Global regulatory initiatives are increasingly concentrated on fortifying the resilience of the financial system against new and emerging sources of risk. Concurrently, efforts continue to focus on reinforcing the resilience of both bank and non-bank financial intermediaries. Domestically, the regulatory endeavor has emphasised enhancing the soundness and resilience of the financial sector, fostering the development of deeper and more sophisticated financial markets and implementing global best practices while keeping in view country-specific circumstances. Introduction 3.1 As the global economy navigates heightened uncertainty, policymakers have maintained the focus on enhancing the resilience of the financial system and consolidating the improvements in regulation and supervision. Global regulatory efforts are also prioritising the mitigation of risks arising from climate change, leveraging advancements in financial technology and dealing with cyber threats, reinforcing the resilience of both traditional banking institutions and non-bank financial intermediaries. 3.2 Against this backdrop, this chapter reviews recent regulatory initiatives undertaken globally and in India to improve the resilience and efficiency of the financial system. III.1 Global Regulatory Initiatives III.1.1 Markets and Financial Stability 3.3 In its study1 of vulnerabilities in short-term funding markets, the Financial Stability Board (FSB) has presented an analytical framework aimed at evaluating potential market reforms in Commercial Paper (CP) and Certificate of Deposit (CD) markets. It advocates exploring structural modifications in these markets to complement investor-focused reforms such as the resilience of key investors like money market funds (MMFs). The proposed reforms encompass improvements in market microstructure, enhancement of regulatory reporting and public disclosures and the expansion of private repo markets for CP and CD collateral. Adjustments to market microstructure may involve digitisation, adoption of shorter settlement conventions and streamlining of ISIN2 generation processes, although requirements in this regard may vary considerably across jurisdictions. Strengthened regulatory reporting and enhanced public disclosure within CP and CD markets could facilitate improved monitoring by regulatory authorities and potentially foster greater market participation by providing more detailed market information to investors. 3.4 The FSB has also issued revised policy recommendations3 for enhancement of liquidity management practices of open-ended fund (OEF) managers beyond current standards. The recommendations emphasise: (a) the need for clearer guidance on the redemption terms that OEFs could offer to investors, aligning them with the liquidity profile of their asset holdings; (b) the importance of ensuring the availability of a diverse range of anti-dilution and quantity-based liquidity management tools (LMT) for use by OEF managers under both normal and stressed market conditions; and (c) increased utilisation and consistency in the use of anti-dilution LMTs across normal and stressed market conditions. The International Organisation of Securities Commissions (IOSCO) plans to operationalise the revised FSB recommendations and monitor progress in implementation in collaboration with the FSB. 3.5 In April 20244, the FSB introduced new global standards to support orderly resolution of central counterparties (CCPs) which aims to ensure that resolution authorities have ready access to a set of specific financial resources and tools as well as any unused recovery resources to support orderly resolution of a CCP. The objective is to ensure that adequate liquidity, loss absorbing and recapitalisation resources and financial tools are available to maintain continuity of a CCP’s critical functions. 3.6 In view of financial institutions’ rising dependencies on third party service providers in supporting critical shared services, in March 20245, the FSB has specified how authorities and firms should approach each of the operational continuity factors (viz, legal, contractual and governance frameworks, resourcing, management information systems and financial resources) for digital services as a supplementary note to the earlier document on ‘Guidance on Arrangements to Support Operational Continuity in Resolution (2016)’. III.1.2 FinTech and Financial Stability 3.7 Widespread adoption of digitalisation has spurred innovation and has led to the emergence of new business models alongside increased dependency of traditional financial players on third party technology providers as many financial services get increasingly provided through new distribution channels. The application of distributed ledger technology (DLT), application programming interfaces (API), cloud computing, artificial intelligence (AI) and machine learning (ML) in finance - broadly referred to as ‘fintech’ - has pertinent implications for financial intermediation process as well as for banks and regulators. The report6 of the Basel Committee on Banking Supervision (BCBS) on the implications of digitalisation of finance for banks and supervisors covers three broad areas, viz., (a) stocking of ‘fintech’ penetration in the banking sector; (b) benefits and risks of new technologies and their suppliers on the financial services provided by banks; and (c) policy recommendations to mitigate potential risks. The report states that while cloud computing has been widely adopted, banks appear to be using AI/ML technologies cautiously, especially for customer-facing services and for revenue generation. 3.8 The report notes that digitalisation has created new sources of vulnerabilities while amplifying existing risks to banks, their customers and to financial stability. Banks are facing ‘strategic risk’ as they need to adapt their business strategies to an increasingly digital environment in which higher dependence on third parties and automated processes has heightened ‘reputational risk’ and ‘operational risk’. Denser interconnectivity among financial entities poses broader financial stability risks such as higher contagion and amplification of procyclical behaviour in times of stress. The regulatory and supervisory implications for banks and supervisors include: (a) effective monitoring of evolving risks and adopting a responsible approach to innovation; (b) safeguarding data and implementing robust risk management processes; and (c) building technological expertise to assess and mitigate risks from new technologies and business models. 3.9 Global regulatory bodies and multilateral organisations such as the Financial Action Task Force (FATF) and the IOSCO have been examining developments in the field of Decentralised Finance7 (DeFi), prompted by concerns that rapid growth in such segments could have implications for broader asset market and global financial stability. To create a regulatory framework for digital assets, the United States is considering the ‘Financial Innovation and Technology for the 21st Century Act (FIT21)’, which is intended to provide market certainty, grant legal recognition to digital assets and allocate jurisdiction to Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) over involved assets, venues and entities. Meanwhile, the SEC approved the trading of exchange traded products (ETP), based on select cryptocurrencies, to create a level playing field for such ETP issuers and ensure customer protection. III.1.3 Banking and Financial Stability 3.10 The BCBS implemented revisions8 to the Basel ‘Core Principles’9, drawing on supervisory insights and structural changes to the global banking system since the previous review in 2012. The review was intended to improve drafting consistency among various ‘Core Principles’ and ensure better alignment with the Basel Framework. The modifications, inter alia, cover: (a) assessment of financial risks; (b) corporate governance and risk management guidelines; and (c) supervisory powers and responsibilities. The revised ‘Core Principles’ introduce the definition of ‘climate-related financial risks’ and adjustments to the requirements for scenario analysis and stress testing to facilitate a more flexible and proportionate application by supervisors. 3.11 The BCBS’s consultative document10 on the revised assessment framework for global systemically important banks (G-SIBs) is aimed at discouraging window-dressing behaviour. BCBS found that the G-SIB framework is sensitive to the year-end values of the indicators reported by banks, which are prone to manipulation. The resultant mismeasurement of a bank’s systemic importance in the G-SIB methodology has implications for financial sector resilience and resource efficiency as well as broader unintended consequences for both financial stability and monetary policy. The document details potential measures to address the relevant shortcomings in the framework, including calculating G-SIB scores based on average values over the reporting year, rather than year-end values. III.1.4 Climate Finance and Financial Stability 3.12 The IOSCO published a report11 outlining current global best practices to address greenwashing12 and the associated challenges faced by supervisors, including data gaps, lack of transparency and reliability of environmental, social, and governance (ESG) ratings, inconsistency in labelling and product classification. The report covers the key elements of the existing supervisory tools and educational measures used by regulators to prevent and address greenwashing. It also specifies the enforcement measures and cross-border cooperation mechanisms which play a key role in addressing sustainability risks at a global level. 3.13 The International Sustainability Standards Board (ISSB), an independent standard-setting body of the International Financial Reporting Standards (IFRS) foundation, published the digital sustainability taxonomy (ISSB taxonomy)13 to help investors analyse sustainability disclosures efficiently. Use of the ISSB taxonomy by companies will enable investors to search, extract and compare the disclosures done as per IFRS S1 and IFRS S2– the sustainability-related financial disclosures for capital markets. 3.14 The European Systemic Risk Board (ESRB) published a report14 focussing on how financial information contained in IFRS disclosures can reflect climate-related risks from a financial stability perspective. It also suggests that additional work on the accounting treatment of carbon pricing mechanism should be prioritised. 3.15 The BCBS discussion paper15 on how climate scenario analysis (CSA), aimed at strengthening the management and supervision of climate-related financial risks, can help banks assess the impact of climate related risks on their overall risk profile and gauge resilience of their business models to climate risks. It, however, acknowledges the limitations of lack of data and variation in assessment methodologies used by jurisdictions in achieving the intended objectives. 3.16 The Network for Greening the Financial System (NGFS) published a cover note16 and three reports on climate transition plans which, inter alia, give recommendations on designing transition plans and assessments of how they can improve risk management frameworks of financial institutions. The NGFS also published a cover report17 and two technical documents on ‘sustainable and responsible investment (SRI) in central banks’ portfolio management’ which make several recommendations on SRI policies and refine central banks’ investment practices, including incorporating climate change analyses into their investment policies. 3.17 The Bank for International Settlements (BIS) Innovation Hub Eurosystem Centre has developed a generative artificial intelligence (AI) tool to help measure climate risks in the financial system through its initiative ‘Project Gaia’18. The tool is aimed at using AI to search corporates’ climate-related disclosures and extract related data such as carbon emissions and green bond issuances. The tool has been designed with inbuilt flexibility to adapt to broader use by central banks and the financial sector. III.1.5 Cyber Security and Financial Stability 3.18 Cybersecurity is an integral element of ensuring financial stability in an ever-changing and interconnected world in which cross-border coordination has become paramount. The G719 Cyber Expert Group consistently engages in exercises to ensure members’ capability to effectively coordinate and communicate responses in the event of a significant cross-border cyber incident affecting the financial system. The group completed one such exercise20 in April 2024 under the hypothetical scenario of a large-scale cyberattack on financial market infrastructures and entities in all G7 jurisdictions. 3.19 As part of its macroprudential strategy to advance system-wide cyber resilience, the ESRB published a report21 reviewing the operational policy tools used to address systemic cyber crises with focus on three aspects: (a) tools for gathering, sharing and managing information about cyber incidents; (b) coordination tools to ensure an effective joint response by financial institutions and authorities; and (c) emergency and backup systems. III.2 Domestic Regulatory Initiatives 3.20 During the period under review, financial regulators undertook several initiatives to improve the resilience of the Indian financial system (major measures are listed in Annex 3). III.2.1 Operational Risk Management and Operational Resilience 3.21 To align domestic regulatory guidance with global best practices on operational resilience including the BCBS principles, a ‘Guidance Note on Operational Risk Management and Operational Resilience’ was issued by the Reserve Bank. The Note has adopted a principle-based and proportionate approach to ensure smooth implementation across REs of various sizes, nature, complexity, geographic location and risk profile of their businesses. It provides overarching guidance to REs to strengthen their operational risk management framework and also enhances their operational resilience to deliver critical operations even through disruption. It has been built on the three pillars: (a) prepare and protect22; (b) build resilience23 and (c) learn and adapt24, together consisting of 17 principles. III.2.2 Voluntary transition of Small Finance Banks to Universal Banks 3.22 The guidelines for ‘on-tap’ licensing of small finance banks (SFBs) provided for a transition path for SFBs to convert into universal banks. With the objective to bring better clarity, the following eligibility criteria have been stipulated for an SFB to transition into a universal bank: (i) scheduled status with a satisfactory track record of performance for a minimum period of five years; (ii) listing of bank’s shares on a recognised stock exchange; (iii) minimum net worth of ₹1,000 crore as at the end of the previous quarter (audited); (iv) meeting the prescribed CRAR requirements for SFBs; (v) net profit in the last two financial years; and (vi) GNPA and NNPA of less than or equal to three per cent and one per cent, respectively, in the last two financial years. III.2.3 Reserve Bank of India (Government Securities Lending) Directions 3.23 In order to add depth and liquidity to the Government securities market and aid efficient price discovery, the Reserve Bank permitted lending and borrowing of Government securities, which will augment the existing market for ‘special repos’25. These Directions are applicable to all Government securities lending transactions undertaken in over-the-counter (OTC) markets. Government securities (excluding Treasury Bills) issued by the Central Government are eligible for lending/borrowing under a Government Securities Lending (GSL) transaction26. Government securities issued by the Central Government (including Treasury Bills) and the State Governments are eligible as collateral under a GSL transaction. 3.24 An entity eligible to undertake repo transactions in Government securities in terms of the Repurchase Transactions (Repo) (Reserve Bank) Directions, 2018, as amended from time to time, is eligible to participate in GSL transactions as lender of securities. Entities that are eligible to undertake short sale transactions in terms of Short Sale (Reserve Bank) Directions, 2018, as amended from time to time, are eligible to borrow securities under a GSL transaction. The system is expected to facilitate wider participation in the securities lending market by providing investors an avenue to deploy idle securities and enhance portfolio returns. III.2.4 Margining for Non-Centrally Cleared OTC Derivatives 3.25 In order to improve safety of settlement of OTC derivatives that are not centrally cleared and following G-20 recommendations, the Reserve Bank issued Master Directions on margining for non-centrally cleared OTC derivatives to implement global practices. Margins for non-centrally cleared derivatives (NCCDs) are expected to reduce contagion and spillover effects by ensuring that collateral is available to offset any default losses. Margin requirements can also have broader macroprudential benefits by reducing the financial system’s vulnerability to potentially destabilising procyclicality and limiting the build-up of uncollateralised exposures within the financial system. 3.26 All financial firms that engage in NCCDs must exchange initial margin (IM) and variation margin (VM), while non-financial entities that engage in NCCDs must exchange VM, to mitigate counterparty risks posed by such transactions, as appropriate. A ‘covered entity’27 is required to exchange IM and VM with other covered entities for NCCD transactions only. VM shall be exchanged on an aggregate net basis across all NCCD contracts that are executed under a single, legally enforceable netting agreement. The initial margin is to be exchanged on a gross basis without any netting of initial margin amounts owed by the two counterparties across all NCCD contracts that are executed under a single, legally enforceable netting agreement. Eligibility criteria for qualifying assets to be collected as collateral for IM and VM purposes have been specified along with the prescribed risk-sensitive haircut to be applied. III.2.5 Investments in Alternative Investment Funds (AIFs) 3.27 In view of certain regulatory concerns regarding the use of Alternative Investment Funds (AIFs) by regulated entities (REs), for evergreening stressed loans, a circular on ‘Investment in Alternative Investment Funds’ was issued in 2023 prohibiting REs from investing in any AIF scheme with direct or indirect downstream investments in a debtor company of the RE. REs were directed to divest such investments within 30 days, failing which they must make full provisions for them. Additionally, investments by REs in ‘subordinated units’ of any AIF scheme with a ‘priority distribution model’ shall be subject to full deduction from the RE’s capital funds. 3.28 In this regard, in order to ensure an effective and consistent implementation of the said circular across REs, a follow-up clarificatory circular was issued, providing the following clarifications/ directives: (i) downstream investments exclude equity shares but include all other investments, including hybrid investments; (ii) provisioning shall be required only to extent of RE’s investment in the AIF scheme which is further invested by the AIF in the debtor company and not the entire investment in AIF scheme; (iii) proposed deductions from capital shall take place equally from both Tier-1 and Tier-2 capital, encompassing all forms of subordinated exposures including investment in nature of sponsor units; (iv) compliance with paragraph 328 of the said circular, regarding full capital deduction for investment by REs in junior/subordinated tranche of AIF scheme, will be applicable only if the AIF does not have any downstream investment in a debtor company; and (v) investments in AIFs through intermediaries such as fund of funds or mutual funds have been scoped out. III.2.6 Omnibus Framework for recognising Self-Regulatory Organisations (SROs) for REs 3.29 Self-regulatory organisations (SROs) enhance the effectiveness of regulations by drawing upon the technical expertise of practitioner members. Their feedback and moral suasion aids in framing/ fine-tuning regulatory policies and managing nuances and trade-offs involved. SROs can also help in fostering innovation, transparency, fair competition and consumer protection. The Reserve Bank issued an Omnibus SRO Framework to develop industry standards of self-governance, supplementing the regulatory and supervisory efforts to instil a stronger compliance culture and to provide a consultative platform for all stakeholders. The framework prescribes the general objectives, functions, eligibility criteria, governance standards and lays down broad membership criteria along with other terms and conditions to be followed by SROs before recognition. Within the broad contours of the framework, along with certain specific instructions, the Reserve Bank in June 2024 invited applications for recognition of SROs for the NBFC sector. III.2.7 Credit/Investment Concentration Norms – Credit Risk Transfer 3.30 The extant large exposure framework (LEF) for NBFC - Upper layer (NBFC-UL) allows for offsetting of exposures to the original counterparty with eligible credit risk transfer instruments. In order to ensure uniformity and consistency in computation of exposures across the NBFC sector, middle layer entities (i.e., NBFC-ML) and base layer entities (i.e., NBFC-BL) are permitted to offset their exposures with eligible credit risk transfer instruments, namely cash margin/caution money/security deposit, central/state government guarantees and certain specified guarantees issued under the credit guarantee schemes. 3.31 Under eligible credit risk transfer instruments, guarantees from central/ state government shall be direct, explicit, irrevocable and unconditional. Further, direct exposures to central/state governments as well as exposures fully guaranteed by the central government have been exempted from concentration limits. While no concentration limit is prescribed for NBFC-BL, they are advised to put in place internal Board approved policies for credit/investment concentration limits for both single borrower/party and single group of borrowers/parties. III.2.8 Framework for dealing with D-SIBs 3.32 The Reserve Bank had issued the framework for dealing with Domestic Systemically Important Banks (D-SIBs) in 2014. The framework requires the Reserve Bank to: (a) identify and disclose the names of banks designated as D-SIBs annually; and (b) review the assessment methodology stipulated for identification of the D-SIBs on a periodic basis. Accordingly, a review of the assessment methodology was carried out, taking into consideration the functioning of the framework since its introduction, international developments in the field of systemic risk measurement and the experience of other countries in implementing the D-SIB framework. In the process, certain revisions have been implemented for the ‘payments’ sub-indicator (to account for the significant changes in payment landscape in India) under the ‘substitutability’ indicator, along with modifications in data requirements under ‘interconnectedness’ and ‘complexity’ indicators, to ensure a more comprehensive representation of systemic importance of banks. III.2.9 Regulatory Framework for Index Providers in the Indian Securities Market 3.33 Given the growing importance of passive funds and concerns regarding conflict of interest and governance practices relating to indices, the SEBI has brought index providers under its regulatory ambit through the Index Providers Regulations, 2024. 3.34 These regulations are applicable only to index providers that administer ‘significant indices’29 and are based on IOSCO principles for financial benchmarks. Accordingly, an index provider shall have to carry out assessment of adherence to the principles at least once in two years. These regulations are not applicable to index providers that administer (a) indices consisting only of global asset classes or consisting of global assets and Indian securities, whether for use in the Indian securities market or elsewhere; and (b) indices for exclusive use in a foreign jurisdiction. The benchmarks in the financial markets regulated by the Reserve Bank, including the significant benchmark notified by the Reserve Bank under section 45W of the Reserve Bank of India Act, 1934, are excluded from the purview of these regulations. III.2.10 Introduction of Beta version of T+0 rolling settlement cycle on optional basis 3.35 Pursuant to the recommendations of Risk Management Review Committee of the SEBI and approval of the SEBI Board, it was decided to put in place a framework for introduction of the Beta version of T+0 settlement cycle on an optional basis, in addition to the existing T+1 settlement cycle in the equity cash market for a limited set of 25 scrips and with a limited number of brokers. To ensure smooth implementation, the market infrastructure institutions (MIIs) have disseminated operational guidelines and frequently asked questions (FAQs) along with the list of 25 scrips for the Beta version of T+0 settlement cycle on their respective websites. A shortened settlement cycle will bring in cost and time efficiency as well as transparency in charges to investors and strengthen risk management at clearing corporations and the overall securities market ecosystem. III.2.11 Business Continuity for Clearing Corporations through Software as a Service (SaaS) Model 3.36 Clearing corporations (CCs) are important MIIs that provide risk management, centralised clearing and guaranteed settlement of trades. CCs operate as a multilateral system between stock exchanges, market participants, clearing banks and depositories. As a part of their risk management mechanism, CCs carry out comprehensive risk management across exchanges based on each trade executed by the members under the inter-operability framework. 3.37 Risk management systems (RMSs) of CCs aim to ensure smooth and uninterrupted functioning of the securities market by carrying out online real-time risk management of trades happening on stock exchanges. To manage disruptions impacting availability of RMS, the SEBI had issued a circular on ‘Business Continuity for Clearing Corporations through Software as a Service (SaaS) Model’ with detailed guidelines relating to the SaaS model for RMS of CCs. Each CC shall design a system to run its RMS related operations to risk manage trades for its clearing members using the RMS software of another CC. This system would be called SaaS-RMS. 3.38 Accordingly, two inter-operable CCs, i.e., National Clearing Limited (NCL) and Indian Clearing Corporation Limited (ICCL), have implemented the SaaS-RMS which would be activated within 30 minutes of occurrence of malfunction in their RMS. This remains the first of its kind redundancy model globally. III.3 Other Developments III.3.1 Customer Protection 3.39 The pattern of complaints received by the Offices of the Reserve Bank of India Ombudsman (ORBIOs) during the second half of 2023-24 indicates that complaints pertaining to loans and advances and digital complaints (i.e., complaints pertaining to mobile/ electronic banking, credit cards and ATM/ CDM/ debit cards) continue to constitute over half of the total complaints (Table 3.1), with two per cent sequential (q-o-q) growth during Q4:2023-24. | Table 3.1: Category of Complaints Received under the RB-IOS, 2021 | | Sr. No. | Grounds of Complaint | RB-IOS (October- December 2023) | RB-IOS (January- March 2024) | | Number | Share in per cent | Number | Share in per cent | | 1 | Loans and Advances & Non-adherence to FPC | 15,591 | 21.4 | 14,329 | 19.2 | | 2 | Mobile/ Electronic Banking | 11,328 | 15.6 | 11,278 | 15.1 | | 3 | Credit Card | 9,635 | 13.2 | 10,145 | 13.6 | | 4 | Opening/ Operation of Deposit accounts | 8,355 | 11.5 | 7,663 | 10.3 | | 5 | ATM/ CDM/ Debit card | 6,829 | 9.4 | 4,902 | 6.6 | | 6 | Others | 971 | 1.3 | 559 | 0.8 | | 7 | Remittance and Collection of instruments | 681 | 0.9 | 629 | 0.8 | | 8 | Para-Banking | 621 | 0.9 | 511 | 0.7 | | 9 | Pension | 656 | 0.9 | 411 | 0.6 | | 10 | Other products and services* | 18,180 | 25.0 | 24,121 | 32.4 | | Total | 72,847 | 100.0 | 74,548 | 100.0 | Note: * includes bank guarantee/ letter of credit, customer confidentiality, premises and staff, grievance redressal, death/ missing claims, etc.

Source: Reserve Bank of India. | III.3.2 Enforcement 3.40 During December 2023 – May 2024, the Reserve Bank undertook enforcement action against 161 REs {four PSBs; nine PVBs; one SFB; one foreign bank, two regional rural banks (RRBs); 132 co-operative banks; nine NBFCs and three HFCs} and imposed an aggregate penalty of ₹22.83 crore for non-compliance with/contravention of statutory provisions and/ or directions issued by the Reserve Bank. III.3.3 Deposit Insurance 3.41 The Deposit Insurance and Credit Guarantee Corporation (DICGC) extends insurance cover to bank depositors with the objective of maintaining their confidence in the banking system and promoting financial stability. The deposit insurance extended by DICGC covers all banks operating in India. The total number of banks registered with the DICGC stood at 1,997 comprising 140 commercial banks {including 43 regional rural banks (RRBs), two local area banks (LABs), six payment banks and 12 SFBs} and 1,857 co-operative banks. 3.42 With the current deposit insurance limit of ₹5 lakh, 97.8 per cent of the total number of deposit accounts (289.8 crore) are fully insured. Of the total assessable deposits of ₹218.23 lakh crore, 43.1 per cent were insured as on March 31, 2024. (Table 3.2). 3.43 The insured deposits ratio (i.e., the ratio of insured deposits to assessable deposits) was higher for cooperative banks (63.2 per cent), followed by commercial banks (42 per cent) (Table 3.3). Within commercial banks, PSBs had a much higher insured deposit ratio vis-à-vis PVBs. | Table 3.2: Coverage of Deposits | | (Amount in ₹ crore and No. of Accounts in crore) | | Sr. No. | Item | Mar 31, 2023 | Sep 30, 2023 | Mar 31, 2024 (P) | Percentage Variation | | (4) over (3) | (5) over (4) | | (1) | (2) | (3) | (4) | (5) | (6) | | | (A) | Number of Registered Banks | 2,026 | 2,009 | 1,997 | | | | (B) | Total Number of Accounts | 276.3 | 287.9 | 289.8 | 4.2 | 0.6 | | (C) | Number of Fully Protected Accounts | 270.5 | 281.8 | 283.3 | 4.2 | 0.5 | | (D) | Percentage (C)/(B) | 97.9 | 97.9 | 97.8 | | | | (E) | Total Assessable Deposits | 1,94,58,915 | 2,04,18,707 | 2,18,23,481 | 4.9 | 6.9 | | (F) | Insured Deposits | 86,31,259 | 90,32,340 | 94,10,674 | 4.6 | 4.2 | | (G) | Percentage (F)/(E) | 44.4 | 44.2 | 43.1 | | | Note: P = Provisional.

Source: DICGC |

| Table 3.3: Bank Group-wise Deposit Protection Coverage (As on March 31, 2024) | | (₹ crore) | | Bank Groups | No. of Insured Banks | Insured Deposits (ID) | Assessable Deposits (AD) | ID / AD (per cent) | | I. Commercial Banks | 140 | 86,66,217 | 2,06,46,359 | 42.0 | | i) Public Sector Banks | 12 | 56,47,647 | 1,15,49,283 | 48.9 | | ii) Private Sector Banks | 21 | 23,63,912 | 72,35,902 | 32.7 | | iii) Foreign Banks | 44 | 50,568 | 10,08,505 | 5.0 | | iv) Small Finance Banks | 12 | 89,532 | 2,15,426 | 41.6 | | v) Payment Banks | 6 | 16,794 | 16,937 | 99.2 | | vi) Regional Rural Banks | 43 | 4,96,827 | 6,19,010 | 80.3 | | vii) Local Area Banks | 2 | 937 | 1,295 | 72.4 | | II. Cooperative Banks | 1,857 | 7,44,457 | 11,77,122 | 63.2 | | i) UCBs | 1,472 | 3,71,859 | 5,56,977 | 66.8 | | ii) SCCBs | 33 | 62,395 | 1,46,144 | 42.7 | | iii) District Central Cooperative Banks | 352 | 3,10,202 | 4,74,000 | 65.4 | | Total | 1,997 | 94,10,674 | 2,18,23,481 | 43.1 | Note: Data is provisional.

Source: DICGC. | 3.44 Deposit insurance premium received by the DICGC grew by 11.7 per cent (Y-o-Y) to ₹23,879 crore (P) during 2023-24, of which commercial banks had a share of 94 per cent (Table 3.4). 3.45 The DIF with the DICGC is primarily built out of the premium paid by insured banks, investment income and recoveries from settled claims, net of income tax. DIF recorded a 17.2 per cent year on year increase to reach ₹1.99 lakh crore as on March 31, 2024. The reserve ratio (i.e., ratio of DIF to insured deposits) increased to 2.11 per cent from 1.96 per cent a year ago (Table 3.5). This is in line with global median of 2 per cent30. | Table 3.4: Deposit Insurance Premium | | (₹ crore) | | Period | Commercial Banks | Co-operative Banks | Total | | 2022-23 | 20,104 | 1,277 | 21,381 | | 2022-23:H1 | 9,872 | 641 | 10,513 | | 2022-23:H2 | 10,232 | 636 | 10,868 | | 2023-24 (P) | 22,543 | 1,336 | 23,879 | | 2023-24:H1 | 10,962 | 666 | 11,628 | | 2023-24:H2 | 11,581 | 670 | 12,251 | Note: P - Provisional.

Source: DICGC. |

| Table 3.5: Deposit Insurance Fund and Reserve Ratio | | (₹ crore) | | As on | Deposit Insurance Fund (DIF) | Insured Deposits (ID) | Reserve Ratio (DIF/ID) (Per cent) | | Mar 31, 2023 | 1,69,602 | 86,31,259 | 1.96 | | Sep 30, 2023 | 1,82,701 | 90,32,340 | 2.02 | | Mar 31, 2024 (P) | 1,98,753 | 94,10,674 | 2.11 | Note: P = Provisional.

Source: DICGC. | III.3.4 Corporate Insolvency Resolution Process (CIRP) 3.46 Since the provisions relating to the corporate insolvency resolution process (CIRP) came into force in December 2016, a total of 7,567 CIRPs commenced by March 2024, out of which 5,647 (74.6 per cent) have been closed. Of the closed CIRPs, around 20 per cent have been closed on appeal or review or settled, 19 per cent have been withdrawn, around 44 per cent have ended in orders for liquidation and 17 per cent have ended in approval of resolution plans (Table 3.6 and 3.7). | Table 3.6: Corporate Insolvency Resolution Process | | Year/Quarter | CIRPs at the beginning of the Period | Admitted | Closure by | CIRPs at the end of the Period | | Appeal/ Review/ Settled | Withdrawal under Section 12A | Approval of Resolution Plan | Commencement of Liquidation | | 2016-17 | 0 | 37 | 1 | 0 | 0 | 0 | 36 | | 2017-18 | 36 | 707 | 95 | 0 | 19 | 91 | 538 | | 2018-19 | 538 | 1,157 | 157 | 97 | 75 | 305 | 1,061 | | 2019-20 | 1,061 | 1,990 | 348 | 220 | 132 | 539 | 1,812 | | 2020-21 | 1,812 | 536 | 92 | 168 | 119 | 349 | 1,620 | | 2021-22 | 1,620 | 890 | 124 | 200 | 144 | 340 | 1,702 | | 2022-23 | 1,702 | 1,263 | 188 | 226 | 189 | 409 | 1,953 | | Apr- Jun, 23 | 1,953 | 252 | 38 | 46 | 43 | 96 | 1,982 | | Jul- Sep, 23 | 1,982 | 249 | 56 | 48 | 85 | 124 | 1,918 | | Oct- Dec, 23 | 1,918 | 247 | 34 | 34 | 80 | 133 | 1,884 | | Jan- Mar, 24 | 1,884 | 239 | 21 | 31 | 61 | 90 | 1,920 | | Total | | 7,567 | 1,154 | 1,070 | 947 | 2,476 | 1,920 | | Source: Compilation from website of the NCLT and filing by IPs. | 3.47 As on March 31, 2024, the outcome of CIRPs shows that of the operational creditor initiated CIRPs that were closed, 53 per cent were closed on appeal, review, or withdrawal (Table 3.8). | Table 3.7: Sectoral Distribution of CIRPs as on March 31, 2024 | | Sector | No. of CIRPs | | Admitted | Closed | Ongoing | | Appeal/ Review/ Settled | Withdrawal under Section 12 A | Approval of RP | Commencement of Liquidation | Total | | Manufacturing | 2849 | 399 | 414 | 452 | 1018 | 2283 | 566 | | Food, Beverages & Tobacco Products | 368 | 45 | 54 | 56 | 139 | 294 | 74 | | Chemicals & Chemical Products | 303 | 53 | 59 | 47 | 91 | 250 | 53 | | Electrical Machinery & Apparatus | 200 | 25 | 22 | 19 | 91 | 157 | 43 | | Fabricated Metal Products | 154 | 23 | 28 | 20 | 50 | 121 | 33 | | Machinery & Equipment | 313 | 57 | 53 | 32 | 105 | 247 | 66 | | Textiles, Leather & Apparel Products | 485 | 58 | 74 | 62 | 198 | 392 | 93 | | Wood, Rubber, Plastic & Paper Products | 333 | 44 | 48 | 59 | 115 | 266 | 67 | | Basic Metals | 478 | 60 | 43 | 119 | 168 | 390 | 88 | | Others | 215 | 34 | 33 | 38 | 61 | 166 | 49 | | Real Estate, Renting & Business Activities | 1631 | 302 | 259 | 139 | 451 | 1151 | 480 | | Real Estate Activities | 463 | 93 | 69 | 40 | 72 | 274 | 189 | | Computer and related activities | 214 | 28 | 36 | 17 | 83 | 164 | 50 | | Research and Development | 10 | 2 | 3 | 1 | 2 | 8 | 2 | | Other Business Activities | 944 | 179 | 151 | 81 | 294 | 705 | 239 | | Construction | 881 | 170 | 143 | 103 | 180 | 596 | 285 | | Wholesale & Retail Trade | 764 | 100 | 74 | 68 | 324 | 566 | 198 | | Hotels & Restaurants | 156 | 30 | 27 | 25 | 41 | 123 | 33 | | Electricity & Others | 211 | 27 | 20 | 42 | 80 | 169 | 42 | | Transport, Storage & Communications | 209 | 24 | 23 | 20 | 88 | 155 | 54 | | Others | 866 | 102 | 110 | 98 | 294 | 604 | 262 | | Total | 7567 | 1154 | 1070 | 947 | 2476 | 5647 | 1920 | Note: The distribution is based on the CIN of corporate debtors and as per National Industrial Classification (NIC 2004).

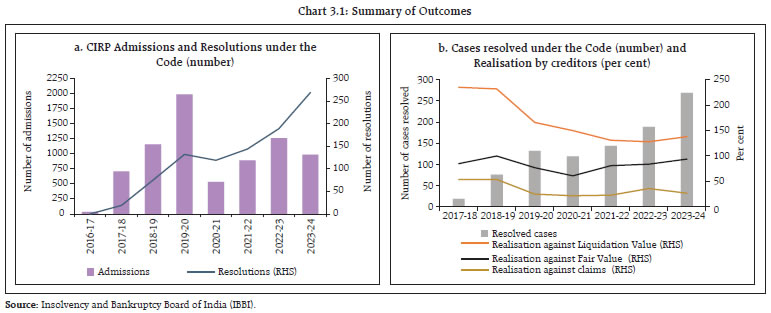

Source: Insolvency and Bankruptcy Board of India (IBBI). |

| Table 3.8: Outcome of CIRPs, Initiated Stakeholder-wise, as on March 31, 2024 | | Outcome | Description | | CIRPs initiated by | | Financial Creditor | Operational Creditor | Corporate Debtor | FiSPs | Total | | Status of CIRPs | Closure by Appeal/Review/Settled | 347 | 798 | 9 | 0 | 1,154 | | Closure by Withdrawal u/s 12A | 306 | 756 | 8 | 0 | 1,070 | | Closure by Approval of RP | 547 | 322 | 74 | 4 | 947 | | Closure by Commencement of Liquidation | 1,148 | 1071 | 257 | 0 | 2,476 | | Ongoing | 1,092 | 720 | 108 | 0 | 1,920 | | Total | 3,440 | 3,667 | 456 | 4 | 7,567 | | CIRPs yielding RPs | Realisation by FCs as per cent of Liquidation Value | 176.3 | 129.5 | 146.7 | 134.9 | 161.8 | | Realisation by FCs as per cent of their Claims | 32.4 | 25.1 | 18.2 | 41.4 | 32.1 | | Average time taken for Closure of CIRP (days) | 683 | 691 | 573 | 677 | 679 | | CIRPs yielding Liquidations | Liquidation Value as per cent of Claims | 5.6 | 9.1 | 8.5 | - | 6.3 | | Average time taken for Closure of CIRP (days) | 495 | 492 | 437 | - | 495 | Note: FiSPs = Financial service providers. A “Financial service provider” means a person engaged in the business of providing financial services (other than banks) in terms of authorisation issued or registration granted by a financial sector regulator.

Source: Insolvency and Bankruptcy Board of India (IBBI). | 3.48 The initiatives being taken to improve the outcomes under the Insolvency and Bankruptcy Code, 2016 (the ‘Code’) include amendments in the regulations, increasing the effective strength of the National Company Law Tribunal (NCLT), setting up of an integrated IT platform and regular interactions with all stakeholders, including NCLT. Some of these initiatives have started yielding results with a rise in the number of admitted cases, approved resolution plans and realisable value (Chart 3.1 a). The number of resolved cases under the Code and realisation by creditors as a proportion to liquidation value and fair value show an increasing trend (Chart 3.1 b). 3.49 Till March 31, 2024, a total of 947 corporate debtors have been resolved under the Code. Cumulatively till March 31, 2024, creditors have realised ₹3.36 lakh crore under the resolution plans. Creditors have realised around 162 per cent of liquidation value, 85 per cent of fair value and over 32 per cent of admitted claims. Realisable value through resolution plans does not include: (a) possible realisation through corporate and personal guarantors and recovery against avoidance transactions; (b) CIRP cost; and (c) other probable future realisations, such as increase in value of diluted equity and funds infused into the corporate debtor, including capital expenditure by the resolution applicants. About 40 per cent of the CIRPs that yielded resolution plans were defunct companies. In these cases, the claimants have realised 155 per cent of the liquidation value and 20 per cent of their admitted claims.  3.50 Although the primary objective of the Code is providing relief to corporate debtors in distress, the Code has also resulted in behavioural changes among debtors who are settling their dues even before start of insolvency proceedings. Till March 2024, 28,818 applications for initiation of CIRPs of corporate debtors having underlying default of ₹10.22 lakh crore were withdrawn before their admission. 3.51 At end-March 2024, the total number of CIRPs ending in liquidation was 2,476 of which, final reports have been submitted in 960 cases for which corporate debtors together had outstanding claims of ₹2.28 lakh crore, but the assets were valued at only ₹0.10 lakh crore. The liquidation of these companies resulted in 87 per cent realisation of the liquidation value. 3.52 The Code endeavours for early closure of various processes in resolution. The 947 CIRPs that have yielded resolution plans by March 2024 took, on an average, 565 days (adjusting for the time excluded by the Adjudicating Authority) for conclusion of processes, while incurring an average cost of 1.25 per cent of liquidation value and 0.74 per cent of resolution value. Similarly, the 2,476 CIRPs that ended up in orders for liquidation took an average of 495 days for conclusion. Further, 960 liquidation processes that were closed by submission of final reports took an average of 605 days for closure. III.3.5 Developments in International Financial Services Centre (IFSC) 3.53 The total asset size of IFSC banking units (IBU) stood at US$ 60.4 billion in March 2024. The cumulative banking transactions undertaken by IBUs crossed US$ 796 billion. Additionally, the cumulative non-deliverable forwards (NDFs) booked reached US$ 439 billion. 3.54 As on April 30, 2024, five entities had been registered by the International Financial Services Centres Authority (IFSCA) as bullion trading members (Bullion TM), six as bullion trading and clearing member (Bullion TMCM), two as bullion professional clearing members (Bullion PCM) and three as bullion trading members cum self-clearing members. Further, 126 ‘Qualified Jewellers’ were notified by the IFSCA. As on April 30, 2024, 8.38 tonnes of gold and 926.86 tonnes of silver had been traded on the India International Bullion Exchange (IIBX) and the turnover stood at US$ 531.44 million and US$ 714.43 million for gold and silver, respectively. The IIBX facilitates efficient price discovery and ensures standardisation, quality assurance and sourcing integrity, apart from giving impetus to financialisation of gold in India. 3.55 The asset management ecosystem at the GIFT-IFSC is growing rapidly and comprises 114 Fund Management Entities, 120 AIFs and four Investment Advisors. The total targeted corpus to be raised by AIFs in the IFSC, including via ‘green shoe’ options, stood at around US$ 33 billion up to March 2024. 3.56 The insurance ecosystem in the GIFT-IFSC comprises 35 entities, including 12 IFSC Insurance Offices (IIOs) and 23 IFSC Insurance Intermediary Offices (IIIOs). The total reinsurance premium booked by IFSC Insurance offices was US$ 360 million and the total reinsurance premium transacted by insurance intermediaries was US$ 918 million, up to March 2024. III.3.6 Insurance 3.57 During 2023-24, new business premium of life insurance industry grew by 1.8 per cent, reaching ₹3.78 lakh crore (provisional) from ₹3.71 lakh crore in the last financial year. The total premium31 underwritten by general and health insurers was ₹2.90 lakh crore during 2023-24 (provisional) as against ₹2.57 lakh crore reported during the previous financial year - a y-o-y growth of 12.8 per cent. Among various lines of business, the health insurance segment (the largest among the non-life insurance sector) has reported the highest growth of 20.2 per cent while the growth in motor insurance premium (second largest segment under non-life insurance) was 12.9 per cent year-on-year. 3.58 In alignment with the 2023-24 budgetary announcements regarding reducing regulatory compliance burden and promoting ease of doing business, encouraging innovation, competition, and sustainable growth in the insurance industry, the IRDAI has replaced 37 regulations with seven regulations and has introduced two new regulations to enhance clarity and coherence in the regulatory landscape. These changes and new regulations, inter alia, (a) provide more flexibility to insurers to manage their expenses including commissions; (b) modify the parameters for compliance and measurement of statutory rural, social sector and motor third party obligations by insurers; (c) establish a digital public infrastructure named ‘Bima Sugam’ to serve as a one stop solution for all insurance stakeholders; (d) improve the procedures and practices adopted by insurers and distribution channels to fulfil their obligations towards policyholders; (e) promote prudent practices in risk management related to outsourcing activities by insurers; and (f) promote good governance in product design and pricing, including strengthening of the principles governing guaranteed surrender value and special surrender value along with disclosures thereof. 3.59 Furthermore, the revamped regulations on ‘Registration, Capital structure, Transfer of shares and Amalgamation of Insurers’ of the Insurance Regulatory and Development Authority of India (IRDAI) aim to simplify various processes, including registration of insurers, transfer of shareholding, amalgamation of insurers and listing of shares on stock exchanges. The regulation on ‘Corporate governance for Insurers’ aims to establish a robust governance framework for insurers, defining the roles and responsibilities of the board and management. The regulation on ‘Registration and Operations of Foreign Reinsurers Branches and Lloyd’s India’ aims to improve the environment for the growth and expansion of the reinsurance sector, ultimately benefiting both insurers and policyholders in India. Further, the regulation on ‘Actuarial, Finance and Investment Functions of Insurers’ aims to implement sound and responsive management practices for effective discharge of actuarial, finance, and investment functions, safeguarding policyholders’ interests, and promoting ease of doing business. III.3.7 Pension Funds 3.60 The National Pension System (NPS) and the Atal Pension Yojana (APY) have continued to progress in terms of the total number of subscribers and Asset Under Management (AUM). During 2023-24, the number of subscribers under NPS and APY together have shown a growth of 16.3 per cent, whereas their AUM has recorded 30.5 per cent growth. The combined subscriber base under NPS and APY has reached 7.35 crore in March 2024, with an AUM of ₹11.72 lakh crore (Chart 3.2), which is primarily invested in fixed income instruments (Chart 3.3). 3.61 According to a Position paper32 by NITI Aayog, 78 per cent of India’s older population is currently living without any pension cover. Further, the United Nations Population Fund33 has estimated the decadal growth of India’s elderly population at 41 per cent. The elderly population is projected to double to over 20 per cent of the total population by 2050. By 2046, the elderly population is likely to surpass the population of children aged 0 to 15 years. This demographic shift will significantly impact the demand for pension benefits and the sustainability of pension schemes in India. If adequate provisions are not made for pension it can lead to a systemic risk in the economy.

3.62 To address the challenges posed by anticipated demographic shifts in India, the following steps have been taken over the years: (a) transition from Defined Benefit pension system to Defined Contribution pension system through the NPS in 2004; and (b) introduction of various old age pension schemes by central government such as Indira Gandhi Old Age Pension Scheme (IGNOAPS), Pradhan Mantri Vaya Vandana Yojana, and Pradhan Mantri Shram Yogi Maandhan Yojana along with similar such schemes by various state governments. An effective participation and coordination between various private and public entities, along with a multipronged and multiagency approach, are essential to make India a fully pensioned society. 3.63 As India embraces technological advancements including Artificial Intelligence (AI) and the Internet of Things (IoT), the pension sector will also face a structural transformation in how services are delivered and managed. While the integration of cutting-edge technologies will improve the efficiency of the overall architecture of the pension ecosystem in India, it will also pose serious threats in terms of cyberattacks, data privacy and security. With respect to the evolving cybersecurity risks, the Pension Fund Regulatory and Development Authority (PFRDA) has been proactively taking various measures to strengthen the IT infrastructure of the NPS ecosystem. Given the dynamic nature of these challenges, active cooperation amongst stakeholder bodies is vital to effectively address the cybersecurity issues in India. Summary and Outlook 3.64 The global financial system has demonstrated remarkable resilience in the face of numerous shocks over the past year. Nonetheless, the attention of global regulatory bodies is on mitigating new and emerging sources of risk that could potentially undermine this resilience. In this context, regulators are prioritising the management of risks stemming from the rapid advancement of financial technology and the escalating threat of cyberattacks. Recognising the potential for these factors to heighten vulnerabilities both at the institutional and systemic levels, regulatory institutions are intensifying their efforts to fortify financial institutions’ standard operating procedures for ensuring business continuity in any resolution process. 3.65 Domestic regulatory initiatives continue to focus on the resilience of financial intermediaries, bolstering efficiency within financial markets, implementing global best practices, streamlining regulatory compliance processes and enhancing customer protection measures. Regulators are consolidating the gains of the past while remaining vigilant in monitoring and adapting to the evolving financial landscape and making the financial system future ready.

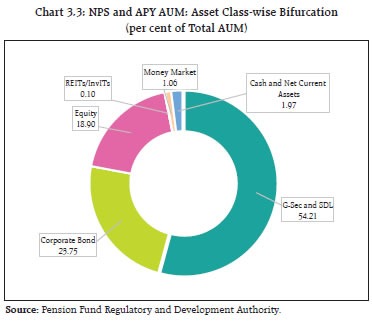

|