[Under Section 45ZL of the Reserve Bank of India Act, 1934] The sixteenth meeting of the Monetary Policy Committee (MPC), constituted under section 45ZB of the Reserve Bank of India Act, 1934, was held from April 2 to 4, 2019 at the Reserve Bank of India, Mumbai. 2. The meeting was attended by all the members – Dr. Chetan Ghate, Professor, Indian Statistical Institute; Dr. Pami Dua, Director, Delhi School of Economics; Dr. Ravindra H. Dholakia, former Professor, Indian Institute of Management, Ahmedabad; Dr. Michael Debabrata Patra, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934); Dr. Viral V. Acharya, Deputy Governor in charge of monetary policy – and was chaired by Shri Shaktikanta Das, Governor. 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely: -

the resolution adopted at the meeting of the Monetary Policy Committee; -

the vote of each member of the Monetary Policy Committee, ascribed to such member, on the resolution adopted in the said meeting; and -

the statement of each member of the Monetary Policy Committee under sub-section (11) of section 45ZI on the resolution adopted in the said meeting. 4. The MPC reviewed the surveys conducted by the Reserve Bank to gauge consumer confidence, households’ inflation expectations, corporate sector performance, credit conditions, the outlook for the industrial, services and infrastructure sectors, and the projections of professional forecasters. The MPC also reviewed in detail staff’s macroeconomic projections, and alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today decided to: Consequently, the reverse repo rate under the LAF stands adjusted to 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate to 6.25 per cent. The MPC also decided to maintain the neutral monetary policy stance. These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 6. Since the last MPC meeting in February 2019, global economic activity has been losing pace. In the US, the subdued performance in the final quarter of 2018 appears to have continued into Q1:2019 as reflected in declining factory activity. The Euro area slowed down in Q4:2018 on soft domestic demand and contracting manufacturing activity. Of its constituents, the Italian economy contracted for two consecutive quarters in Q3 and Q4. In the UK, growth slowed down on Brexit uncertainty, with industrial production contracting during September-January. The Japanese economy rebounded in Q4 on increased domestic consumption expenditure and recovering investment spending. However, the latest data on manufacturing activity and business confidence suggest that growth lost momentum in Q1:2019. The monetary policy stances of the US Fed and central banks in other major advanced economies (AEs) have turned dovish. 7. Economic activity also slowed down in some major emerging market economies (EMEs). The Chinese economy decelerated in Q4:2018 on subdued domestic and global demand impacting industrial activity. Much of this weakness seems to have continued into 2019 as reflected in low factory output in Q1, though the purchasing managers’ index (PMI) moved into expansion zone in March after three months of contraction. In Q1, the Russian economy continued to be impacted by both domestic and external headwinds. The Brazilian economy ended 2018 on a weak note; going into 2019, available economic indicators for Q1 suggest that economic activity remained restrained by both weak domestic and external demand. The South African economy slowed down in the final quarter of 2018. Subdued industrial activity and worsening external demand point to a further loss in momentum in Q1. 8. Crude oil prices have risen on production cuts by OPEC and Russia as well as disruption in supplies due to US sanctions on exports from Venezuela. Gold prices weakened on expectations of positive outcomes of the China-US trade deal. Inflation continued to remain low in major AEs and many key EMEs due to slowing global growth and stable or falling commodity prices. 9. Financial markets continued to be driven by monetary policy stances of key central banks and movements in crude oil prices. In the US, the equity market witnessed some selling pressure in the last week of March on weak economic data. Equity markets in EMEs gained, benefitting from country-specific factors and easing of global financing conditions. Bond yields in the US softened, slipped into negative territory in Germany and dipped further into negative territory in Japan as central banks signalled softer stances. Bond yields in most EMEs have been falling in tandem with those in AEs and on the improving inflation outlook. In currency markets, the US dollar has traded with an appreciating bias in recent weeks. EME currencies have traded with a depreciating bias on country-specific factors and on fears of a weakening economic outlook in China. Domestic Economy 10. Turning to the domestic economy, the second advance estimates for 2018-19 released by the Central Statistics Office (CSO) in February 2019 revised India’s real gross domestic product (GDP) growth downwards to 7.0 per cent from 7.2 per cent in the first advance estimates. Domestic economic activity decelerated for the third consecutive quarter in Q3:2018-19 due to a slowdown in consumption, both public and private. However, gross fixed capital formation (GFCF) growth remained in double digits for the fifth consecutive quarter in Q3, with the GFCF to GDP ratio rising to 33.1 per cent in Q3:2018-19 against 31.8 per cent in Q3:2017-18, supported primarily by the government’s thrust on the road sector and affordable housing. The drag on aggregate demand from net exports also moderated in Q3 due to a marginal acceleration in exports and a sharp deceleration in imports led by a decline in crude oil prices. 11. On the supply side, the second advance estimates of the CSO placed the growth of real gross value added (GVA) lower at 6.8 per cent in 2018-19 as compared with 6.9 per cent in 2017-18. GVA growth slowed down to 6.3 per cent in Q3 due to a deceleration in agriculture output from the record level achieved in the previous year. Industrial GVA growth remained unchanged in Q3, with manufacturing GVA growth slowing somewhat. Services GVA growth also remained unchanged in Q3; while growth in construction activity accelerated, there was some loss of momentum in public administration, defence and other services. 12. Beyond Q3, the second advance estimates of foodgrains production for 2018-19 at 281.4 million tonnes were 1.2 per cent lower than the fourth advance estimates of 2017-18, but 1.4 per cent higher than the second advance estimates of 2017-18. According to the National Oceanic and Atmospheric Administration (NOAA) of the US, El Niño conditions strengthened during February 2019, which may affect the prospects of a normal south west monsoon. 13. Of the high frequency indicators of industry, the manufacturing component of the index of industrial production (IIP) growth slowed down to 1.3 per cent in January 2019 due to automobiles, pharmaceuticals, and machinery and equipment. The growth of eight core industries remained sluggish in February. Credit flows to micro and small as well as medium industries remained tepid, though they improved for large industries. Capacity utilisation (CU) in the manufacturing sector, however, as measured by the Reserve Bank’s order books, inventory and capacity utilisation survey (OBICUS), improved to 75.9 per cent in Q3 from 74.8 per cent in Q2 exceeding its long-term average; the seasonally adjusted CU rose to 76.1 per cent from 75.4 per cent. The business assessment index of the industrial outlook survey (IOS) points to an improvement in overall sentiments in Q4. The manufacturing purchasing managers’ index (PMI) remained in expansion zone for 20th month in March. The key indicators of investment activity contracted, viz., production of capital goods in January and imports of capital goods in February. 14. High frequency indicators of the services sector suggest significant moderation in activity. Sales of commercial vehicles contracted during February. Other indicators of the transportation sector, viz., port freight traffic and international air freight traffic, also contracted. However, indicators of the construction sector, viz., consumption of steel and production of cement, continued to show healthy growth. The hotels sub-segment showed some improvement in foreign tourist arrivals in January and international air passenger traffic in February. The services PMI continued to be in expansion zone for the tenth consecutive month in March 2019. 15. Retail inflation, measured by y-o-y change in the CPI, rose to 2.6 per cent in February after four months of continuous decline. The uptick in inflation was driven by an increase in prices of items excluding food and fuel and weaker momentum of deflation in the food group. However, inflation in the fuel group collapsed to its lowest print in the new all India CPI series. 16. Within the food group, deflation in four sub-groups – vegetables, sugar, pulses and fruits – continued in February. Egg prices moved into inflation after remaining in deflation in previous three months, while inflation ticked up in all other food sub-groups. 17. Inflation in the fuel and light sub-group collapsed from 4.5 per cent in December to 1.2 per cent in February. Prices of liquefied petroleum gas (LPG) declined sharply, pulled down by the lagged impact of the softening of international energy prices. The prices of firewood, with the second largest weight in the fuel group, also declined. Electricity slipped into deflation in January and February. Inflation in kerosene remained elevated, however, reflecting the impact of the calibrated increase in its administered price. 18. CPI inflation excluding food and fuel declined to 5.2 per cent in January, but rose to 5.4 per cent in February, driven by a broad-based pick-up in inflation in the personal care and effects, and recreation and amusement sub-groups. However, inflation in the clothing and footwear, and transport and communication sub-groups fell, the latter reflecting the reduction in petrol and diesel prices. Inflation in the health and education sub-groups remained elevated, even though it moderated markedly during January-February vis-à-vis December. 19. Inflation expectations, measured by the Reserve Bank’s survey of households, declined in the February round over the previous round by 40 basis points each for the three months ahead and for the one year ahead horizons. Firms participating in the Reserve Bank’s industrial outlook survey of manufacturing companies reported reduction in input price pressures, but they expected an increase in staff expenses in Q1:2019-20. Farm and industrial input costs increased at a slow pace in January-February 2019. Nominal growth in rural wages and staff costs in the organised manufacturing and services sectors remained muted in Q3:2018-19. 20. From a daily net average surplus of ₹27,928 crore (₹279 billion) during February 1-6, 2019, systemic liquidity moved into deficit during February 7 - March 31, reflecting the build-up of government cash balances. Currency in circulation expanded sharply in February-March. The liquidity needs of the system were met through injection of durable liquidity amounting to ₹37,500 crore (₹375 billion) in February and ₹25,000 crore (₹250 billion) in March through open market purchase operations (OMOs). Consequently, total durable liquidity injected by the Reserve Bank through OMOs aggregated ₹2,98,500 crore (₹2,985 billion) for 2018-19. Liquidity injected under the LAF, on an average daily net basis, was ₹95,003 crore (₹950 billion) during February (February 7-28, 2019) and ₹57,043 crore (₹570 billion) in March. The weighted average call rate (WACR) remained broadly aligned with the policy repo rate in February and March. 21. Anticipating the seasonal tightening of liquidity at end-March, the Reserve Bank conducted four longer term (tenor ranging between 14-day and 56-day) variable rate repo auctions during the month in addition to the regular 14-day variable rate term repo auctions. Furthermore, the Reserve Bank conducted long-term foreign exchange buy/sell swaps of US$ 5 billion for a tenor of 3 years on March 26, 2019, thereby injecting durable liquidity of ₹34,561 crore (₹346 billion) into the system. 22. Export growth remained weak in January and February 2019 mainly due to exports of petroleum products decelerating in response to a fall in international crude oil prices. Among non-oil exports, engineering goods, chemicals, leather and marine products recorded either sequentially lower or negative growth. As in the case of exports, lower international crude oil prices downsized the oil import bill. Non-oil non-gold imports declined sharply, dragged down by the subdued demand for pearls and precious stones, transport equipment, project goods and vegetable oils. The trade deficit narrowed in February 2019 – both sequentially and on a year-on-year basis – to its lowest level in 17 months. This, along with the increase in services exports and lower outgo of income payments, resulted in narrowing of the current account deficit sequentially. On the financing side, net FDI inflows were strong in April-January 2018-19. Foreign portfolio investors turned net buyers in the domestic capital market in Q4:2018-19. India’s foreign exchange reserves were at US$ 412.9 billion on March 31, 2019. Outlook 23. In the sixth bi-monthly monetary policy resolution of February 2019, CPI inflation was projected at 2.8 per cent for Q4:2018-19, 3.2-3.4 per cent for H1:2019-20 and 3.9 per cent for Q3:2019-20, with risks broadly balanced around the central trajectory. Actual inflation outcomes averaged 2.3 per cent in January-February. 24. The inflation path during 2019-20 is likely to be shaped by several factors. First, low food inflation during January-February will have a bearing on the near-term inflation outlook. Second, the fall in the fuel group inflation witnessed at the time of the February policy has become accentuated. Third, CPI inflation excluding food and fuel in February was lower than expected, which has imparted some downward bias to headline inflation. Fourth, international crude oil prices have increased by around 10 per cent since the last policy. Fifth, inflation expectations of households as well as input and output price expectations of producers polled in the Reserve Bank’s surveys have further moderated. Taking into consideration these factors and assuming a normal monsoon in 2019, the path of CPI inflation is revised downwards to 2.4 per cent in Q4:2018-19, 2.9-3.0 per cent in H1:2019-20 and 3.5-3.8 per cent in H2:2019-20, with risks broadly balanced. 25. GDP growth for 2019-20 in the February policy was projected at 7.4 per cent in the range of 7.2-7.4 per cent in H1, and 7.5 per cent in Q3 – with risks evenly balanced. Since then, there are some signs of domestic investment activity weakening as reflected in a slowdown in production and imports of capital goods. The moderation of growth in the global economy might impact India’s exports. On the positive side, however, higher financial flows to the commercial sector augur well for economic activity. Private consumption, which has remained resilient, is also expected to get a fillip from public spending in rural areas and an increase in disposable incomes of households due to tax benefits. Business expectations continue to be optimistic. Taking into consideration the above factors, GDP growth for 2019-20 is projected at 7.2 per cent – in the range of 6.8-7.1 per cent in H1:2019-20 and 7.3-7.4 per cent in H2 – with risks evenly balanced.   26. Beyond the near term, several uncertainties cloud the inflation outlook. First, with the domestic and global demand-supply balance of key food items expected to remain favourable, the short-term outlook for food inflation remains benign. However, early reports suggest some probability of El Niño effects in 2019. There is also the risk of an abrupt reversal in vegetable prices, especially during the summer months. Second, inflation in fuel group items, particularly electricity, firewood and chips saw unprecedented softening in H2:2018-19. There is, however, uncertainty about the sustainability of this softening in inflation in fuel items. Third, the outlook for oil prices continues to be hazy, both on the upside and the downside. On the one hand, continuing OPEC production cuts will reduce supplies. On the other hand, there is considerable uncertainty about demand conditions. Should there be a swift resolution of trade tensions, a pick-up in global demand is likely to push up oil prices. However, should trade tensions linger and demand conditions worsen, crude prices may fall from current levels, despite production cuts by OPEC. Fourth, inflation excluding food and fuel has remained elevated over the past twelve months with some pick up in prices in February. However, should the recent slowdown in domestic economic activity accentuate, it may have a bearing on the outlook for inflation in this category. Fifth, financial markets remain volatile reflecting in part global growth and trade uncertainty, which may have an influence on the inflation outlook. Sixth, the fiscal situation at the general government level requires careful monitoring. 27. The MPC notes that the output gap remains negative and the domestic economy is facing headwinds, especially on the global front. The need is to strengthen domestic growth impulses by spurring private investment which has remained sluggish. 28. Against this backdrop, the MPC decided to reduce the policy repo rate by 25 basis points and maintain the neutral stance of monetary policy. 29. Dr. Pami Dua, Dr. Ravindra H. Dholakia, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted in favour of the decision to reduce the policy repo rate by 25 basis points. Dr. Chetan Ghate and Dr. Viral V. Acharya voted to keep the policy rate unchanged. 30. Dr. Chetan Ghate, Dr. Pami Dua, Dr. Michael Debabrata Patra, Dr. Viral V. Acharya and Shri Shaktikanta Das voted in favour of the decision to maintain the neutral stance of monetary policy. Dr. Ravindra H. Dholakia voted to change the stance from neutral to accommodative. 31. The minutes of the MPC’s meeting will be published by April 18, 2019. 32. The next meeting of the MPC is scheduled during June 3, 4 and 6, 2019. Voting on the Resolution to reduce the policy repo rate by 25 bps to 6.0 per cent | Member | Vote | | Dr. Chetan Ghate | No | | Dr. Pami Dua | Yes | | Dr. Ravindra H. Dholakia | Yes | | Dr. Michael Debabrata Patra | Yes | | Dr. Viral V. Acharya | No | | Shri Shaktikanta Das | Yes | Statement by Dr. Chetan Ghate 33. Since the last review, the continual decline in both 3 month and 1 year ahead inflationary expectations of households is encouraging. Households’ current inflation perception is below 7%. The percentage of respondents expecting inflation below 6% for 3 month and 1 year ahead horizons has also been increasing over different survey rounds. It should be noted that although the 1 year ahead inflationary expectation declined by 40 bps to 8.1% compared to the previous round it is still only 50 bps below the March 2018 value (8.6%). 34. The elevated level of inflation ex food and fuel continues to be a concern, although I am more sanguine about its trajectory after the last few prints. My major concern with inflation ex food and fuel is that sequential gains continue to be strong. Inflation ex food fuel will only be buttressed by the rise in crude prices (USD 68.3 on April 2 versus USD 62.2 on February 7, equivalent to a 9.8% increase since the last review). Crude prices have also remained resilient despite lower projections for global growth. Oil is not a “Hotelling” good (constraints in different locations prevent supply responses that would otherwise help in mitigating overall price rises). This makes inflation management challenging. 35. Food prices continue to be subdued although the extent of disinflation is falling. The unusually low summer uptick in food inflation (3.2%) combined with a sharp decline in winter prices in FY 19 has kept food prices unexpectedly low. The shift in momentum of food in the last couple of prints indicates that low food inflation has possibly reached a nadir. I re-iterate my concern from the last review: RBI’s projections for Q4 2019-2020 headline inflation continue to be on the lower side because of an assumed low momentum for food. If vegetable prices rebound in April-August in a stronger way, RBI’s projections will be easily breached. What compounds problems this time is the rise in the price of crude, although there has been an off-setting impact because of the nominal appreciation of the rupee (3.3% since the last review). It wouldn’t hurt to wait for a couple of months to watch the momentum on food inflation and other variables before taking a call on further rate cuts. 36. The major question in this review is whether there is sufficient accumulation of downside risks on growth to warrant a monetary policy response. Are the drivers of growth fading? 37. My sense is that that the business cycle depicts “early cycle” weakness. At this juncture, I see sub 7% growth rates confined possibly to just two quarters: Q3 and Q4 FY 19. These will be our “kitchen-sink” quarters (i.e., quarters where the most adverse outcomes to the economy are realized). Looking at the momentum on GDP growth (Q-o-Q SAAR), there has also been an uptick in Q3 FY 19. 38. Various RBI surveys don’t depict an economy in collapse. PMIs in Manufacturing and Services continue to be in expansion zone for several months, capacity utilization in the manufacturing sector has gone up sequentially in the last four quarters (76.1% seasonally adjusted in Q3), adjusted non-food credit grew by 14.8% in March 2019 compared with 11.3% in the last fiscal year, and there has been a sharp uptick in consumer confidence (a positive “sentiment shock”) with the future expectation index at an all-time high. 39. Notwithstanding this, what is worrying is the performance of private final consumption expenditures (PFCE), about 59% percent of GDP. A variety of high frequency indicators look fairly weak which nowcast a loss in growth momentum. 40. What confounds this however is the fairly robust numbers for PFCE growth (8.4% Q3 FY 19 and 9.8% Q2 FY 19), (although admittedly, this is partly due to the outsized role that livestock had in the PFCE numbers for Q3 FY 19). Looking at data from April 2017 – January 2019 for consumer durables, out of 22 months, only 6 months showed negative growth. For non-durables, only 2 months out of 22 months showed negative growth. Consumer durables growth in Q2 was 8.1% in FY 19, and 6.0% in Q3. Consumer non-durables growth was 6.1% in Q2 FY 19 dropping to 4.6% in Q3 FY 19. 41. Various consumption indicators therefore look mixed. 42. In contrast, GFCF (gross fixed capital formation) has risen over the past few quarters to 33.1% of GDP in Q3: 2018-2019. RBI’s study on “Private Corporate Investment in India: Slow Recovery Underway” and enterprise surveys depict planned capex showing a turn-around in 2018-2019, with inventory ratios moving down in manufacturing. 43. Somewhat worrying though is that the machine and equipment component of GFCF is showing signs of stress. 44. In terms of consumption-investment linkages, somewhat more concerning is some preliminary econometric evidence, using data from 1996: Q2 to 2018: Q4 that PFCE growth (quarter on quarter, seasonally adjusted) drives GFCF growth with a lag of two quarters. Simple Granger causality tests also suggest that consumption demand drives investment demand and not vice versa. This suggests that subdued consumption growth may cause investment growth to taper, signs of which should be carefully watched. 45. I continue to view the elevated levels of the combined fiscal deficit and the on-going thrust towards competitive populism as jeopardizing the durability of inflation in the medium term. This should be carefully watched. 46. On the external front, while India’s overall growth rates have always been somewhat immune to our export performance, I view the muted performance of exports and imports over the last four months with concern. 47. Given the above reasons, maintaining status quo on rates at the current juncture would be consistent with sustainable growth in the economy and achieving the inflation target over the medium-term. Contrary to some of my colleagues in the MPC, I feel that frequent changes in policy rates and stance runs the risk of introducing uncertainty and volatility because of our own actions. 48. I will, however, carefully watch the incoming growth-inflation data and am open to a reassessment of my views. 49. I also vote to retain a neutral stance. Statement by Dr. Pami Dua 50. Headline inflation rose to 2.6% in February 2019 after four months of continuous decline. CPI inflation excluding food and fuel declined to 5.2% in January but increased to 5.4% in February, driven by an increase in personal care and effects, recreation and amusement sub-groups. On the basis of quarterly data, headline inflation fell from 4.8% in Q1: FY18-19 to 3.9% in Q2 and 2.6% in Q3. As per RBI projections, it is expected to decline to 2.4% in Q4 before rising to 2.9% in Q1: FY 19-20 and 3% in Q2. CPI excluding food and fuel has declined from 6.3% in Q1: FY 18-19 to 5.9% in Q3: FY 18-19. This softening in inflation is also exhibited in consumer and producer expectations. 51. Inflation expectations in the March 2019 round of the Reserve Bank’s Survey of Households softened by 40 basis points each for the three-month ahead and one-year ahead horizons, vis-à-vis the last round in December 2018. Further, the proportion of respondents expecting higher inflation declined. The gap between current inflation perceptions and expectations also narrowed, indicating anchoring of inflation expectations at a lower level. According to the January-March 2019 round of the Reserve Bank’s Industrial Outlook Survey, manufacturing firms expect a moderation in pressure in selling prices in Q1: 2019-20 with easing of input cost pressures. Salary costs, however, are expected to firm up. As per the Business Inflation Expectations Survey conducted by IIM-Ahmedabad in February 2019, businesses expect moderation in one-year-ahead CPI headline inflation from December 2018. The Economic Cycle Research Institute’s (ECRI) Indian Future Inflation Gauge, a harbinger of inflation, remains in a cyclical downswing, indicating that underlying inflation pressures are still subdued. 52. In the coming months, upside risks to inflation include a potentially weak monsoon; uncertainty in oil prices and how weaker global demand conditions may weigh against OPEC’s production decisions; volatility in financial markets; trade tensions; and the possibility of fiscal slippage. Downside risks include low food prices; moderation in inflation excluding food and fuel; and slowdown in global growth. 53. On the output side, RBI lowered its projection for GDP growth for 2019-20 from 7.4% in the February policy to 7.2%. Indicators paint a mixed picture, with weakening investment activity that is reflected in a slowdown in production and imports of capital goods. On the other hand, consumer confidence improved in the March 2019 round of RBI’s Consumer Confidence Survey, with an uptick in both current perceptions as well as future expectations, which is at an all-time high. This upward trajectory can be attributed to an improvement in sentiment with respect to general economic situation, employment scenario and price levels. According to RBI’s Order Books, Inventory and Capacity Utilization Survey (OBICUS), capacity utilisation in the manufacturing sector improved in Q3 from the previous quarter. The Business Expectations Index of RBI’s Industrial Outlook Survey, however, signals moderation in optimism in Q1: 2019-20. At the same time, the Purchasing Managers’ Index (PMI) remained in expansion zone for the twentieth month in March, while the services PMI continued in expansion zone for the tenth successive month in March 2019. Meanwhile, ECRI’s Indian Leading Index growth has increased in recent months, indicating an improved growth outlook. ECRI’s Indian Leading Exports Index growth continues to languish, however, suggesting that Indian exports growth will ease due to pessimistic prospects for global growth. 54. On the global front, ECRI’s international long leading indexes, including those for the U.S., Eurozone and China, are in continued cyclical downswings, pointing to a further slowdown in global growth. In fact, according to ECRI's 20-Country Long Leading Index, the global growth outlook is the worst it has been in three years. In the U.S., the Fed has not only doubled down on its abrupt about-face with regard to policy “normalization,” but also indicated that no rate hikes are planned this year, and only one rate hike is planned next year. As a result, the U.S. futures markets see no chance of a rate hike but some chance of a rate cut later this year, with some risk of recession. As expected, these cyclical prospects have resulted in an end to monetary policy “normalization” plans not only in the U.S., but also around the world, while opening up more room for policy easing. Meanwhile, ECRI’s international future inflation gauges, which are predictors of the direction of inflation, are pointing to the intensification of worldwide disinflation. Thus, the global prognosis is one of slow growth accompanied by benign inflation. 55. In view of the global growth slowdown and a benign global and domestic inflation outlook, I vote for decreasing the policy repo rate by 25 basis points and maintaining the neutral stance. Statement by Dr. Ravindra H. Dholakia 56. In the MPC meeting of February, 2019, I had explicitly stated that a space of 50 to 60 bps policy rate cut had opened up and that I would like to cut the repo rate by 25bps to begin with. Developments after the February MPC meeting have further opened up additional space of about 40 to 50 bps. The monthly headline CPI inflation prints of January and February 2019 have continued to undershoot the RBI projections substantially, forcing the RBI for further downward revision of headline inflation from 2.8 to 2.4 percent for Q4:FY 2018-19. Other developments on increase of USD 5 per barrel in crude oil prices, exchange rate appreciation, energy price revisions and monsoon expectations have all together led the RBI to revise its projections of the headline inflation trajectory downwards by 30-40 bps for the next 12 months. This is a very positive development on front of price stability in the economy and has opened up space for correcting the real interest rates in the system decisively. In my opinion, there are not even remote chances for the headline inflation to breach the medium term target of 4 percent substantially in foreseeable future for two consecutive quarters or even one quarter. On the other hand, there are serious concerns about the growth performance of economy. Global pessimism on growth and developments on domestic front have led the RBI to revise its growth projections downward for 2019-20. For 3 to 4 quarters in a row, from Q3:2018-19 to Q2:2019-20, the Indian economy is most likely to register a sub-seven percent real growth thereby substantially opening up an output gap exerting downward pressure on wage and price inflation. As per the mandate given to the MPC, under such circumstances, we need to give a sustained boost to the economy. I, therefore, vote for a change of stance from neutral to accommodative with a 25 bps cut in the policy repo rate, though I would have preferred to cut it by 35-40 bps this time. More precise reasons for my vote are as follows: -

Downward revision of the headline CPI inflation trajectory by RBI considers build up of substantial excess buffer stock of rice and wheat and prices of other food items like vegetables and fruits not experiencing the regular expected seasonal spikes reflecting structural corrections to control inflation in agri-commodities. -

While the crude oil prices show volatility and a recent rising tendency, their sustainability at higher levels is doubtful. Moreover, their pass-through to domestic inflation has also not occurred to the fullest extent in recent times. In my opinion, it may not be a major cause of worry for domestic inflation till it breaches the level of USD 80 – 85 per barrel on a durable basis, which is unlikely. -

Thus, oil prices, vegetable prices and fruit prices present volatile elements and any increase in them can at best be considered only temporary shocks as per our recent experience. They may not be considered durable shocks needing any policy response given the recent experience. -

The energy prices including electricity which have been subdued of late are likely to remain so for the next 10-12 months because any substantial price revisions are not on cards. The inflation ex-food and fuel is also likely to show a sharper decline in coming months because the inflationary expectations are getting anchored. -

As per the RBI survey, the household inflationary expectations 3 months and 12 months ahead continued to decline for the fourth consecutive bi-monthly round sharply and this time by 40 bps each. Moreover, the gap between the household perception and their expectations about inflation is narrowing over recent rounds. The IIM Ahmedabad survey of Businesses also show a continuing decline in their headline CPI inflationary expectations 12 months ahead by 53 bps. Thus, the inflationary expectations are getting anchored as is usually expected with any inflation targeting policy implementation. Even the RBI projections of the headline CPI inflation 12 months ahead have been below the targeted 4 per cent for two consecutive policies. The core inflation (with whatever definition but theoretically correct concept) will no longer be sticky at high levels and will show tendency towards the medium term target sooner than later. -

In this context, the concept and measurement of the output gap and more importantly its relationship with unemployment gap is crucial. On one hand, some economists argue that there is hardly any output gap (particularly if adjusted for financial factors); and on the other hand, several economists are emotionally arguing about existence of serious involuntary unemployment. These two contradictory views cannot be reconciled theoretically within the same macroeconomic model unless we consider measurement issues. Potential output and its growth in a rapidly developing emerging market economy like India needs to be measured differently than in a typical structurally stable and relatively slow growing advanced economy. Similarly, involuntary unemployment needs to be measured in such an economy avoiding all well-known limitations about disguised unemployment and underemployment. I have been consistently arguing that unless the real growth exceeds 8-8.5 percent per annum, the output gap reflecting the unemployment gap in the economy is not likely to close. Till that point, there would be downward pressure on the labour market and market determined wages and thereby on the so-called ‘core’ inflation. -

The downward revision of real growth from 7.4 to 7.2 percent for the coming year 2019-20 by RBI, therefore, opens up the output gap reflecting the unemployment gap substantially and needs a policy response. This is all the more so, because there are significant downside risks to the growth projection in my opinion. Due to global slowdown and US trade actions, our exports are already suffering. Investment has not revived to reach its earlier peak. The fiscal policy is constrained because of the lack of fiscal space and impending general elections. It is, therefore, the monetary policy that needs to provide the boost since, as per the mandate given to MPC, inflation is well under control. Cutting the policy rate gradually over time would correct the real interest rate in the economy and encourage investments. In this context, it is also relevant to note that most of the Central Banks globally have changed their tone to dovish. 57. This is the right time to act decisively. When the pitch is favourable and no possibility of bouncers or googlies coming in, a well set batsman has to score and not miss the opportunity to build the total by defending unnecessarily. I would, therefore, continue to cut the policy rate by 25bps and change the stance to accommodative indicating that any hikes in the rates are off the table for the time being. Statement by Dr. Michael Debabrata Patra 58. As anticipated by the MPC, inflation turned up in February 2019, lifted by food prices emerging out of five months of deflation. Three features of the upturn are noteworthy. 59. First, the January and February readings of inflation that became available after the MPC met last in February have undershot the projection made in that meeting. It is reasonable to expect that the March reading - that will become available on April 12 - may reveal that food prices are out of deflation, but headline inflation is still softer than the February meeting projection. I belabour this point because it informs the error correction process that is concurrently taking place. 60. Second, the entire inflation projection path of the MPC's April 2019 meeting has shifted downwards by 30-40 basis points from its trajectory in the February meeting. This is important in a forward-looking sense because as intermediate variables that provide a first glimpse of monetary policy's unseen and moving targets, the projections are indicating that the primary mandate assigned to the MPC appears secured at this juncture – inflation will likely remain at or below target over the 12-month horizon for which forecasts are available. 61. Third, the one year ahead projection of inflation seems to be validated by incoming data. Survey results indicate that households, businesses and professional forecasters have become more optimistic on the inflation outlook than before over the same time horizon. In the case of households, there is also evidence of the anchoring of expectations. Consumer confidence in the inflation outlook remaining benign over the year ahead is rising. Signals extracted from all this information would argue that if the primary target for monetary policy is likely to be achieved on a durable basis, some space opens up for policy attention to the objective of growth as enjoined by the RBI Act. 62. Given this headroom, the dilemma is two-fold: (1) with growth expected to accelerate from 7 per cent in 2018-19 to 7.2 per cent in 2019-20, is policy support really needed? (2) even if the case is admissible, is it the right time to steer monetary policy in defence of growth? Why not exercise prudence and wait and watch for durable signs of underlying pressures on inflation other than food or fuel easing, and/or indications that the slowdown in growth is not a soft patch but a cyclical downswing? This may avoid wasting ammunition. 63. To speak to these questions, the baseline projection of growth is subject to downside risks. First, we are already living in a world in which India’s real GDP growth averaged 6.5 per cent in the second half of 2018-19, not 7 per cent. Even if the horizon is extended to incorporate the projections for the first half of 2019-20, real GDP growth is still expected to be sub-7 per cent. Second, the drivers of growth are fading. Data that have arrived since the MPC’s February meeting indicate that demand conditions in the manufacturing sector are slowing down, with the weakening of sales of fast moving consumer goods implying that consumption spending may be losing steam. Meanwhile, capacity utilisation in manufacturing is running above trend in the absence of investment in new capacity. This suggests that the current pace of growth could be difficult to sustain if the capex cycle does not start up soon. Given the limited fiscal space, the support from government final consumption expenditure (GFCE) that has held up growth – GDP growth excluding GFCE was 6.3 per cent in 2017-18 (as against the headline GDP growth of 7.2 per cent) and 6.8 per cent in 2018-19 (7.0 per cent)1 – may not be available going forward. Exports have flattened, with the slowing down of global growth and trade imparting downside risks. Non-oil non-gold imports have contracted, indicative of weakening domestic demand. 64. Third, I continue to maintain the view that the biggest risks to growth are global. Some of these risks are already materialising. Global growth estimates and projections are being marked down as incoming data confirm the loss of momentum that is underway. Capital flows to EMEs have returned after a turbulent year gone by, but safe haven demand restrains a fuller resumption, and uncertainty in financial markets remains high. Crude prices are firming up, with financialisation of energy stocks adding upside. 65. Monetary policy has a overarchingly domestic orientation. With inflation being quiescent and growth at risk, I vote for a reduction in the policy rate by 25 basis points while maintaining a neutral policy stance. I will, however, remain watchful about the upturn in food prices that usually precedes the onset of the monsoon. Statement by Dr. Viral V. Acharya 66. In the minutes of the February 2019 Monetary Policy Committee (MPC) meeting, I had provided several reasons for why I had voted to keep the policy rate at 6.5% and the stance at neutral. 67. Since then, the headline inflation prints have revealed further softening of inflation in January, followed by a pick-up in February. Notably, inflation excluding food and fuel softened unexpectedly in January, while reverting somewhat in February; nevertheless, it remains uncomfortably close to 5.5%. Food inflation, in contrast, has behaved more in line with the expectations; fuel inflation has remained unusually weak. 68. As per my assessment, these outcomes combined with a further softening of household inflation expectations and a marginal opening up of the output gap (traditional measure), would have justified a rate cut of 25 basis points from 6.5% to 6.25% at the April meeting. In particular, the softening of inflation excluding food and fuel gives greater durability to the inflation path remaining around the target rate of 4% in the medium term even if the policy rate were to be reduced from 6.5% to 6.25%. However, given that the MPC had already cut the policy rate to 6.25% at its February meeting, the relevant decision now for me was whether to reduce the policy rate further from 6.25%. 69. I vote for keeping the policy rate unchanged at 6.25% for similar reasons as echoed in my February meeting statement, with some additional uncertainties that I flag below. 70. First, oil prices have marched upwards by an additional 10% since the February policy. This rise has taken the Brent Crude price closer to $70 per barrel. Its momentum cannot be taken lightly given the uncertainty witnessed last year on oil prices and the pressure it puts on inflation, the external sector and financial markets. While the pass-through to consumers remains somewhat incomplete at present, it will eventually hit the pump prices and generalise through transportation fares into non-fuel components of headline inflation. 71. Second, food deflation has attendant fiscal risks, as I explained in detail in my February meeting statement. Fiscal responses to deal with agrarian distress resulting from low food prices can impart a significant upside risk to the inflation trajectory, an uncertainty that may get partly resolved in the coming months. 72. Third, let me reiterate that inflation excluding food and fuel remains uncomfortably close to 5.5%, i.e., at elevated levels as through most of the past twelve months. This is confirmed also in rising staff costs in the formal sector. Conversely, it is only the benign food inflation that is allowing the monetary policy to not respond to the discomforting elevated levels of inflation excluding food and fuel. An important observation on food inflation is in order; in all of recent years, even as the level of food inflation has trended downward, it has remained highly volatile within each year; peak-to-trough cycle in food inflation typically tends to be of around 8 months duration, and the month of February has already shown some seasonal uptick in prices of several food items. Hence, soft food inflation may not persist for long, a scenario in which the elevated level of inflation excluding food and fuel would steer the headline inflation away from the target rate of 4%. This can risk hardening of inflation expectations of households. 73. Fourth, professional forecasters are pegging inflation trajectory somewhat higher than that of the Reserve Bank; this is due to their factoring in some fiscal slippage for this year as well as post-election, as gathered from their qualitative responses. Dissaving induced by such fiscal slippage also creates a rather weak transmission of monetary policy to the private and household sectors of the economy as bank deposits compete with small savings and corporate bonds with government securities. 74. These factors, combined with mixed news regarding the prospects of a normal monsoon suggest to me that this is a particularly inopportune time to reduce the interest rate. In 2-4 months, several uncertainties as posed above are likely to be resolved, helping steer interest rates in a clear direction, upward or downward or simply staying put, depending on how the risks play out. In the meantime, efforts could be made to improve the financial system structurally for better transmission of monetary policy to the real economy, especially as there are headwinds to such transmission from the rise in overall public sector borrowing requirement. 75. On the growth front, signals from the domestic economy are mixed. Capacity utilisation continues to improve which augurs well for future investment, and services growth remains robust; however, consumption demand shows signs of weakness. Global growth is exhibiting a synchronised slowdown; as I have contended in my past statements, mild moderation of global growth benefits India through a downward pressure on oil prices; it is extreme moderation that hurts India and more so through the financial flows channel rather than the trade channel, the latter having been largely insensitive to external prospects in recent years. 76. Aggregate flow of financial resources to the commercial sector remains robust with banks substituting for the weak credit growth of non-banks; bank credit growth continues to be above nominal GDP growth; equity markets have been buoyant; foreign portfolio flows have reversed into India following the dovish stance of advanced country central banks; together, these imply that the finance-neutral output gap, my preferred measure of output gap which accounts for financial cycles, continues to remain closed. 77. On balance, therefore, notwithstanding signs of weakness in growth evinced in high frequency economic indicators, I am inclined to wait for some more time for incoming data to resolve several important uncertainties that will shape the Indian economy in the coming one or two years. The counter-factual exercises suggest that 6.25% policy repo rate is just “right” for achieving headline inflation target of 4% on a durable basis in the medium term; continuing oil price rise or fiscal impulses or seasonal uptick in volatile vegetable prices would likely require some tightening down the road; only a substantial collapse in global growth, which seems unlikely at present given proactive responses of central banks in advanced economies and China, would justify a rate cut at this point. Hence, I am erring on the side of caution, choosing to be patient, rather than supporting another rate cut on the back of MPC’s February decision to cut the rate. Statement by Shri Shaktikanta Das 78. Since the last policy in February 2019, there has been further weakening of domestic growth impulses, with global growth slowdown posing major headwinds to India’s exports. Inflation has continued to surprise on the downside. CPI inflation for January and February averaged 2.3 per cent as against projection of 2.8 per cent for the January-March quarter of 2019 in the February policy. Accordingly, inflation for Q4:2018-19 in all likelihood is set to be lower than that projected in the February policy. 79. CPI inflation excluding food and fuel moderated from 5.6 per cent in December to 5.4 per cent in February. The spike in prices in the health and education sub-groups in December proved to be a one-off phenomenon. The food group continued to be in deflation for the fifth consecutive month in February. Inflation in the fuel and light sub-group unexpectedly collapsed from 4.5 per cent in December to 1.2 per cent in February, with electricity prices remaining in deflation. Inflation expectations of households, measured by the Reserve Bank’s survey of households, declined in the February round over the previous round by 40 basis points each for the three-month ahead and the one-year ahead horizons. With this, inflation expectations have declined cumulatively by as much as 160 basis points for the three-month ahead and 170 basis points for one-year ahead horizons in the last four survey rounds. 80. In comparison with the February policy, CPI inflation projection is now revised downwards by 30-40 basis points to 2.4 per cent in Q4:2018-19, 2.9-3.0 per cent in H1:2019-20 and 3.5-3.8 per cent in H2, with risks broadly balanced. This baseline inflation scenario, however, is subject to several uncertainties, especially from crude oil and food prices. More precisely, the uncertainties/risks include: (i) the highly uncertain outlook for oil prices, which are vulnerable to both upward pressure due to continuing OPEC production cuts, as well as downward pressure due to further slowing down of the global economy; (ii) the risk of an abrupt reversal in vegetable prices, which may get accentuated due to deficient monsoon should there be El Niño conditions; and (iii) inflation excluding food and fuel may soften further from the present levels if the recent slowdown in domestic economic activity intensifies. The fiscal situation at the general government level also needs a careful vigil. Given India’s large dependence on imports of crude oil, stability in international crude oil prices is critical for domestic macroeconomic stability. 81. Moving on to economic activity, high frequency indicators suggest a further loss of pace in growth. Private consumption has been weakening as reflected in deceleration in the growth of passenger car sales and domestic air passenger traffic, weak performance of consumer durables and non-durables, and continuing contraction in non-oil non-gold imports. Investment activity has also decelerated due to contraction in production of capital goods in January and imports of capital goods in February. On the supply side, industrial growth has weakened as reflected in deceleration in the growth of index of industrial production (IIP) for January; the growth of core industries for February remained sluggish. However, capacity utilisation (CU) in the manufacturing sector has improved and is also above the long-term average. In the services sector, sales of commercial vehicles, port freight traffic and international air freight traffic contracted during February. However, indicators of the construction sector, viz., growth in consumption of steel and production of cement, continued to show healthy growth. 82. Overall financing conditions have continued to improve as reflected in the total flow of resources to the commercial sector. However, bank credit flows to micro and small as well as medium industries remain extremely weak. GDP growth for 2019-20 has been revised downwards to 7.2 per cent – in the range of 6.8-7.1 per cent in H1:2019-20 and 7.3-7.4 per cent in H2 – with risks evenly balanced. 83. Investment demand is losing traction and a deceleration in exports may further impact investment activity. With the inflation outlook looking benign and headline inflation expected to remain below target in the current year, it becomes necessary to address the challenges to sustained growth of the Indian economy. Hence, I vote for reducing the policy repo rate by 25 basis points. I would like to state here that there is a need to consider interest rate adjustments, not necessarily in the conventional way of 25 bps or multiples thereof. This idea needs further debate and discussion. Further, with several uncertainties facing the economy, it is appropriate to maintain the neutral stance of monetary policy. 84. The RBI will continue to watch the evolving growth and inflation dynamics and shall act in time and act decisively while ensuring price stability on an enduring basis in pursuance of its mandate under the RBI Act. Yogesh Dayal

Chief General Manager Press Release : 2018-2019/2481

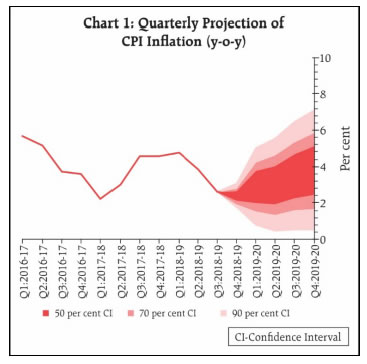

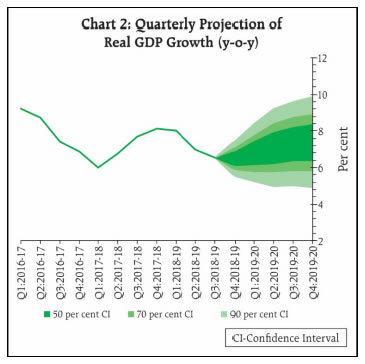

|