1. Chief guest, Shri M. Damodaran, Dr. Dhingra, Director NIBM, other dignitaries on the dais, distinguished bankers, faculty and staff of the institution, proud parents, and, all graduating students, and of course, friends from media, I thank NIBM for giving me the opportunity to be part of this occasion and share some thoughts when another batch of bank management graduates is passing out. 2. Martin Luther King Jr. once said “Intelligence plus character – that is the goal of true education”. If I can paraphrase what he said in the context of management education, I would say that the true goal of management education is to teach business acumen and professional ethics. When it is a degree from an institute specializing in banking & finance, the emphasis on ethics becomes even greater. The need to do the right thing in the right manner cannot be overemphasized today, given the overhang of large stressed assets that we are dealing with. 3. When the banking regulator speaks to bank management graduates in today’s scenario, it cannot but be on the resolution of stressed assets, because we have to get over with this problem soon, so that our banking system dominated by Public Sector Banks (PSBs) can attain a sustainable growth path in near future. Accordingly, I will explain the recent steps that the Reserve Bank has taken in this direction and as a part of this, I will dwell at some length on the new framework for resolution of stressed assets that we articulated in our circular of February 12, 2018. Stressed Assets 4. The graph below shows the evolution of stressed assets, including Non-Performing Assets (NPAs) of the banking system in India. It is beneficial to look at stressed assets as whole rather than NPAs only, to avoid errors in inter-temporal comparison because an account becomes an NPA only when it is recognized as such. As I had clarified in a speech in August 2016 on the topic Asset Quality of Indian Banks: Way Forward (https://rbi.org.in/scripts/BS_SpeechesView.aspx?Id=1023), this growth in stressed assets was in turn the outcome of rapid credit growth during 2006-2011. During this time, the nominal credit growth was in excess of 20% Y-O-Y and far in excess of the nominal growth in industry.  5. As may be seen from the graph, stressed assets have registered a steady growth since 2011; but if we were to look at NPAs, the growth was muted until 2014 and has been more dramatic, particularly after 2015-16. This is because, the Reserve Bank undertook an Asset Quality Review (AQR) that led to recognition as NPA of several loans, which banks had then considered to be standard assets. Indeed, NPAs went up from 4.62% in 2014-15 to 7.79% in 2015-16, and were as high as 10.41% by December 2017. Asset Quality Review 6. In February 2014, the Reserve Bank issued the framework for resolution of stressed assets. An important part of the framework was the setting up of the Central Repository of Information on Large Credits (CRILC). CRILC captured all exposures of banks above Rs 50 million. The data was accessible not just to the Reserve Bank but also to banks. For the first time we created a supervisory database of this nature, which gave Reserve Bank a comprehensive view of the banking system’s exposure to a large borrower and how the exposure to the same borrower was classified differently by different banks. While our stand has been that asset classification should be based on the record of recovery with individual banks, CRILC gave us the wherewithal to objectively assess whether the divergent classifications were indeed justified. It also gave us a better insight into movement of funds from one bank to the other to keep an account standard. 7. This way, the AQR, backed by CRILC, enabled us to get a banking system-wide view of large bank credits and make a holistic assessment of the true state of health of those exposures. Together, they led to identification of NPAs that had not been recognized as such by the banks and also of accounts that would require to be downgraded over various timelines, if necessary closures such as resolution or account upgrade were not achieved. The resulting recognition of true asset quality at banks largely explains the spurt in NPAs during the last three years. Evolution of Resolution Frameworks in India 8. Before I come to the framework enunciated in the circular of February 12, 2018, it would be good to have a quick look at the resolution frameworks we had in place before. The normal principle for restructuring is that an account should be downgraded if any amount is forborne. The Reserve Bank put in place, in August 2001, the Corporate Debt Restructuring (CDR) mechanism for restructuring of debt without the need for an asset quality downgrade if the restructuring plan met certain conditions. The CDR mechanism worked well initially. In later years, its asset quality forbearance was used more as a tool for avoiding recognition of non-performance of stressed assets and less for their effective resolution. Therefore, in May 2013, we announced the decision to withdraw the forbearance on asset classification effective April 1, 2015. However, in the wake of the mounting NPAs, the Reserve Bank allowed asset classification benefits for certain types of restructuring schemes. These included the Strategic Debt Restructuring (SDR), Flexible Structuring of Project Loans and the Scheme for Sustainable Structuring of Stressed Assets (S4A). Thus, while the principle that a restructuring would call for downgrade of the asset was in place, a window of exception was opened, provided the contours of restructuring met certain conditions. 9. It has been our view that the restructuring schemes were required at a time when we did not have an effective bankruptcy law in place. The schemes essentially created a framework for resolution that should normally happen under the aegis of an insolvency and bankruptcy law. The focal points of the schemes were deep restructuring of stressed assets, change of ownership / management of stressed borrowers, optimal structuring of credit facilities, and haircuts wherever the exposures were economically unviable. 10. In 2016, the Insolvency and Bankruptcy Code, 2016 (IBC), which is a comprehensive bankruptcy code, was enacted and notified. The Code envisages timely resolution of borrower defaults through collective decision making by the creditors. The Code is both process-oriented and time-oriented. It is-process-oriented, in that it lays down, in detail, the various steps that need to be followed once a borrower is admitted for insolvency; and it is time-oriented because it specifies strict timelines for insolvency resolution, failing which the borrower would have to be taken into liquidation. 11. The general approach of bankers to stress in large assets has been one of avoiding the de jure recognition of non-performance of such accounts. This is why we have a history of a large number of cases of failed restructuring as the schemes were used for avoiding a downgrade rather than resolving the asset. Prolonging the true asset quality recognition suited both the bankers and the borrowers. The former could make their books look cleaner than they actually were; the latter could avoid the defaulter tag even while, in fact defaulting. Governor had referred to this in his March 14, 2018 speech (https://www.rbi.org.in/home.aspx) as the borrower-banker nexus, which may not have a pejorative connotation, but implied that the banks indulged in the proverbial act of extending and pretending. It is instructive to mention here that most cases where the SDR scheme was invoked did not result in change of management, implying that the scheme was used only for the asset classification benefit during the standstill period of 18 months. The strike rate in case of S4A was somewhat better, because there were preconditions to the applicability of the scheme and the Overseeing Committee (OC) ensured strict adherence to the framework upfront. However, the total value of such cases in the overall scheme of things was not that significant. 12. The amendments to the Banking Regulation Act, 1949 empowering the Reserve Bank to direct banks to refer specific cases of default for resolution under IBC were a clear indication that an external nudge was required for banks to file insolvency application against large borrowers. As you may be aware, RBI constituted an Internal Advisory Committee (IAC) in 2017 to determine cases to be referred under IBC. Based on its recommendations, a total of 41 accounts were identified for such reference in two tranches. The IAC opined that RBI should evolve a steady-state framework for filing insolvency applications in future, rather than identify cases itself periodically. The New Paradigm 13. The recommendation of the IAC made eminent sense for the following reasons. Firstly, the IBC is a comprehensive and time-bound framework for dealing with corporate stress. Secondly, a clear articulation of policy in this regard will bring certainty to all the stakeholders. Thirdly, a steady-state framework for reference under IBC was the logical outcome of the amendments to the BR Act; it would not have been equitable, if the powers were used for a limited time for a limited number of cases. Finally and more importantly, the IAC recommendation was in consonance with Reserve Bank’s preference all along for an efficient legal framework for insolvency and bankruptcy over regulatorily mandated schemes. 14. It was therefore, decided to go ahead with the recommendation of the IAC. Since a process-oriented Code was enacted in the country which also provided for exploring resolution options before liquidation, another process-oriented regulatory framework for out-of-court resolution of stressed assets was considered redundant. The Reserve Bank decided that rather than having two process-oriented frameworks, it would be beneficial to have two complementary frameworks that seamlessly align with each other - one which provides full flexibility for out-of-court workouts to be explored within a reasonable period after default, failing which, the other, viz., the statutory process under the IBC would kick in. 15. The new framework for resolution of stressed assets outlined in the Reserve Bank’s circular of February 12, 2018 is an outcome of the above philosophy. You would notice that unlike the earlier frameworks, this is more outcome-oriented and leaves considerable flexibility to banks to determine the process as well as the contours of the restructuring plan. The revised framework removes various process and input constraints which were embedded in the earlier regulatory schemes for restructuring. Instead it provides as much flexibility as possible to lenders and the stressed borrowers so long as a credible resolution plan is implemented within a specified timeframe. If lenders and the stressed borrowers are unable to put in place a credible resolution plan within the timelines, then the structured insolvency resolution process under the IBC should take over. 16. Let me highlight some other noteworthy features. The revised framework tries to reduce the arbitrage the borrowers are currently enjoying while raising funds through borrowing from banks vis-à-vis raising funds from the capital markets. If a borrower delays coupon/principal payment on a corporate bond even for one day, the market would penalize the borrower heavily – the rating would be downgraded, the yields on the bonds would shoot up, cost of further financing would increase, suits would be filed by investors, etc., to name a few. So far, defaults in bank borrowings have not attracted similar reactions. Only when the overdues stretch beyond 90 days, the loans would be classified as non-performing assets; hence, efforts by lenders and borrowers have been to avoid the account having to be de jure classified as NPA, notwithstanding the de facto status. What this means is that debt contract embedded in bank loans in India has been continuously losing its sanctity, especially where the borrowing is large. There is a need to change this and restore the sanctity of the debt contract, lest bank debt becomes subordinate even to equity. The new framework is precisely aimed at doing this. Prompt repayment to banks is critical because they access unlimited uncollateralized funding from among others, the common persons, on the strength of the banking licence. 17. What the revised framework also does is to enjoin upon the banks as creditors to enforce their contracts or renegotiate their contracts with their borrowers so that they are not in default in the first place. Where the contracts are renegotiated, banks books should reflect this through asset classification and provisioning. This is why the framework requires banks to report even one day default and draw up resolution plans thereupon such that the borrower is not in default as on 180th day from the date of such default. You would have noted that while it is mandatory to report defaults on a weekly basis, the classification of loans as non-performing assets will still be on the 90-day-past-due criterion. As such, the idea is to nudge lenders and borrowers to take timely corrective action so that the deterioration in the asset quality is avoided to the extent possible. At the same time, with defaults being reported to a central database, which is accessible to all banks, the credit discipline is expected to further improve. 18. There has been some commentary on the sufficiency of timelines provided for implementation of the resolution plan under the revised framework. The new framework requires lenders to put in place a resolution plan within 180 days of default and some have commented that 180 days is insufficient to put in place a resolution plan, especially where multiple lenders are involved. However, one has to note that ‘default’ in payment is a lagging, not leading, indicator of financial stress of a borrower and the framework provides 180 days after a default to put in place a resolution plan. Lenders need to be proactive in monitoring their borrowers and be able to identify financial stress using a combination of leading indicators and renegotiation points in the form of loan covenants rather than wait for a borrower to default. Such early identification of stress and loan modifications in response would provide sufficient time for lenders to put in place the required resolution plan. 19. Another major change that has been introduced under the revised framework is that resolution plans can now be implemented individually or jointly by lenders. Previously, the lenders had to form a Joint Lenders Forum (JLF) wherein a decision taken by the majority of lenders was to be binding on the minority lenders. Of course, the latter had an option to exit the JLF. In the revised framework, the Reserve Bank has withdrawn the instructions on the JLF. Complete discretion and flexibility has been given to banks to formulate their own ground rules in dealing with borrowers who have exposures with multiple banks. In the earlier regime, the resolution plan was mostly the same across banks. Under the revised framework, the lenders can implement resolution plans that are tailored to their internal policies and risk appetites. Therefore, unlike the perception in some quarters, the new framework does not seek unanimity. However, if at the end of the 180 days of first default, the borrower is in default to a bank, that bank is mandated to refer the case under IBC. So what the regulations require is that the borrower should not be in default- under the existing contract if there is no restructuring, and under the restructured repayment schedule if there is a restructuring. So let me be crystal clear: there is a chatter that the new framework mandates unanimity across lenders but the fact of the matter is the exact opposite. We are not mandating anything on this aspect. In fact, the guiding principle of the framework is to impose as few mandatory prescriptions on the process as possible. 20. As I have emphasized, the revised framework relies more on outcome check rather than process check. The lenders have complete freedom to decide on the contours of the resolution plan. However, the credibility of the resolution plan is sought to be ensured through the requirement of independent credit evaluation by credit rating agencies. To ensure greater credibility of the rating opinion, contrary to the “issuer pays” model of credit rating, the new framework prescribes “user pays” model for credit opinions – user here being the banks. For credit rating agencies, the incentive to not give erroneous or questionable credit opinion is the credibility and reputation of the agency in the market, which is its main currency for sustained business. Going forward, we will put in place necessary evaluation standards for assessing the performance of rating agencies on this score. 21. Some concerns have been expressed that the 1-day default clause is onerous. These concerns are not well founded. Let me tell you why. For cash credit account, the 30-day trigger has been retained. For term loans, where the repayment schedules are predetermined, borrowers need to and indeed have enough notice to arrange funds in time. It is a behaviour change in repayment of credit that has to come about. I must say here, on the basis of first few reports received from banks under the new reporting system, that non-payment on due date appears to be seen as par for the course by the banks and the borrowers. The data shows that a large number of borrowers, even some highly rated ones, have failed on the 1-day default norm. This has got to change. If borrowers fail to pay on the due date because of a cash flow problem, banks should see that as an early warning indicator warranting immediate action. If borrowers, with ability to pay on the due date, delay it routinely or because they see other arbitrage options, that must change too. Bankers should warn their customers that 1-day default will lead to their being on watch for resolution. Borrowers too should realise that they have to meet payment obligations as per the contract and it is no more sufficient to pay up only by 60/90 days past due date. 22. This brings me to the next commentary on the revised framework. One of the general refrains is that there are delays in payment by buyers including, rather predominantly, government bodies and that it could lead to a significant increase in slippages. First, the repayment schedules of loans should take into account such idiosyncratic risks and accordingly be customized to suit the cash flow pattern of the borrowers. Second, there must be enough skin in the game from the borrower so that there are adequate buffers (debt service reserve accounts) to tide over temporary cash flow volatility. The present problem is that banks allow excessively high leverage thus leaving out any possibility that the borrower can be made to deal with emergencies. This has been possible in an environment in which both the lender and the borrower were not too keen to maintain the sanctity of the debt contract. Such poor credit culture must be incentivized to change and the revised framework is aimed to precisely achieve this objective. I want to mention here that for the small borrower who may not have the wherewithal to bring funds swiftly in the event of non-payment by clients, the framework makes an exception. The framework for restructuring has been consciously made non-applicable to the Micro, Small and Medium Enterprises (MSMEs) with borrowings of Rs 250 million and less. We have left their resolution framework unchanged from what was outlined for them in March 2016. 23. One of the features notices in the past was evergreening of loans to avoid the recognition of non-performance. At the same time, it is necessary to distinguish evergreening from grant of additional finance for meeting genuine business needs. The revised framework requires grant of additional credit facilities to a firm in financial difficulty to be treated as a case of restructuring and lists out the criteria for determining whether or not the borrower is in financial difficulty. Some have expressed the view that the criteria are too broad. The banks, through policies approved by their boards, should fix the parameters and ensure strict adherence thereto. We would expect boards to be reasonable in setting the parameters and will not accept case specific exceptions. 24. Some question the timing of the February 12th circular. I would say certain changes are sooner brought in than later. The search for that perfect time for a long overdue reform can become a never ending exercise. I am not sure whether the protagonists of the view that the reform was untimely know when the right time is other than that it is some time in future!. Having said that, I would want to point out that the Sixth Bi-monthly Monetary Policy Statement, 2017-18 observed that there are early signs in the economy of a revival in investment activity as reflected in improving credit off take, large resource mobilisation from the primary capital market, and improving capital goods production and imports. Further, the process of recapitalisation of PSBs has got underway, which has enhanced their ability to provide for credit losses as well as, in case of better capitalized banks, to contribute to the credit growth. The Reserve Bank has directed banks to file insolvency applications against large distressed borrowers as mentioned earlier, and these accounts are getting resolved under the IBC. All these steps should improve credit flows further and create demand for fresh investment, which may further accelerate growth. The Reserve Bank believes that a focused framework for resolution of distressed borrowers which respects and enforces the sanctity of the debt contract is required to make sure that the excesses observed during the last credit cycle are not repeated and we don’t end up in a similar situation few years down the line. 25. There is also an important equity perspective to the revised framework. As successive Financial Stability Reports of the Reserve Bank have pointed out, the proportion of stressed assets in the larger advances is higher than the share of larger advances in the total advances (see chart below). If the stress in larger advances is not handled in a manner such that both probability of default and loss given default are contained, the resultant low risk-adjusted return on bank assets may have to be compensated in the form of higher borrowing rates for the smaller borrowers. Alternatively, it may mean a low return on bank equity, which may have externalities through the fiscal channel given the principal shareholder of many stressed banks is the government.  There is another issue from the equity perspective. One must understand that smaller firms and new entrants, which create dynamism and enterprise within sectors of the economy, get unfairly competed out when large borrowers are routinely able to obtain soft landing even upon defaults and under-performance. 26. Finally, you may be knowing that banks are required to keep provisions for loans on their books, to cover for future expected losses. This means that as the likelihood of income or recovery from a loan decreases, the amount to be kept as provisions by the banks should increase. If the resulting drain on bank profits has to be contained, the action to address stressed assets should commence no sooner than the emergence of early signs of stress. Thus, bankers should be alive to the increase in risk as the probability of default increases and take adequate measures to contain the loss given default, such as through loan covenants, increased collateral, and/or higher risk premium, with promptitude. If such measures are not undertaken in time, it becomes too late to do anything outside of bankruptcy proceedings. The following table and graph provide enough evidence to suggest that quicker action by banks while the borrowing business is still a going concern results in much lower loan loss. It is instructive to note that the resolution regime has a bearing on the ease of doing business ranking of a country and the new framework alongwith the IBC will be an important step in improving the ranking. | Economy | Resolving Insolvency rank | Recovery rate (%) | Time (years) for resolution | Cost (% of estate) of resolution | Outcome (0 as piecemeal sale and 1 as going concern) | | Norway | 6 | 93.1 | 0.9 | 1 | 1 | | Japan | 1 | 92.4 | 0.6 | 4.2 | 1 | | Singapore | 27 | 88.7 | 0.8 | 4 | 1 | | Hong Kong SAR, China | 43 | 87.2 | 0.8 | 5 | 1 | | United Kingdom | 14 | 85.2 | 1 | 6 | 1 | | Korea, Rep. | 5 | 84.7 | 1.5 | 3.5 | 1 | | United States | 3 | 82.1 | 1 | 10 | 1 | | Germany | 4 | 80.6 | 1.2 | 8 | 1 | | Russian Federation | 54 | 40.7 | 2 | 9 | 0 | | China | 56 | 36.9 | 1.7 | 22 | 0 | | South Africa | 55 | 34.4 | 2 | 18 | 0 | | India | 103 | 26.4 | 4.3 | 9 | 0 | | Source: http://www.doingbusiness.org/data/exploretopics/resolving-insolvency |

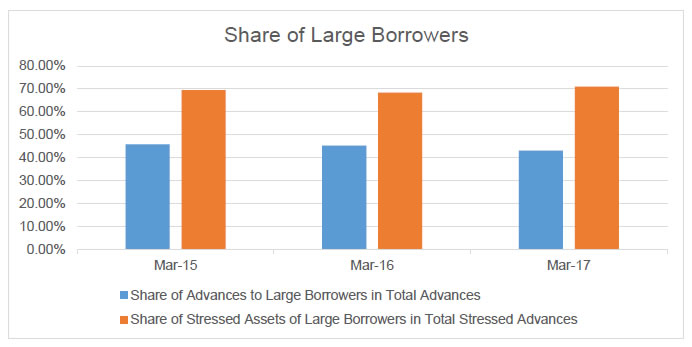

In fact, such timely intervention should be second nature to a bank. Similarly, paying dues on time should be the natural behavior expected from a borrower. The revised framework seeks to inculcate such a behaviour in both lenders and borrowers so as to create a credit culture that is conducive to a safe and sound banking system and a vibrant business environment. 27. Let me then summarise my comments on the revised framework of February 12, 2018: (a) The new framework brings our regulatory framework for stressed assets on par with international norms shorn of all forbearances. (b) It has been made possible because the IBC provides a time-bound legal framework for dealing with debt resolution if the lenders cannot sew up a resolution quickly. (c) Not putting this framework in place would be tantamount to letting go waste the landmark economic legislation that IBC is. (d) The framework undoes many intrusive regulations by specifying outcomes rather than processes. (e) Finally, the framework seeks a fundamental change, for the better, in behaviour of lenders and borrowers, for it can’t be business as usual. 28. Before I sign off, let me throw in one more word of caution. There appears to be taking hold a herd movement among bankers to grow retail credit and the personal loan segment. This is not a risk-free segment and banks should not see it as the grand panacea for their problem riddled corporate loan book. There are risks here too that should be properly assessed, priced and mitigated. 29. I hope that the new tools and lessons that you have learnt as NIBM students, will help us build a strong and resilient banking system in which banks and borrowers understand the new restructuring and resolution paradigm, appreciate it, assimilate it, and live by it. Let me conclude by extending my heartiest congratulations once again to all the graduates on successfully completing the prestigious Post-Graduate Programme in Banking and Finance. These are challenging but exciting times and as you stand on the threshold of a new or renewed career in banking and finance, I trust you will continue to cherish dreams of youth, and among other things, endeavor to build a strong credit culture wherever you go and thereby make a success of the new paradigm that I have outlined. I thank you all for your kind attention. |