 Credit Card Receivables | 1,11,361 | 1,32,076 | 1,38,560 | 1,43,937 | 34.5 | 18.6 | 4.9 | 2.2 | | | 4.4 Vehicle/Auto Loans | 2,69,677 | 2,89,366 | 3,29,522 | 3,61,849 | 12.9 | 7.3 | 13.9 | 21.2 | | | 4.5 Education Loans | 76,233 | 79,056 | 78,823 | 82,433 | 1.8 | 3.7 | -0.3 | 2.9 | | | 4.6 Advances against Fixed Deposits (incl. FCNR (B), etc.) | 77,135 | 80,753 | 74,013 | 72,718 | -0.1 | 4.7 | -8.3 | 1.7 | | | 4.7 Advances to Individuals against Shares, Bonds, etc. | 9,339 | 5,619 | 5,619 | 6,092 | 46.3 | -39.8 | 0 | -12.7 | | | 4.8 Other Retail Loans | 5,47,010 | 6,64,781 | 7,76,441 | 8,15,535 | 25.6 | 21.5 | 16.8 | 20.8 | | 5 | Gross Bank Credit | 95,26,932 | 1,00,98,420 | 1,06,40,811 | 1,07,52,479 | 13.4 | 6.0 | 5.4 | 6.8 | Note: 1. Figures in the table may not tally with the figures released by RBI in ‘Sectoral Deployment of Bank Credit’ every month due to difference in coverage of banks.

2. Percentage variations are March over March.

3. The data pertain to SCBs.

4. *September 2021 over September 2020.

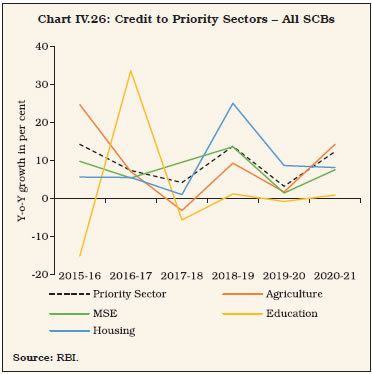

Source: Off-site returns (domestic operations), RBI. | IV.46 During 2020-21, retail loan portfolios of banks outgrew their services sector lending, aided by double digit acceleration in housing loans- the biggest component of retail loans. Vehicle loans gained traction, reflecting consumer interest after companies announced substantial discounts on automobiles. IV.47 The RSA ratio of SCBs had been decelerating for five consecutive years since 2015 on better asset quality recognition by banks after the asset quality review (AQR). With the restructuring scheme announced in August 2020 by the Reserve Bank in response to the pandemic, the RSA ratio, especially of services and retail loans increased sharply in 2020-21, led by contact-intensive services (Chart IV.25). 5.1 Priority Sector Credit IV.48 Priority sector lending (PSL) accelerated in 2020-21, primarily driven by revival in credit to agriculture—especially Kisan Credit Card (KCC) loans—and micro and small enterprises (MSEs) by both PSBs and PVBs (Chart IV.26 and Appendix Table IV.3). IV.49 PSL, which is typically pro-cyclical, is also influenced by bank-specific characteristics such as asset quality of the PSL vis-à-vis non-priority sector loans, size of the lending bank and their branch network (Box IV.2). IV.50 During 2020-21, all bank groups managed to achieve the overall PSL targets. Shortfalls were observed in certain sub-targets by PSBs (micro enterprises) and PVBs (agriculture; small and marginal farmers (SMFs) and non-corporate individual farmers) (Table IV.16). A phased increase in PSL targets for SMFs and weaker sections as per the revised PSL guidelines issued in September 2020 is expected to deepen credit penetration to thesesectors12.

Box IV.2: Determinants of Priority Sector Lending Priority sector lending – aimed at meeting requirements of sectors which are credit-starved but are socially significant began in India in 1969. SCBs8 are required to lend 40 per cent of their previous year’s adjusted net bank credit (ANBC) or credit equivalent of off balance-sheet exposures (CEOBE), whichever is higher, to the priority sector. Despite uniform regulatory requirements, banks have deviated from the regulatory target in some periods across banks and bank groups. Multiple avenues are available to banks to meet regulatory obligations in case of shortfall in direct lending, including Inter- Bank Participation Certificates (IBPCs), securitisation of priority sector loans, depositing shortfalls in funds such as the Rural Infrastructure Development Fund (RIDF) and other funds with NABARD, NHB, SIDBI and MUDRA Ltd. In 2016, trading in priority sector lending certificates (PSLCs) was introduced, which was a game changer as it allowed buying for shortfall and selling for overachievement of PSL targets without corresponding transfer of loan, cash flows or risk. Empirically, priority sector lending is found to depend on various bank-specific characteristics like the nature of ownership, size as well as performance (Kumar, Batra, & Deisting, 2016). A fixed effect panel regression for the period March 2005 till December 2020 with organic PSL by banks as the dependent variable using quarterly bank-wise data on 59 banks suggests that asset quality plays an important role in priority sector lending decisions: banks which face priority sector asset quality stress tended to lend less to it. GDP, which is a control for macro-economic factors, and bank size9 – a bank-specific control variable – have a positive relationship with PSL. A dummy for the March quarter was found to be positive and significant, as banks tended to backload their PSL in the last quarter to improve their annual average and achieve the regulatory target10. Branches to assets ratio, a proxy for banks’ reach, is also found to be significant11. | Table 1: Determinants of Priority Sector Lending | | Variables | Dependent Variables | | Priority Sector Advances | Priority Sector Agricultural Advances | Priority Sector MSE Advances | | Dependent Variable (-1) | 0.477*** | 0.564*** | 0.746*** | | | (0.111) | (0.0947) | (0.0313) | | Priority GNPA Ratio | -0.0161*** | | | | | (0.00314) | | | | Non-Priority GNPA Ratio | 0.00495** | | 0.00492*** | | | (0.00192) | | (0.00171) | | Agriculture GNPA Ratio | | -0.00606*** | | | | | (0.000868) | | | MSE GNPA Ratio | | | -0.0154*** | | | | | (0.00326) | | March Dummy | 0.0351*** | 0.0616*** | 0.0461*** | | | (0.0103) | (0.0161) | (0.0156) | | GDP | 0.0568** | | 0.0979** | | | (0.0231) | | (0.0454) | | Agricultural GDP | | 0.0896*** | | | | | (0.0329) | | | CRAR | | 0.00230 | 0.00329 | | | | (0.00332) | (0.00231) | | PSLC Dummy | 0.0597*** | 0.0443** | -0.0204 | | | (0.0217) | (0.0167) | (0.0225) | | Bank Size | 0.480*** | 0.397*** | 0.290*** | | | (0.106) | (0.0962) | (0.0515) | | Branches per Asset | 0.00240*** | | | | | (0.000542) | | | | Rural Branches per Asset | | 0.00713*** | | | | | (0.00173) | | | Urban Branches per Asset | | | 0.00344*** | | | | | (0.000623) | | RoE | 0.00 | | | | | (0.000) | | | | Constant | -1.307*** | -1.990*** | -2.581*** | | | (0.338) | (0.495) | (0.371) | | Observations | 2,765 | 2,769 | 2,749 | | R-squared | 0.970 | 0.938 | 0.948 | | Number of Banks | 59 | 59 | 59 | Notes: 1. Robust standard errors in parentheses

2. *** p<0.01, ** p<0.05, * p<0.1 | For the sub-targets on lending to agriculture (18 per cent) and micro and small enterprises (MSEs) (7.5 per cent), similar models are estimated with rural and urban branches to assets ratio, respectively. The coefficients are significant and positive. Banks with significant brick-and-mortar presence in rural areas lend higher to priority agriculture sector while those in urban areas specialise in MSE lending. A positive and significant PSLC dummy for overall PSL as well as sub-targets suggests that the introduction of PSLCs has given banks an opportunity to profitably trade in PSLCs while simultaneously fulfilling regulatory targets. References: Kumar, M., Batra, N., & Deisting, F. (2016). Determinants Of Priority Sector Lending: Evidence From Bank Lending Patterns In India. The International Journal of Business and Finance Research. | IV.51 The total trading volume of PSLCs grew by 26 per cent to ₹5,89,163 crores during 2020-21. Among the four PSLC categories, significant growth was recorded in case of PSLC-General and PSLC-Micro Enterprises (Chart IV.27). IV.52 The weighted average premiums (WAPs) for PSLCs increased year-on-year by 11 to 44 basis points across categories in 2020-21, with PSLC-SMF and PSLC-A categories commanding significantly higher premiums than PSLC-G and PSLC-ME. During H1:2021-22, the WAP on PSLCs-ME increased sharply due to change in the definition of MSMEs. The increase in WAP across other categories may be attributed to COVID-related stress (Table IV.17). Table IV.16: Priority Sector Lending by Banks

(As on March 31, 2021) | | (Amount in ₹ crore) | | Item | Target/ sub-target (per cent of ANBC/ CEOBE) | Public Sector Banks | Private Sector Banks | Foreign Banks | Small Finance Banks | | Amount Outstanding | Per cent of ANBC/ CEOBE | Amount Outstanding | Per cent of ANBC/ CEOBE | Amount Outstanding | Per cent of ANBC/ CEOBE | Amount Outstanding | Per cent of ANBC/ CEOBE | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | | Total Priority Sector Advances | 40/75* | 24,16,750 | 41.06 | 14,33,674 | 40.62 | 1,99,969 | 41.02 | 59,055 | 86.00 | | of which | | | | | | | | | | | Total Agriculture | 18.0 | 10,68,112 | 18.15 | 5,29,637 | 15.01 | 45,457 | 18.97 | 19,239 | 28.02 | | Small and marginal farmers | 8.0 | 5,53,455 | 9.40 | 2,40,754 | 6.82 | 24,233 | 10.11 | 17,798 | 25.92 | | Non-corporate Individual Farmers# | 12.14 | 7,69,173 | 13.07 | 3,64,026 | 10.31 | 29,187 | 12.18 | 20,422 | 29.74 | | Micro Enterprises | 7.50 | 4,18,763 | 7.11 | 2,93,072 | 8.30 | 18,050 | 7.53 | 16,580 | 24.14 | | Weaker Sections | 10.0 | 7,27,794 | 12.37 | 3,58,002 | 10.14 | 28,037 | 11.70 | 36,377 | 52.97 | Notes: 1. Amount outstanding and achievement percentage are based on the average achievement of banks for four quarters of the financial year.

2. *: Total priority sector lending target for Small Finance Banks is 75 per cent.

3. #: Target for non-corporate farmers is based on the system-wide average of the last three years’ achievement. For FY 2020-21, the applicable system wide average figure is 12.14 percent.

4. For foreign banks having less than 20 branches, only the total PSL target of 40 per cent is applicable.

Source: RBI. | IV.53 While the share of priority sector accounts in total bank lending increased only marginally from 35 per cent in 2019-20 to 36 per cent in 2020-21, their share in total GNPAs increased markedly from 32.8 per cent to 40.5 per cent during the same period, led by delinquencies in agricultural and micro and small enterprises PSL (Table IV.18). 5.2 Credit to Sensitive Sectors IV.54 Banks’ exposure to sensitive sectors decelerated during 2020-21. Nevertheless, it grew at a higher pace than overall credit growth, led by the real estate sector, especially by PVBs and FBs. Banks’ capital market exposure contracted for the second consecutive year (Chart IV.28 and Appendix Table IV.4). | Table IV.17: Weighted Average Premium on Various Categories of PSLCs | | (Per cent) | | PSLC Category | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2020-21 (Apr-Sep) | 2021-22 (Apr-Sep) | | PSLC-A | 1.29 | 0.79 | 1.17 | 1.55 | 1.61 | 2.00 | | PSLC-ME | 0.61 | 0.57 | 0.44 | 0.88 | 0.54 | 2.03 | | PSLC-SMF | 1.54 | 1.15 | 1.58 | 1.74 | 1.87 | 2.38 | | PSLC-G | 0.59 | 0.31 | 0.35 | 0.46 | 0.49 | 0.85 | | Source: RBI. |

Table IV.18: Sector-wise GNPAs of Banks

(At end-March) | | (Amount in ₹ crore) | | Bank Group | Priority Sector | Of which | Non-priority Sector | Total NPAs | | Agriculture | Micro and Small Enterprises | Others | | Amt. | Per cent# | Amt. | Per cent# | Amt. | Per cent# | Amt. | Per cent# | Amt. | Per cent# | Amt. | Per cent# | | PSBs | | | | | | | | | | | | | | 2020 | 2,36,212 | 36.66 | 1,11,571 | 17.31 | 90,769 | 14.09 | 33,872 | 5.26 | 4,08,205 | 63.34 | 6,44,417 | 100.00 | | 2021 | 2,58,228 | 44.76 | 1,15,281 | 19.98 | 1,01,786 | 17.64 | 41,161 | 7.13 | 3,18,747 | 55.24 | 5,76,974 | 100.00 | | PVBs | | | | | | | | | | | | | | 2020 | 36,219 | 19.69 | 14,462 | 7.86 | 16,111 | 8.76 | 5,646 | 3.07 | 1,47,751 | 80.31 | 1,83,970 | 100.00 | | 2021 | 50,557 | 27.04 | 18,900 | 10.11 | 23,473 | 12.56 | 8,184 | 4.38 | 1,36,384 | 72.96 | 1,86,941 | 100.00 | | FBs | | | | | | | | | | | | | | 2020 | 1,692 | 16.57 | 376.07 | 3.68 | 1070.24 | 10.48 | 245.66 | 2.41 | 8,516 | 83.43 | 10,208 | 100.00 | | 2021 | 1,802 | 17.67 | 328.97 | 3.23 | 1193.62 | 11.70 | 279.48 | 2.74 | 8,397 | 82.33 | 10,199 | 100.00 | | SFBs | | | | | | | | | | | | | | 2020 | 1,376 | 80.51 | 255.77 | 14.96 | 753.88 | 44.10 | 366.59 | 21.45 | 333 | 19.49 | 1,709 | 100.00 | | 2021 | 4,974 | 83.31 | 1509.6 | 25.28 | 2049.4 | 34.32 | 1415.23 | 23.70 | 996 | 16.69 | 5,971 | 100.00 | | All SCBs | | | | | | | | | | | | | | 2020 | 2,75,499 | 32.79 | 1,26,664 | 15.07 | 1,08,704 | 12.94 | 40,131 | 4.78 | 5,64,806 | 67.21 | 8,40,305 | 100.00 | | 2021 | 3,15,561 | 40.45 | 1,36,019 | 17.44 | 1,28,502 | 16.47 | 51,039 | 6.54 | 4,64,524 | 59.55 | 7,80,085 | 100.00 | Notes: 1. Amt.: – Amount; Per cent: Per cent of total NPAs.

2. Constituent items may not add up to the total due to rounding off.

3. # Share in total NPAs.

Source: Off-site returns (domestic operations), RBI. |

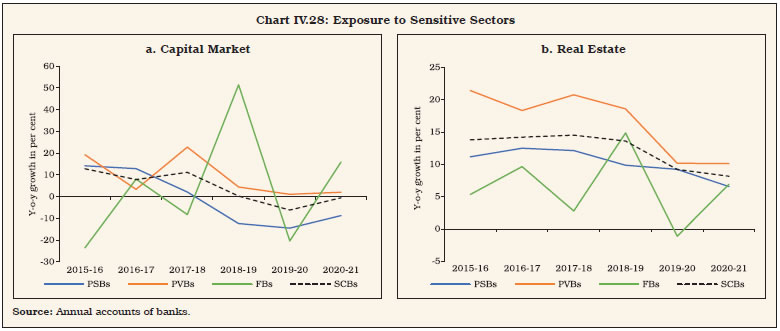

6. Performance of Banking Stocks IV.55 After the outbreak of the COVID-19 pandemic, equity markets in India fell sharply, tracking global cues. Banking sector stocks were hit hard, reflecting investors’ concerns about their financial health, although the impact was not homogenous across banks and bank groups. Subsequently, in response to the policy measures initiated by the Reserve Bank and the Government of India, stock prices revived (Chart IV.29) IV.56 Empirical evidence suggests that stock prices of banks with weak balance sheets were hammered down more by investors in the pandemic shock (Box IV.3)

Box IV.3: Impact of COVID-19 Lockdown on Banking Stock Performance Globally, the pandemic and lockdowns led to persistent underperformance of banking sector stocks vis-à-vis the headline index. Market anxiety over potential liquidity risks led to a sell-off in these stocks. Subsequently, however, as policy support measures were introduced, reversals also became evident (Acharya et al., 2021; Kunt et al., 2021). In India, too, the imposition of a nation-wide lockdown effective from March 24, 2020 onwards triggered investors’ anxiety about banking stocks. In order to unravel this phenomenon empirically, a two-step approach is adopted13. In the first step, an event study model (MacKinlay, 1997; Mathur et al., 2021) was employed to compute equation (1), which is estimated over a period of 91 to 11 days prior to the event day, i.e. imposition of lockdown. As expected, CARs for SCBs declined significantly following the announcement of the nation-wide lockdown (Chart 1). Moreover, the impact was felt across the board, irrespective of bank size and bank group (Chart 2).

In the second step, a cross-sectional regression model (equation 3) is used to investigate the role of bank-level characteristics in explaining the CARs15:  where the size of the bank (proxied by log of total assets) and a binary variable for bank group (0 for PVBs and 1 for PSBs) are used as control variables. Balance sheet and financial variables such as profitability (RoE), asset quality (GNPA ratio and slippage ratio) and capital adequacy (CET-1 ratio), are represented by Xb. The results from the regression analysis suggest that controlling for size and ownership, banks which had stronger balance sheets and financial positions – such as higher RoE and CET-1 ratio – in the pre-pandemic period suffered lower losses. On the other hand, banks which entered the pandemic with higher GNPA and slippage ratios were penalised by markets with sharper price corrections (Table 1). These findings highlight the importance of robust balance sheets of banks so as to withstand large macroeconomic shocks. | Table 1: Regression Results | | Dependent Variable: CAR (-1, +1) | | Categories | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | | Size | 0.050 | 0.070 | 0.127 | -0.101 | 0.117 | | | (1.070) | (0.976) | (1.005) | (0.997) | (0.782) | | Bank-Group Dummy | 0.731 | 1.259 | 2.108 | 3.943 | 1.806 | | | (2.625) | (2.404) | (2.667) | (2.814) | (1.931) | | ROE | - | 0.100* | - | - | - | | | | (0.040) | | | | | CET-1 ratio | - | - | 0.724* | - | - | | | | | (0.282) | | | | GNPA ratio | - | - | - | -0.414* | - | | | | | | (0.181) | | | Slippage Ratio (annualized) | - | - | - | - | -1.180*** | | | | | | | (0.238) | | Number of Observations | 30 | 30 | 30 | 30 | 30 | | Adjusted R2 | -0.07 | 0.11 | 0.09 | 0.08 | 0.43 | | BIC | 206.30 | 203.07 | 203.64 | 204.19 | 189.76 | Notes: 1. Figures in parenthesis represents standard errors

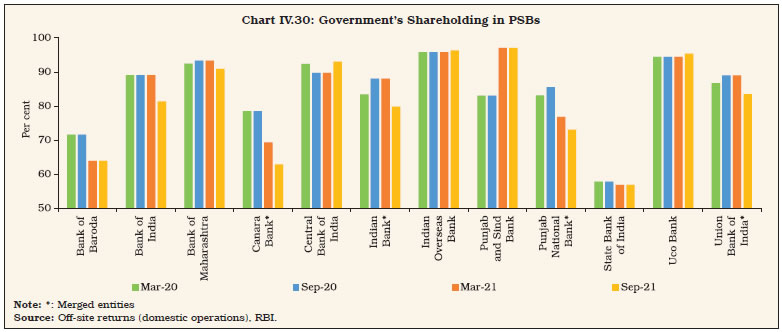

2. ***p < 0.001, **p < 0.01, *p < 0.5 | References Acharya, V. V., Engle III, R. F., & Steffen, S. (2021). Why did bank stocks crash during COVID-19? (No. w28559). National Bureau of Economic Research. Demirgüç-Kunt, A., Pedraza, A., & Ruiz-Ortega, C. (2021). Banking sector performance during the covid-19 crisis. Journal of Banking & Finance, 106305. Mathur, A., Sengupta, R., & Pratap, B. (2021). Saved by the bell? Equity market responses to surprise Covid-19 lockdowns and central bank interventions. (Forthcoming) MacKinlay, A. C. (1997). Event Studies in Economics and Finance. Journal of Economic Literature, 35(1), 13–39. | 7. Ownership Pattern in Commercial Banks IV.57 Government ownership in Canara Bank, Punjab National Bank, Indian Bank and Union Bank of India increased substantially following the amalgamation of ten PSBs into four, effective from April 1, 202016. During H2:2020-21, the government’s shareholding increased in Punjab and Sind Bank due to recapitalisation17 and decreased in Bank of Baroda, Canara Bank, Punjab National Bank and State Bank of India, owing to capital raising through private placements (Chart IV.30). Furthermore, as at end-September 2021, government shareholding decreased in Bank of India, Bank of Maharashtra, Canara Bank, Indian Bank, Punjab National Bank and Union Bank of India on account of raising of fresh equity from the market. Capital infusions planned for PSBs during 2021-22 are expected to change their ownership pattern further18.  IV.58 During the year, one private sector bank, Lakshmi Vilas Bank Limited, amalgamated with a foreign bank, DBS Bank India Limited, with effect from November 27, 2020. With this, 21 PVBs were operational in India as at end-March 2021. In terms of foreign investments, non-residents’ shareholding was well within the limits of 74 per cent for PVBs including Local Area Banks (LABS) and Small Finance Banks (SFBs) and 20 per cent for PSBs (Appendix Table IV.5). 8. Corporate Governance IV.59 Effective governance and balanced compensation practices in banks are important risk mitigation tools as they boost depositors’ confidence and also reinforce financial stability. Following the discussion paper on ‘Governance in Commercial Banks in India’ issued in June 2020 and the feedback received thereon, the Reserve Bank issued an interim set of instructions addressing several operational subjects on April 26, 2021. 8.1 Composition of Boards IV.60 Apart from ensuring competency, diversity and meeting the fit-and-proper criterion, appointment of independent directors goes a long way in ensuring board effectiveness. Most PVBs in India have achieved this in varying degrees, with the dominant presence of independent directors on their boards as well as in their key supervisory committees, including the Audit Committee of the Board (ACB), Risk Management Committee of the Board (RMCB) and Nomination and Remuneration Committee (NRC) (Chart IV.31). IV.61 It is also necessary to limit the presence of management on the board and key supervisory committees to ensure functional independence. Ensuring that the Chair of the board is not a member of these committees helps minimise role conflicts. The share of PVBs where the Chair is not a member of an ACB increased to 47 per cent at end-March 2021 from 35 per cent a year ago. However, the share remained unchanged at 29 per cent in the case of RMCBs19. 8.2 Executive Compensation IV.62 The compensation paid to a bank Chief Executive Officer (CEO) in comparison to a representative bank employee varies greatly across different bank groups. For PSBs, on an average, CEOs earn 3 times the typical employee20, while the same was as high as 75 times in the case of SFBs and 67 times in the case of PVBs. The corresponding multiple was low for FBs as the remuneration received by employees is relatively high. The variation across bank groups remained consistent through 2018-19 and 2019-20 (Chart IV.32). IV.63 Revised guidelines on compensation21 require that the compensation of CEOs / Whole Time Directors (WTDs) / Material Risk Takers (MRTs) must be adjusted for all types of risk, their outcomes and time horizons. Moreover, the mix of cash, equity and other forms of payment must be consistent with risk alignment, wherein the variable pay component should be in the range of 50 to 75 per cent of the total pay, a minimum of 60 per cent of which should be under deferral arrangements. The cash component of variable pay is also capped between 33 to 50 per cent22 under the revised guidelines (Chart IV.33).

9. Foreign Banks’ Operations in India and Overseas Operations of Indian Banks IV.64 During 2020-21, the number of FBs operating in the country reduced as compared to a year ago23, however, total branches of FBs increased due to amalgamation of Lakshmi Vilas Bank with DBS Bank, with effect from, November 27, 2020 (Table IV.19). On the other hand, PSBs have been reducing their overseas presence for the last three and a half years to achieve greater cost efficiency. PVBs also shut down their less profitable operations abroad during the year (Appendix Table IV.6). | Table IV.19: Operations of Foreign Banks in India | | | Foreign banks operating through branches | Foreign banks having representative offices | | No. of Banks | Branches | | Mar-16 | 46 | 325 | 39 | | Mar-17 | 44 | 295 | 39 | | Mar-18 | 45 | 286 | 40 | | Mar-19 | 45# | 299* | 37 | | Mar-20 | 46# | 308* | 37 | | Mar-21 | 45# | 874* | 36 | Notes: 1. #: Includes two foreign banks, namely SBM Bank (India) Limited and DBS Bank India Limited which are operating through Wholly Owned Subsidiary (WOS) mode.

2. *: Includes branches of SBM Bank (India) Limited and DBS Bank India Limited (including branches of amalgamated entity i.e. Lakshmi Vilas Bank as on March 2021) operating through WOS mode

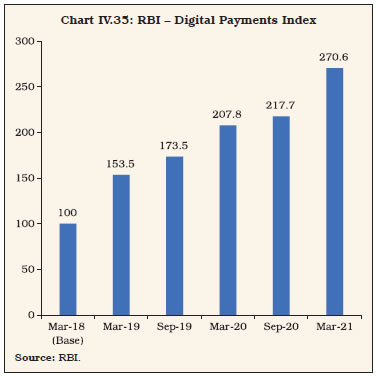

Source: RBI. | 10. Payment Systems and Scheduled Commercial Banks IV.65 The payment systems landscape in India is undergoing transformation due to rapid technological advancements and innovations, complemented by supportive regulatory policies. The Reserve Bank’s Payment and Settlement Systems: Vision 2019-2021 envisaged payment systems that are not just safe and secure, but are also efficient, fast and affordable. In addition, there has been a greater thrust by the government for rapid adoption of digital payment services by all segments of the society. IV.66 Digital modes of payments have grown by leaps and bounds over the last few years. As a result, conventional paper-based instruments such as cheques and demand drafts now constitute a negligible share (Chart IV.34). IV.67 The growth in volume of total payments decelerated to 26.7 per cent during 2020-21 from 43.7 per cent a year ago. In terms of value, total payments contracted for the second consecutive year, mainly due to decline in value of transactions via RTGS and paper-based instruments (Table IV.20).

| Table IV.20: Payment Systems Indicators | | Item | Volume (Lakh) | Value (₹ Crore) | | 2018-19 | 2019-20 | 2020-21 | 2018-19 | 2019-20 | 2020-21 | | 1. Large Value Credit Transfers – RTGS | 1,366 | 1,507 | 1,592 | 13,56,88,187 | 13,11,56,475 | 10,55,99,849 | | 2. Credit Transfers | 1,18,481 | 2,06,297 | 3,17,868 | 2,60,90,471 | 2,85,56,593 | 3,35,04,226 | | 2.1 AePS (Fund Transfers) | 11 | 10 | 11 | 501 | 469 | 623 | | 2.2 APBS | 14,949 | 16,747 | 14,373 | 86,226 | 99,048 | 1,11,001 | | 2.3 ECS Cr | 54 | 18 | - | 13,235 | 5,146 | - | | 2.4 IMPS | 17,529 | 25,792 | 32,783 | 15,90,257 | 23,37,541 | 29,41,500 | | 2.5 NACH Cr | 8,834 | 11,100 | 16,465 | 7,29,673 | 10,37,079 | 12,16,535 | | 2.6 NEFT | 23,189 | 27,445 | 30,928 | 2,27,93,608 | 2,29,45,580 | 2,51,30,910 | | 2.7 UPI | 53,915 | 1,25,186 | 2,23,307 | 8,76,971 | 21,31,730 | 41,03,658 | | 3. Debit Transfers and Direct Debits | 4,914 | 6,027 | 10,457 | 5,24,556 | 6,05,939 | 8,65,520 | | 3.1 BHIM Aadhaar Pay | 68 | 91 | 161 | 815 | 1,303 | 2,580 | | 3.2 ECS Dr | 9 | 1 | - | 1,260 | 39 | - | | 3.3 NACH Dr | 4,830 | 5,842 | 9,646 | 5,22,461 | 6,04,397 | 8,62,027 | | 3.4 NETC (linked to bank account) | 6 | 93 | 650 | 20 | 200 | 913 | | 4. Card Payments | 61,769 | 72,384 | 57,787 | 11,96,888 | 14,34,813 | 12,91,799 | | 4.1 Credit Cards | 17,626 | 21,773 | 17,641 | 6,03,413 | 7,30,894 | 6,30,414 | | 4.2 Debit Cards | 44,143 | 50,611 | 40,146 | 5,93,475 | 7,03,920 | 6,61,385 | | 5. Prepaid Payment Instruments | 46,072 | 53,811 | 49,743 | 2,13,323 | 2,15,558 | 1,97,696 | | 6. Paper-based Instruments | 11,238 | 10,414 | 6,704 | 82,46,065 | 78,24,822 | 56,27,108 | | Total - Retail Payments (2+3+4+5+6) | 2,42,473 | 3,48,933 | 4,42,557 | 3,62,71,304 | 3,86,37,726 | 4,14,86,348 | | Total Digital Payments (1+2+3+4+5) | 2,32,602 | 3,40,026 | 4,37,445 | 16,37,13,425 | 16,19,69,379 | 14,14,59,089 | | Total Payments (1+2+3+4+5+6) | 2,43,839 | 3,50,440 | 4,44,149 | 17,19,59,490 | 16,97,94,201 | 14,70,86,197 | Notes: 1. RTGS system includes customer and inter-bank transactions only.

2. The figures for cards are for transactions at point of sale (POS) terminals only, which include online transactions.

3. Figures in the columns might not add up to the total due to rounding off of numbers.

4. -: nil

Source: RBI. | 10.1 Digital Payments IV.68 In recent years, the Reserve Bank has been encouraging wider adoption of digital modes of payments and strengthening of the required infrastructure. The pandemic provided a fillip to the faster adoption of retail digital payments. 24x7x365 availability of Centralised Payment Systems (CPS) i.e., National Electronic Funds Transfer (NEFT) and Real Time Gross Settlement (RTGS), with effect from December 2019 and December 2020, respectively, reduced risks and enhanced efficiency of the entire payments ecosystem. Subsidies provided through the Payment Infrastructure Development Fund (PIDF), operationalised in January 2021, have helped to develop infrastructure in Tier-3 to Tier-6 centres and north-eastern states and are expected to give a boost, going forward. Granting non-bank Payment System Providers (PSPs)24 direct access to the CPS will widen the reach of digital financial services to all segments of users. IV.69 RTGS, which facilitates high value transactions on real time basis, dominates the digital payments space in value terms. On the other hand, Unified Payments Interface (UPI) from the retail segment has a majority share in transaction volume. The robust growth in transactions using innovative payment systems such as National Electronic Toll Collection (NETC), BHIM Aadhaar Pay and Aadhaar Enabled Payment System (AePS) points to greater acceptability of contactless payments during the year (Table IV.20). To measure the progress of digitisation and assess the deepening and penetration of digital payments, the Reserve Bank launched a composite Digital Payments Index (DPI) in January 2021, comprising five broad parameters (weights indicated in brackets) – (i) payment enablers (25 per cent); (ii) payment infrastructure – demand-side factors (10 per cent); (iii) payment infrastructure – supply-side factors (15 per cent); (iv) payment performance (45 per cent); and (v) consumer centricity (5 per cent). The index is computed semi-annually, with March 2018 as the base period (Chart IV.35).  10.2 ATMs IV.70 During 2020-21, the total number of automated teller machines (ATMs) (on-site and off-site) operated by SCBs increased for the second consecutive year after declining in 2018-19. The number of PSB ATMs, however, declined in their pursuit of greater cost efficiency by leveraging network externalities (Table IV.21, Appendix Table IV.7). | Table IV.21: Number of ATMs | | (At end-March) | | Sr. No. | Bank Group | On-Site ATMs | Off-site ATMs | Total Number of ATMs | | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | | I | PSBs | 80,691 | 78,007 | 57,855 | 59,106 | 1,38,546 | 1,37,113 | | II | PVBs | 30,483 | 34,828 | 38,886 | 37,566 | 69,369 | 72,394 | | III | FBs | 225 | 690 | 678 | 1,135 | 903 | 1,825 | | IV | SFBs* | 1,870 | 2,079 | 56 | 52 | 1,926 | 2,131 | | V | PBs# | 2 | 1 | 14 | 111 | 16 | 112 | | VI | WLAs | - | - | - | - | 23,597 | 25,013 | | VII | All SCBs (I to V) | 1,13,271 | 1,15,605 | 97,489 | 97,970 | 2,10,760 | 2,13,575 | | VIII | Total (VI+VII) | - | - | - | - | 2,34,357 | 2,38,588 | Notes: 1. *: 10 scheduled SFBs as at end-March 2020 and end-March 2021.

2. #: 1 scheduled PB (Paytm Payments Bank) as at end-March 2020 and end-March 2021.