On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (April 8, 2022) decided to: • keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent. The marginal standing facility (MSF) rate and the Bank Rate remain unchanged at 4.25 per cent. The standing deposit facility (SDF) rate, which will now be the floor of the LAF corridor, will be at 3.75 per cent. • The MPC also decided to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below Assessment Global Economy 2. Since the MPC’s meeting in February 2022, the global economic and financial environment has worsened with the escalation of geopolitical conflict and accompanying sanctions. Commodity prices have shot up substantially across the board amidst heightened volatility, with adverse fallouts on net commodity importers. Financial markets have exhibited increased volatility. Crude oil prices jumped to 14-year high in early March; despite some correction, they remain volatile at elevated levels. Supply chain pressures, which were set to ease, are rising again. The broad-based jump in global commodity prices has exacerbated inflationary pressures across advanced economies (AEs) and emerging market economies (EMEs) alike causing a sharp revision in their inflation projections. The global composite purchasing managers’ index (PMI) eased to 52.7 in March from 53.5 in February with output growth slowing in both manufacturing and services sectors. World merchandise trade momentum has weakened. 3. Several central banks, especially systemic ones, continue to be on the path of normalisation and tightening of monetary policy stances. Resultantly, sovereign bond yields in major AEs have been hardening. Bullion prices had buoyed to near 2020 highs on safe haven flows, with some recent correction as bond yields rose. Global equity markets fell, although more recently they have recovered some ground. In recent weeks, strong capital outflows from the EMEs have moderated thus curbing the downward pressures on their currencies, even as the US dollar has strengthened. Overall, the global economy faces major headwinds from several fronts, including continuing uncertainty about the pandemic’s trajectory. Domestic Economy 4. The second advance estimates (SAE) for 2021-22 released by the National Statistical Office (NSO) on February 28, 2022 placed India’s real gross domestic product (GDP) growth at 8.9 per cent, 1.8 per cent above the pre-pandemic (2019-20) level. On the supply side, real gross value added (GVA) rose by 8.3 per cent in 2021-22, with its major components, including services, exceeding pre-pandemic levels. GDP growth in Q3:2021-22 decelerated to 5.4 per cent. 5.In Q4:2021-22, available high frequency indicators exhibit signs of recovery with the fast ebbing of the third wave but the picture is mixed. Urban demand reflected in domestic air traffic rebounded in March and the pace of contraction in passenger vehicle sales moderated in February. On the other hand, rural demand mirrored in two-wheeler and tractor sales contracted in February. Import of capital goods increased robustly in February, although domestic production continued to contract. Merchandise exports remained buoyant and clocked double-digit growth for the thirteenth successive month in March 2022 and reached US$ 417.8 billion in 2021-22 surpassing the target of US$ 400 billion. All categories of imports, however, have risen even faster, leading to merchandise trade deficit at a record annual level of US $ 192 billion in 2021-22 or 6.1 per cent of GDP. 6.On the supply side, foodgrains production touched a new record in 2021-22, with both kharif and rabi output crossing the final estimates for 2020-21 as well as the targets set for 2021-22. The manufacturing PMI remained in expansion zone in March, although it moderated somewhat to 54.0 from 54.9 in February. Services sector indicators – railway freight; e-way bills; GST collections; toll collections; fuel consumption; and electricity demand – were in expansion in February-March. The services PMI continued in expansion mode, inching up to 53.6 in March from 51.8 in the preceding month. 7. Headline CPI inflation edged up to 6.0 per cent in January 2022 and 6.1 per cent in February, breaching the upper tolerance threshold. Pick-up in food inflation contributed the most in headline inflation, with inflation of cereals, vegetables, spices and protein-based food items like eggs, meat and fish being the key drivers. Fuel inflation moderated on continuing deflation in electricity and steady LPG prices. Core inflation, i.e., CPI inflation excluding food and fuel remained elevated, though there was some moderation from 6.0 per cent in January to 5.8 per cent in February primarily due to the easing of inflation in transport and communication; pan, tobacco and intoxicants; recreation and amusement; and health. 8. Overall system liquidity remained in large surplus, with average daily absorption (through both the fixed and variable rate reverse repos) under the LAF at ₹7.5 lakh crore in March, marginally lower than ₹7.8 lakh crore in January-February 2022. Reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 10.9 per cent (y-o-y) on April 1, 2022. Money supply (M3) and bank credit by commercial banks rose (y-o-y) by 8.7 per cent and 9.6 per cent, respectively, as on March 25, 2022. India’s foreign exchange reserves increased by US$ 30.3 billion to US$ 607.3 billion in 2021-22. Outlook 9. Looking ahead, the inflation trajectory will depend critically upon the evolving geopolitical situation and its impact on global commodity prices and logistics. On food prices, domestic prices of cereals have registered increases in sympathy with international prices, though record foodgrains production and buffer stock levels should prevent a major flare up in domestic prices. Elevated global price pressures in key food items such as edible oils, and in animal and poultry feed due to global supply shortages impart high uncertainty to the food price outlook, warranting continuous monitoring. 10. In this scenario, pro-active supply management is critical to contain inflation. International crude oil prices remain volatile and elevated, with considerable uncertainties surrounding global supplies. With the broad-based surge in prices of key industrial inputs and global supply chain disruptions, input cost push pressures appear likely to persist for longer than expected earlier. Their pass-through to retail prices, though limited till now given the continuing slack in the economy, needs to be monitored carefully. Manufacturing sector firms polled in the Reserve Bank’s industrial outlook survey expect higher input and output price pressures going forward. Taking into account these factors and on the assumption of a normal monsoon in 2022 and average crude oil price (Indian basket) of US$ 100 per barrel, inflation is now projected at 5.7 per cent in 2022-23, with Q1 at 6.3 per cent; Q2 at 5.8 per cent; Q3 at 5.4 per cent; and Q4 at 5.1 per cent (Chart 1).  11. Going forward, good prospects of rabi output augur well for rural demand. With the ebbing of the third wave and expanding vaccination coverage, the pick-up in contact-intensive services and urban demand is expected to be sustained. The government’s thrust on capital expenditure coupled with initiatives such as the production linked incentive (PLI) scheme should bolster private investment activity, amidst improving capacity utilisation, deleveraged corporate balance sheets, higher offtake of bank credit and congenial financial conditions. At the same time, the escalation of the geopolitical situation and the accompanying surge in international crude oil and other commodity prices, tightening of global financial conditions, persistence of supply-side disruptions and significantly weaker external demand pose downside risks to the outlook. The future course of the pandemic and the uncertainties about the pace of monetary policy normalisation in major advanced economies also weigh on the outlook. Taking all these factors into consideration, the real GDP growth for 2022-23 is now projected at 7.2 per cent, with Q1 at 16.2 per cent; Q2 at 6.2 per cent; Q3 at 4.1 per cent; and Q4 at 4.0 per cent, with risks broadly balanced (Chart 2).  12.The MPC is of the view that since the February meeting, the ratcheting up of geopolitical tensions, generalised hardening of global commodity prices, the likelihood of prolonged supply chain disruptions, dislocations in trade and capital flows, divergent monetary policy responses and volatility in global financial markets are imparting sizeable upside risks to the inflation trajectory and downside risks to domestic growth. 13. Given the evolving risks and uncertainties, the MPC has decided to keep the policy repo rate unchanged at 4 per cent. The MPC also decided to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 14. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate at 4.0 per cent. 15. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das unanimously voted to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 16. The minutes of the MPC’s meeting will be published on April 22, 2022. 17. The next meeting of the MPC is scheduled during June 6-8, 2022.

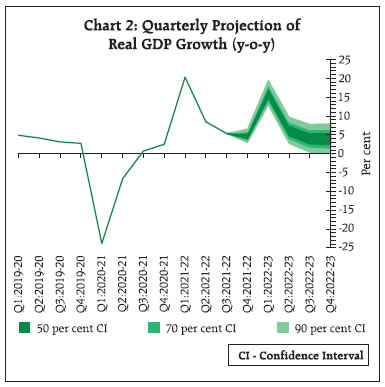

|