On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (February 5, 2021) decided to: - keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent. - The MPC also decided to continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. The global economic recovery slackened in Q4 (October-December) of 2020 relative to Q3 (July-September) as several countries battle second waves of COVID-19 infections, including more virulent strains. With massive vaccination drives underway, risks to the recovery may abate and economic activity is expected to gain momentum in the second half of 2021. In its January 2021 update, the International Monetary Fund (IMF) has revised upward its estimate of global growth in 2020 to (-)3.5 per cent from (-)4.4 per cent and increased the projection of global growth for 2021 by 30 basis points to 5.5 per cent. Barring some emerging market economies, inflation remains benign on weak aggregate demand, although rising commodity prices carry upside risks. Financial markets remain buoyant, supported by easy monetary conditions, abundant liquidity and optimism from the vaccine rollout. Global trade is also expected to rebound in 2021, with services trade on a slower recovery than merchandise trade. Domestic Economy 3. The first advance estimates of GDP for 2020-21 released by the National Statistical Office (NSO) on January 7, 2021 estimated real GDP to contract by 7.7 per cent, in line with the projection of (-)7.5 per cent set out in the December 2020 resolution of the MPC. High frequency indicators – railway freight traffic; toll collection; e-way bills; and steel consumption – suggest that revival of some constituents of the services sector gained traction in Q3 (October-December). The agriculture sector remains resilient - rabi sowing was higher by 2.9 per cent year-on-year (y-o-y) as on January 29, 2021, supported by above normal north-east monsoon rainfall and adequate reservoir level of 61 per cent (as on February 4, 2021) of full capacity, above the 10 years average of 50 per cent. 4. After breaching the upper tolerance threshold of 6 per cent for six consecutive months (June-November 2020), CPI inflation fell to 4.6 per cent in December on the back of easing food prices and favourable base effects. Food inflation collapsed to 3.9 per cent in December after averaging 9.6 per cent during the previous three months (September-November) due to a sharp correction in vegetable prices and softening of cereal prices with kharif harvest arrivals, alongside supply side interventions. On the other hand, core inflation, i.e. CPI inflation excluding food and fuel remained elevated at 5.5 per cent in December with marginal moderation from a month ago. In the January 2021 round of the Reserve Bank’s survey, inflation expectations of households softened further over a three month ahead horizon in tandem with the moderation in food inflation; one year ahead inflation expectations, however, remained unchanged. 5. Systemic liquidity remained in large surplus in December 2020 and January 2021, engendering easy financial conditions. Reserve money rose by 14.5 per cent y-o-y (on January 29, 2021), led by currency demand. Money supply (M3), on the other hand, grew by only 12.5 per cent as on January 15, 2021, but with non-food credit growth of scheduled commercial banks accelerating to 6.4 per cent. Corporate bond issuances at ₹5.8 lakh crore during April-December 2020 were higher than ₹4.6 lakh crore in the same period of last year. India’s foreign exchange reserves were at US$ 590.2 billion on January 29, 2021 – an increase of US$ 112.4 billion over end-March 2020. Outlook 6. With the larger than anticipated deflation in vegetable prices in December bringing down headline closer to the target, it is likely that the food inflation trajectory will shape the near-term outlook. The bumper kharif crop, rising prospects of a good rabi harvest, larger winter arrivals of key vegetables and softer egg and poultry demand on avian flu fears are factors auguring a benign inflation outcome in the months ahead. On the other hand, price pressures may persist in respect of pulses, edible oils, spices and non-alcoholic beverages. The outlook for core inflation is likely to be impacted by further easing in supply chains; however, broad-based escalation in cost-push pressures in services and manufacturing prices due to increase in industrial raw material prices could impart upward pressure. Furthermore, there could be increased pass-through to output prices as demand normalises as indicated in the Reserve Bank’s industrial outlook, services and infrastructure outlook surveys and purchasing managers’ indices (PMIs) and firms regain pricing power. International crude oil prices may remain supported by demand build up on optimism from vaccination and continuing production cuts by OPEC plus. The crude oil futures curve has become downward sloping since December 2020. Taking into consideration all these factors, the projection for CPI inflation has been revised to 5.2 per cent in Q4:2020-21, 5.2 per cent to 5.0 per cent in H1:2021-22 and 4.3 per cent in Q3: 2021-22, with risks broadly balanced (Chart 1). 7. Turning to the growth outlook, rural demand is likely to remain resilient on good prospects of agriculture. Urban demand and demand for contact-intensive services is expected to strengthen with the substantial fall in COVID-19 cases and the spread of vaccination. Consumer confidence is reviving and business expectations of manufacturing, services and infrastructure remain upbeat. The fiscal stimulus under AtmaNirbhar 2.0 and 3.0 schemes of government will likely accelerate public investment, although private investment remains sluggish amidst still low capacity utilisation. The Union Budget 2021-22, with its thrust on sectors such as health and well-being, infrastructure, innovation and research, among others, should help accelerate the growth momentum. Taking these factors into consideration, real GDP growth is projected at 10.5 per cent in 2021-22 – in the range of 26.2 to 8.3 per cent in H1 and 6.0 per cent in Q3 (Chart 2).  8. The MPC notes that the sharp correction in food prices has improved the food price outlook, but some pressures persist, and core inflation remains elevated. Pump prices of petrol and diesel have reached historical highs. An unwinding of taxes on petroleum products by both the centre and the states could ease the cost push pressures. What is needed at this point is to create conditions that result in a durable disinflation. This is contingent also on proactive supply side measures. Growth is recovering, and the outlook has improved significantly with the rollout of the vaccine programme in the country. The Union Budget 2021-22 has introduced several measures to provide an impetus to growth. The projected increase in capital expenditure augurs well for capacity creation thereby improving the prospects for growth and building credibility around the quality of expenditure. The recovery, however, is still to gather firm traction and hence continued policy support is crucial. Taking these developments into consideration, the MPC in its meeting today decided to continue with an accommodative stance of monetary policy till the prospects of a sustained recovery are well secured while closely monitoring the evolving outlook for inflation. 9. All members of the MPC – Dr. Shashanka Bhide; Dr. Ashima Goyal; Prof. Jayanth R. Varma; Dr. Mridul K. Saggar; Dr. Michael Debabrata Patra; and Shri Shaktikanta Das – unanimously voted for keeping the policy repo rate unchanged at 4 per cent. Furthermore, all members of the MPC voted to continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. 10. The minutes of the MPC’s meeting will be published by February 22, 2021. 11. The next meeting of the MPC is scheduled during April 5 to 7, 2021. (Yogesh Dayal)

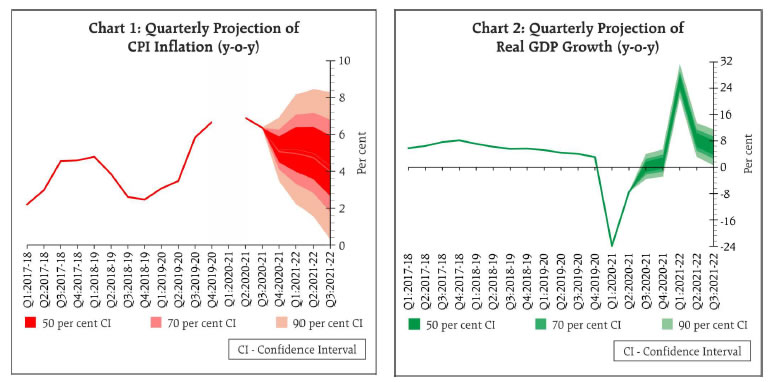

Chief General Manager Press Release: 2020-2021/1050 |