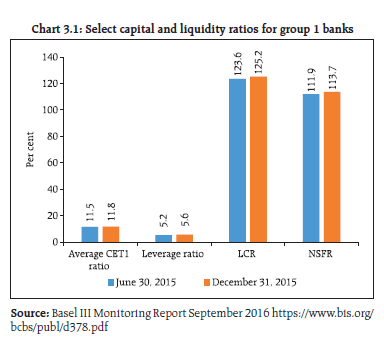

The global regulatory standards continue to be strengthened. However, the risks of divergence from the demanding global standards amidst discriminatory treatment of foreign financial institutions have increased. Further, cutting down on correspondent banking activities by some of the major global banks due to regulatory and profitability concerns may discourage formal financial intermediation channels to reach out to financially underserved parts of the world. At the same time, some risks inherent in banks may be getting transferred to other segments of the financial markets due to increasing regulatory scrutiny and elevated capital requirements for banks. In domestic financial markets, a number of macroprudential and other regulatory measures taken are expected to enhance transparency in the functioning of financial markets and empower customers with wider product-choices and more effective grievance redressal, leading to further strengthening of the financial sector. An effective implementation of guidelines on capacity building in the banking sector and shift to Ind AS for banks and insurance companies will require dedicated efforts by these entities. While regulatory measures on partial credit enhancement will further support the corporate bond market, the guidelines on market mechanism and large exposures will help in reducing banks’ exposures to large corporates. Introduction of two new life cycle funds and creation of a separate asset class for alternate investment are expected to provide more options to investors in pension schemes. Section A International and domestic regulatory developments I. The banking sector 3.1 Major developments in global regulatory standards include regulatory capital treatment of banks’ investments in instruments that comprise total loss-absorbing capacity (TLAC)1 for global systemically important banks (G-SIBs) and standards for interest rate risk in the banking book (IRRBB)2. In addition, the Basel Committee on Banking Supervision (BCBS) has released a consultative document3 and a discussion paper on policy considerations related to the regulatory treatment of accounting provisions under the Basel III regulatory capital framework; it has also issued revisions to the securitisation framework4. 3.2 Adoption of BCBS standards by various jurisdictions, as reflected in their Regulatory Consistency Assessment Program (RCAP) reports, has been satisfactory. However, given the political economies’ waning appetite for globalisation, especially in the developed countries, the risk of major divergences from Basel standards, especially the more demanding ones, become substantive. Already there are signs of discomfort, especially in the Eurozone, over new proposals such as risk weighting floors for credit risk and more capital for conduct risk. Meanwhile, there is also a proposal by the European Commission to stipulate higher capital requirements for large foreign banks with subsidiaries in the EU. Seen as retaliation to the extant US regulatory stance on European banks, these developments may impact global cooperation on the standard setting mechanism. On the other side of the Atlantic, it is speculated that the political transition in the US could pose risks to Dodd Frank reforms. At the same time, debates over effectively addressing the issue of ‘too big to fail’ (TBTF) continue (Box 3.1). The constant tweaking of regulations seems to be impacting IT systems and budgets suggesting the need for an infrequent but periodical calendar-based approach to regulatory changes.9 Box 3.1: TBTF – Who is benefitting? The previous issues of FSR have highlighted that globally the balance sheet size of ‘big’ banks had continued to grow, notwithstanding the regulatory measures (additional capital requirements and resolution framework leading to ‘living wills’). The International Monetary Fund (IMF), in its Global Financial Stability Report (GFSR), released in April 20145, had indicated that the probability of governments bailing out SIBs still remained high, across regions. Besides the controversies surrounding the label of TBTF – (one, without paying an insurance premium the bank concerned receives an insurance from the tax payer against defaults and two, the ensuing moral hazard that comes with the insurance in the form of incentivising bank managements to take riskier bets) – theoretically, this added insurance policy should increase the valuations of banks being labelled as TBTF. However, if that happens, the TBTF transfers wealth from new buyers to existing holders of equity/debt. In other words, new buyers are paying for the TBTF insurance via higher equity and bond prices. “To summarise, the value of being designated TBTF is capitalised into the price of a firm’s equities and its bonds. TBTF provides a windfall capital gain to shareholders and creditors at the time of the designation. But after that, new buyers of equities and debt are paying for that status. Consequently, determining who gets “bailed out” when an institution is TBTF is a more complicated task than it appears”. (Waller, Christopher, 2016) There is some evidence that the TBTF status is not only visible in lower funding costs but is also reflected in abnormally low returns (adjusted to risks) on their stocks (Gandhi and Lustig 2015). Similar evidence could be gathered for German bank stocks (Nitschka, Thomas 2016).The larger issue that may be of interest is that debt and associated covenants have a disciplining role too on managements. But for public institutions, with embedded sovereign guarantee, there may not be any incentive to insist on covenants. Although, the long term foreign currency debt could be an exception to this, the disciplining role of debt might be at risk. In fact, beyond a certain threshold, there could possibly be a risk of regulatory capture by these institutions as their bargaining power in terms of systemic stability increases. This in turn may lead to ‘accounting’ and ‘regulatory’ solutions (forbearances) to an otherwise economic problem. While the debate continues, the Financial Stability Board (FSB) has published the 2016 list of global systemically important banks (G-SIBs)6 and global systemically important insurers (G-SIIs)7. The 30 banks and 9 insurers on the 2016 lists remain the same as those on the 2015 list, but in the G-SIB list four banks moved to a higher bucket, and three banks moved to a lower bucket which correspond to required levels of additional capital buffers. On domestic front also, there was no change in the banks identified as domestic systemically important banks (D-SIBs) in 20168. References: 1. Waller, Christopher, (2016): Who Exactly Benefits from Too Big To Fail?, Economic Research, Federal Reserve Bank of St. Louis, 2016, NO. 13 (Posted 2016-06-27) 2. Gandhi and Lustig, (2015): Size Anomalies in U.S. Bank Stock Returns, The Journal of Finance, April 2015, Volume 70, Issue 2 3. Nitschka, Thomas, (2016): Is There a Too-Big-to-Fail Discount in Excess Returns on German Banks’ Stocks?, International Finance 3.3 While on the one hand, with reforms, banks appear to be getting more resilient in terms of capital and liquidity with the gradual implementation of Basel III (see Chart 3.1), on the other hand they have cut activities that are deemed too costly to be commercially pursued amid regulatory and profit pressures.10 Further, cutting down on correspondent banking activities by some of the major global banks due to regulatory and profitability concerns may discourage formal financial intermediation channels to reach out to financially underserved parts of the world. With increasing scrutiny of banks and improved capital provisions, banks have become stronger than they were before the crisis. However, a view is emerging on whether the risks are moving into the markets. There is also scepticism over the adequacy of the re-regulatory process in appreciating and addressing the gap between risk appetite and risk capacity (the current framework does not prescribe capital requirements based on this gap) of entities that operate across the financial sector on the one hand and unambiguously distinguishing and treating credit and liquidity risks on the other (Persaud, Avinash 2016).  3.4 The process of implementation of the BCBS standards for the banks in India continues as Reserve Bank issued the final guidelines on the Large Exposures (LE) Framework to be fully implemented by March 31, 2019 (Table 3.1). Although the BCBS proposals to apply non-zero risk weights and disallow exemption from the large exposure (LE) rules on banks’ sovereign exposure are still work-inprogress, the Reserve Bank has allowed exemptions to the sovereign exposures from LE limits in its LE Framework which is in line with the BCBS’ April 2014 LE standards. In addition, elements of the Basel III capital framework will be selectively applied to the four all-India financial institutions (AIFIs) from April 1, 2018.11 II. The securities market 3.5 The Growth and Emerging Markets Committee (GEMC) of the International Organisation of Securities Commissions (IOSCO) has published its report on ‘Corporate Governance in Emerging Markets.’12 The report, inter-alia, discusses the issue of ‘Director Independence’ based on (i) the concept of ‘independence’ itself; and (ii) the ability of directors to provide constructive criticism, without being divisive. 3.6 SEBI has undertaken several regulatory reform measures (Table 3.1) for the domestic securities market including tightening of insider trading norms and enhancing transparency in the policies of credit rating agencies (CRAs). Further, IOSCO has recently published a consultation report13 on other CRA products (OCPs). As the CRAs in India also widen their reach and scope and offer a number of services through their affiliates, which may not be regulated, the contents and objectives of the report are very relevant and will be useful in understanding the risks and benefits arising from such products and services of CRAs. III. The insurance sector 3.7 The International Association of Insurance Supervisors (IAIS) recently came out with a document14 which set out the rationale for the IAIS’s revisions of the non-traditional non-insurance (NTNI) definition and a detailed description of potentially systemic insurance product features. It also revised and clarified the concepts of substantial liquidity risk and macroeconomic exposure. IV. Recent regulatory initiatives and their rationale 3.8 Some of the recent regulatory initiatives, including prudential and consumer protection measures with the rationale thereof are given in Table 3.1 | Table 3.1: Important prudential and consumer protection measures & rationale thereof July – December 2016 | | Date | Measure | Rationale/Purpose | | 1. Reserve Bank of India | | July 14 | An Inter-regulatory Working Group on Fin Tech and Digital Banking set up. | -

To undertake a scoping exercise to gain a general understanding of the major Fin Tech innovations/ developments, counterparties/entities, technology platforms involved and how markets, and the financial sector in particular, are adopting new delivery channels, products and technologies. -

To assess opportunities and risks arising from the digitisation of the financial system. -

To assess the implications and challenges for various financial sector functions such as intermediation, clearing and payments being taken up by non-financial entities. -

To examine cross-country practices. -

To chalk out appropriate regulatory responses with a view to re-aligning/re-orienting regulatory guidelines and statutory provisions for enhancing Fin Tech/digital banking-associated opportunities while simultaneously managing the evolving challenges and risk dimensions. | | July 21 | Banks were permitted to reckon government securities held by them up to another 1 per cent of their net demand and time liabilities (NDTL) under the facility to avail liquidity for liquidity coverage ratio (FALLCR) within the mandatory SLR requirements as level 1 high quality liquid assets (HQLA) for the purpose of computing their liquidity coverage ratio (LCR). Hence, the total carve-out from SLR available to banks will be 11 per cent of their NDTL. | The Reserve Bank started the phasing-in of LCR under Basel III reforms from January 2015 with a minimum requirement of 60 per cent with a gradual increase of 10 per cent each year to reach 100 per cent from January 2019. As India already had a statutory liquidity ratio (SLR) and the introduction of LCR significantly increased the requirement of holding HQLAs by banks, a need was felt to rationalise the HQLA requirements under the two ratios by common reckoning of government bonds- to a certain extent. This measure will help banks in meeting the increasing minimum LCR while maintaining their financing of other assets. | | August 4 | Website 'Sachet' launched to curb illegal collection of deposits. | India is a vast country with different types of entities engaged in providing financial services. Further, the presence of different regulators for different kinds of entities, overlapping of regulatory roles, the presence of regulatory gaps and low levels of financial literacy among the people make it difficult for the common man to differentiate between a regulated and an unregulated entity and to find a suitable forum for redressal of his grievances arising from transactions with such entities. This initiative enables the public to obtain information regarding entities that are allowed to accept deposits, lodge complaints and also share information regarding illegal acceptance of deposits by unscrupulous entities. The website will also help enhance coordination among regulators and state government agencies and thus be useful in curbing instances of unauthorised acceptance of deposits by unscrupulous entities. | | August 4 | Regulatory guidelines on implementing the Indian Accounting Standards (Ind AS) for all-India financial institutions issued. AIFIs shall comply with Ind AS for financial statements for accounting periods beginning from April 1, 2018 onwards, with comparatives for the period ending March 31, 2018 or thereafter. | MCA outlined the roadmap for implementing the international financial reporting standards (IFRS) converged Ind AS for banks, non-banking financial companies, select all-India term lending and refinancing institutions and insurance entities in January 2016. All scheduled commercial banks have to comply with Ind AS from April 1, 2018. The guidelines broadly advises AIFIs about the steps to facilitate implementation of Ind AS. | | August 25 | Guidelines on enhancing credit supply for large borrowers through the market mechanism issued. The guidelines introduced the concepts of ‘specified borrower’ and ‘normally permitted lending limit’ (NPLL) for the purpose of setting in disincentives for borrowing from the banking sector beyond a certain cut-off. NPLL means 50 per cent of the incremental funds raised by a specified borrower over and above the aggregate sanctioned credit limit (ASCL) as on the reference date, in the financial years (FYs) succeeding the FY in which the reference date falls. As per the prudential measures proposed under the disincentive mechanism, from 2017-18 onwards incremental exposure of the banking system to a specified borrower beyond NPLL shall be deemed to carry higher risk which shall be recognised by way of additional provisioning (3 percentage points over and above the applicable provision) and higher risk weights (75 percentage points over and above the applicable risk weight) for the exposure. | While the regulatory measures for addressing the concentration risk to individual banks arising from their exposures to individual and group entities existed since 1989, build-up of concentration risk at the banking system level from banks’ collective exposures to specific counterparties has been a matter of concern. These guidelines address this concern by dis-incentivising aggregate borrowing by a borrower from the banking system beyond a cut-off limit. | | August 25 | In a partial review of its instructions on ‘partial credit enhancement (PCE) to corporate bonds’ the Reserve Bank allowed an increase in the aggregate exposure limit from the banking system for a specific bond issue to 50 per cent of the bond issue size from the extant limit of 20 per cent of the bond issue size. In addition, within the aggregate limit, a limit of up to 20 per cent of the bond issue size for an individual bank has been allowed. | Reserve Bank’s circular dated September 24, 2015 on PCE capped the aggregate exposure limit of all banks towards the PCE for a given bond issue at 20 per cent of the bond issue size. In order to further support the development of corporate bonds market, RBI has allowed this higher exposure limit. | | September 1 | Guidelines on Sale of Stressed Assets by Banks issued. | The Reserve Bank, as part of the Framework for Revitalising Distressed Assets in the Economy, had previously amended certain guidelines relating to sale of non-performing assets (NPAs) by banks to Securitisation Companies (SCs)/ Reconstruction Companies (RCs). The current guidelines have been issued with a view to further strengthen banks’ ability to resolve their stressed assets effectively, and put in place an improved framework governing sale of such assets by banks to SCs/RCs/other banks/ Non-Banking Financial Companies /Financial Institutions etc. | | October 27 | A framework permitting AD category-I banks to allow start-ups to raise external commercial borrowings (ECB) limited to US$ 3 million or equivalent per financial year issued. | This was issued with a view to facilitating start-ups to access funding through ECB route. | | November 10 | Schemes for stressed assets – revisions issued, which revise certain provisions under various previous guidelines -- Framework for Revitalising Distressed Assets, Flexible Structuring of Project Loans, Strategic Debt Restructuring Scheme, Scheme for Sustainable Structuring of Stressed Assets, etc. | The changes in these guidelines have been carried out with the objectives of : -

harmonising the stand-still clause as applicable in case of the Strategic Debt Restructuring Scheme with other guidelines; -

clarifying the deemed date of commencement of commercial operations; and -

partially modifying of certain guidelines based on the experience gained in using these tools in resolving stressed assets and feedback received from stakeholders as also taking into consideration the requirements of the construction sector. | | November 21 | A short-term deferment of classification of the loan assets of its regulated entities (REs) as substandard allowed. Under this instruction, an additional 60 days have been permitted beyond what is applicable for the concerned RE for recognition of a loan account as substandard. This relaxation will be available only in certain cases of dues payable between November 1, 2016 and December 31, 2016. | In view of the need of some more time to repay the loan dues by small borrowers due to consequences arising from withdrawal of the legal tender status of the existing ₹500 and ₹1,000 notes (SBN), RBI has allowed this short term change in its income recognition, asset classification and provisioning (IRAC) norms. | | December 1 | Final guidelines on large exposures (LE) Framework issued with a view to implementing the BCBS’ Standards on Large Exposures (April 2014) with effect from March 31, 2019. The salient features of the proposed LE Framework include: -

The LE limit in respect of each counterparty and group of connected counterparties, under normal circumstances, will be capped at 20 per cent and 25 per cent respectively of the eligible capital base. -

The eligible capital base will be defined as the Tier 1 capital of the bank as against ‘Capital Funds’ at present. -

A group of connected counterparties will be identified on the basis of objectively defined ‘control’ criteria. | Concentration risk arising from large exposures of banks to a few single or group of interconnected counterparties has been a matter of concern and Reserve Bank had prescribed single and group exposure norms in the matter since March 1989. In order to foster a convergence among widely divergent national regulations on dealing with large exposures, the BCBS issued the Standards on ‘Supervisory framework for measuring and controlling large exposures’ in April 2014. The Reserve Bank has decided to suitably adopt these standards for banks in India. These standards propose to objectively define a group of connected counterparties on the basis of ‘Control’ criteria and lower the exposure ceiling to such groups. These standards also propose adoption of “Look Through Approach” (LTA) for collective investment undertakings (CIUs), securitisation vehicles and other structures to determine the relevant counterparties. | | 2. Securities and Exchange Board of India (SEBI) | | September 1 | Additional risk management norms for commodity derivatives markets issued. These include at least a 2-day margin period of risk, delivery period margins, steps to regain matched books, concentration margins and default waterfalls for national commodity derivatives exchanges. | To streamline and strengthen the risk management framework and to avoid any systemic risk across national commodity derivatives exchanges. | | September 7 | Guidelines on restrictions on promoters and whole-time directors of compulsorily delisted companies pending fulfilment of exit offers to the shareholders issued. | To ensure effective enforcement of exit option to the public shareholders in case of compulsory delisting. | | September 20 | Guidelines on Enhanced Disclosures (viz. commission paid to distributors, average Total Expense Ratio) in Consolidated Account Statement (guidelines issued on September 20, 2016 read with that issued on March 18, 2016) | To increase transparency of information to investors. | | September 23 | Regulatory framework for commodity derivatives brokers issued. | To harmonise regulatory provisions for brokers across equity and commodity derivatives markets. | | October 10 | Exclusively listed companies (ELC) of derecognised / non-operational / exited stock exchanges placed in the Dissemination Board (DB) | To protect the interest of shareholders of such ELCs by providing them an exit option | | October 26 | Guidelines on freezing of promoter and promoter group demat accounts for non-compliance with certain provisions of listing regulations issued. | To ensure effective enforcement with regard to the prescribed 'uniform fine structure' for non-compliance with certain provisions of SEBI’s listing regulations and standard operating procedure for suspension and revocation of trading of specified securities. | | November 1 | Enhanced standards for credit rating agencies (CRAs) issued. These are aimed at bringing in greater transparency in CRAs’ policies, enhancing the standards followed by the industry thereby facilitating ease of understanding the ratings by investors. The circular broadly covers the policies with respect to non-co-operation by the issuer, accountability and managing the conflict of interest of the members of a rating committee, standardising the format of CRAs’ press releases and disclosure on their websites amongst others. | CRAs play an important role in financial sectors. Reducing mechanistic reliance on CRAs was one of the major reform agendas of the Financial Stability Board in the wake of the global financial crisis. However, due to challenges in finding alternative standards of creditworthiness and inadequate internal resources for risk assessment, CRAs remain significant providers of credit ratings in India and other developing countries. Against this backdrop, higher transparency in CRAs’ procedures and policies can add to a better understanding of the ratings assigned by them by the users of such ratings. | | November 23 | SEBI’s board decision – FPIs permitted to invest in unlisted non-convertible debentures and securitised debt instruments. | To enhance the investor base in unlisted debt securities and securitised debt instruments. | | November 23 | SEBI’s board decision- amendment to listing regulations to enforce disclosures and shareholder approval for private equity funds entering into compensation agreements to incentivise promoters, directors and key managerial personnel of listed investee companies. | To prevent potential unfair practices. | | 3. Insurance Regulatory and Development Authority of India (IRDAI) | | July 12 | Non insistence of Advance Discharge Voucher for releasing payments | In order to protect the policyholders, the Authority issued this guideline intimating the Life Insurers “Not to withhold or delay the payment for the reason of non-execution of advance discharge voucher and to make the policy payment to the policyholders to discharge its contractual obligations”. | | July 18 | Insurance Regulatory and Development Authority of India (Health Insurance) Regulations, 2016. | -

Additional norms for protection of interest of policyholders -

Enhance the scope of health insurance product innovation -

Enabling mechanism to reward healthy behaviour of policyholders -

Facilitation in group health insurance product approval process | | August 5 | The Authority has issued IRDAI (Listed Indian Insurance companies) Guidelines, 2016 applicable to all insurers who have listed their equity shares or are in the process of getting their shares listed on the stock exchanges. These guidelines are in addition to IRDAI (Issuance of Capital by Indian Insurance Companies transacting Life Insurance Business) Regulations, 2015 and IRDAI (Issuance of Capital by Indian Insurance Companies transacting other than Life Insurance Business) Regulations, 2015 and cover aspects related to minimum promoter shareholding and provisions relating to transfer of the shares. The Guidelines are also applicable to an insurance intermediary licensed by the Authority provided that such insurance intermediaries are drawing more than 50 per cent of its revenue from insurance business. | The guidelines seek to address operational aspects such as monitoring the foreign direct investment (FDI) in insurance sector, approval of share transfer, ceiling of holding on various classes of the investors, listing of the Insurers. | | November 7 | Guidelines on Point of Sales (POS) Person for Life Insurance | These guidelines allowing marketing of simple plain products by POS persons are aimed at providing easy access to life insurance to people at large and enhancing insurance penetration and density. | | November 7 | Guidelines on Point of Sales (POS) Products for Life Insurance | The guidelines prescribe the eligible products that can be sold by Point of Sales Persons. | | 4. Pension Fund Regulatory and Development Authority (PFRDA) | | November 4 | Two new life cycle (LC) funds (LC 75 and LC 25) introduced for private sector subscribers, in addition to the existing life cycle fund to provide a pre-programmed diversification of assets in various asset classes as per the age and risk profile of the subscriber. | A prudential investor regime envisages appropriate fund-age allocation and diversification across asset classes in accordance with the risk appetite of the subscribers. However, for those unwilling or unable to make a choice of asset allocations, life cycle funds not only provide a simpler and professional way of managing funds but also provide investors with a pre-programmed opportunity to adequately diversify and rebalance their portfolios in accordance with their age-specific risk levels. The life cycle fund is based on the globally accepted best practice of ‘declining risk appetite with increasing age.’ Presently, NPS provides for one life cycle fund option to NPS subscribers wherein equity allocation is capped at 50 per cent, tapering off to 10 per cent at the time of retirement. This life cycle fund is also the default option for private sector subscribers. Now, in accordance with the recommendations of the Bajpai Committee, two more life cycle funds have been floated: a) the aggressive life cycle fund wherein for the first time subscribers are allowed investments up to 75 per cent in equity, tapering off to 15 per cent by the time they near retirement, b) the conservative life cycle fund wherein the maximum exposure in equity shall be 25 per cent, tapering off to 5 per cent by the time subscriber approaches retirement. | | November 4 | Guidelines on the creation of separate asset class A (for alternate investments) issued. This creates a separate asset class ‘A’ (for alternate investments) for private sector NPS subscribers in addition to existing asset classes E, C and G. Investments in asset class A will comprise of the following- 1. Commercial mortgage based securities or residential mortgage based securities. 2. Units issued by real estate investment trusts regulated by SEBI. 3. Asset backed securities regulated by SEBI. 4. Units of Infrastructure Investment Trusts regulated by SEBI. 5. Alternative investment funds (AIF categories I and II) registered with SEBI. | Internationally, institutional investors like PFs consider alternative investments as potential revenue earners due to their benefits as tools of diversification (with low or negative correlation with the other traditional assets in the portfolio), lower volatility and higher risk adjusted returns. Investments in alternative investment funds will help in risk diversification and returns optimisation since the returns of these asset classes are not directly co-related to the returns from traditional asset classes. Any downtrend in other asset classes may be compensated up to some extent by returns generated by these instruments and viceversa. Therefore, the introduction of alternative investment funds and the creation of a separate asset class A (alternate investment) will allow pension funds to diversify their portfolios and hence reduce the risks associated with specific traditional asset classes and also help them in achieving optimum returns. | Section B Other developments I. The Financial Stability and Development Council 3.9 Financial Stability and Development Council (FSDC) held one meeting (15th meeting of FSDC on July 5, 2016) since the publication of the last FSR in June 2016,wherein issues such as rising bank NPAs, developing a robust regulatory framework for various credit guarantee schemes of the Government, comprehensive scheme for identification of systemically important financial institutions (SIFIs) across all sub-sectors of financial sector and possible stress in the financial markets on account of maturity of concessional swaps in 2013 against FCNR deposits were discussed. 3.10 The FSDC sub-committee held one meeting (18th meeting of FSDC-SC) on August 29, 2016, wherein report of Financial Stability Board (FSB) Peer Review of India, report of the Working Group (WG) on Development of Corporate Bond Market in India, proposed Bill on setting up of statutory Financial Data Management Centre (FDMC)15, Minimum Assured Return Scheme (MARS) under National Pension System (NPS) and regulation of spot exchanges were discussed. The sub-committee also reviewed the functioning of the technical groups supporting it and functioning of the state level coordination committees (SLCCs) in various states/ union territories. As decided in the previous subcommittee meeting held in April 2016, the Ministry of Finance (MoF) has set up a working group on issues related to gold, SEBI has formed a committee on the stewardship code and the Reserve Bank has set up an Inter-regulatory working group on Fin Tech and digital banking and another committee on household finances. II. The banking sector Capacity building 3.11 Effective and capable human resources in regulated entities are important for implementing and fulfilling regulatory objectives. The Reserve Bank had constituted a Committee on Capacity Building (July 2014), with the objective of implementing non-legislative recommendations of the Financial Sector Legislative Reforms Commission (FSLRC) relating to capacity building in banks and non-banks, streamlining training interventions and suggesting changes thereto in view of ever increasing challenges in the banking and non-banking sectors. In August 2016, the Reserve Bank issued guidelines on capacity building in banks and AIFIs prescribing adoption of some of the recommendations of the committee. Banks are required to identify specialised areas for certification of the staff manning key responsibilities. To begin with, the banks are required to make acquiring a certification mandatory for: (i) treasury operations – dealers, mid-office operations; (ii) risk management – credit risk, market risk, operational risk, enterprise-wide risk, information security, liquidity risk; (iii) accounting – preparing of financial results, audit function; and (iv) credit management – credit appraisal, rating, monitoring, credit administration. Bank supervision: Concerns and developments Frauds in technology and traditional banking environments 3.12 In the recent past, frauds in the technology environment have accentuated through malware attacks and skimming frauds in ATMs, misuse of SWIFT messages by employees and attacks on the SWIFT messaging system of a bank. Considering the large scale penetration of ATMs in semi-urban and rural areas and a massive addition of new customers under the Jan Dhan scheme with ATM cards, it is of utmost importance that ATMs’ operations are carried out in a completely sanitised manner. While the Reserve Bank has issued caution advices and specific instructions in this regard, banks need to be vigilant. 3.13 The instances of large scale forex remittances in the guise of import advances/payments is another area of supervisory concern. While banks may not have any credit exposures to such parties remitting forex, misuse of banking channels for such remittances is a serious concern, and, therefore, banks need to enhance rigour in their data analytics and reporting structures to aid board level governance. The Reserve Bank has enhanced regulatory and supervisory instructions in this regard and many banks in India have been penalised for violation of instructions issued under Prevention of Money Laundering Act (PMLA) and Foreign Exchange Management Act (FEMA). Similarly, the instances of contravention of Reserve Bank’s instructions on opening of current account and providing non-fund based credit facilities (bill/LCs discounting/guarantees) by banks to constituents who are not their regular borrowers also need to be addressed. Move towards cyber security risk audit of banks 3.14 Recognising the potential impact of major cyber security incidents on the stability of financial system, Reserve Bank established a Cyber Security and IT Examination (CSITE) Cell in 2015. Comprehensive guidelines on “Cyber Security Framework in Banks” covering best practices has been issued in June 2016. IT examinations and thematic studies, independent of financial supervision, are conducted to assess the robustness of banks’ cyber infrastructure and governance practices. Cyber drills are also conducted in collaboration with the Indian Computer Emergency Response Team (CERT-In) to evaluate the cyber security incident response capabilities in banks. Full coverage under risk based supervision (RBS) by the end of the year 3.15 Introduced in 2012-13, supervisory program for assessment of risk and capital (SPARC) has been successfully implemented over three supervisory cycles for the banks operating in India, covering more than 65 per cent of the banking system assets and liabilities. While the newly licensed banks are ab-initio covered under this supervisory program, from 2016-17 supervisory cycle, all scheduled commercial banks (excluding RRBs and Local Area Banks) have been placed under the SPARC framework. III. Implementation of Ind AS 3.16 The Ministry of Corporate Affairs (MCA), Government of India had notified the Companies (Indian Accounting Standards) Rules, 2015 in February 2015. In January 2016, MCA outlined the roadmap for implementing the International Financial Reporting Standards (IFRS) converged Indian Accounting Standards (Ind AS) for banks, non-banking financial companies, select all-India term lending and refinancing institutions and insurance entities. The process of convergence of the current accounting framework in India with IFRS has started with certain categories of corporates transitioning to Ind AS in this financial year. The Reserve Bank has issued directions in February & August 2016 in terms of which all scheduled commercial banks (excluding regional rural banks) and AIFIs shall prepare Ind AS financial statements for accounting periods commencing from April 1, 2018 (with previous year comparatives). 3.17 Insurance companies are also required to prepare Ind AS based financial statements for accounting periods beginning April 1, 2018. IRDAI has constituted an implementation group of accountants, actuaries, industry experts and officials of the Authority with the mandate of examining the implications of implementing Ind AS, addressing implementation issues and facilitating the formulation of operational guidelines to converge with Ind AS in the Indian insurance sector. IV. Payment and settlement systems 3.18 Payment and settlement systems (PSS) as part of the financial market infrastructure (FMI), play a critical role in ensuring an efficient and stable financial system and in the smooth functioning of the overall economy. As mentioned in previous FSRs, India has been keeping pace in adopting international standards and best practices and implementing global regulatory reforms which seek to adequately address the systemic risks associated with FMIs. 3.19 As the regulatory and supervisory authority for payment and settlement systems16 (except those under stock exchanges), the Reserve Bank has adopted a broad approach towards facilitating and encouraging an increasing number of payment transactions, especially large value transactions in electronic (non-cash) modes. The share of electronic transactions in total transactions in volume terms moved up to 84.4 per cent from 74.6 per cent, accounting for more than 95.2 per cent in value terms. While a large proportion of these are on account of RTGS and the Clearing Corporation of Indian Limited (CCIL), the share of retail electronic payments and mobile payments is steadily increasing (Chart 3.2). 3.20 There is a trend of increasing shift towards electronic payment systems, with the usage of card payments (credit cards and debit cards) registering consistent growth (Chart 3.3). 3.21 Recent initiatives towards reducing the size of the cash economy are likely to sharply increase the use of digital money and its equivalents. The Reserve Bank in its ‘Vision 2018’ document reassured that it would take further measures ‘to encourage greater use of electronic payments by all sections of society so as to achieve a “less-cash” society.’ Apart from addressing security concerns, other measures will be required to effect a larger ‘cultural’ shift away from proclivity for cash in the present Indian context. Frictions that create a wedge between electronic modes of transaction and cash not only in terms of ease but also in terms of costs need to be addressed in bringing electronic payment channels closer to cash. V. Fin Tech and Reg Tech 3.22 Rapid developments are taking place in the area of Fin Tech globally. Market players, mainly technology start-ups, as well as regulators and central banks are evolving to the technological innovations in financial services. It is understood that the future of financial regulation, supervision and policymaking lies in using technology and data to improve the speed, quality and comprehensiveness of information in support of targeted, risk-based decision making. Reg Tech can reduce the cost of compliance for financial institutions and increase consumer trust and participation in the system. Regulators across the globe are trying to proactively engage with the tech firms to customise the technological applications to improve the regulatory process. Many jurisdictions have established regulatory sandboxes and innovation hubs for testing of new products/services and providing support/guidance to regulated as well as unregulated entities. Certain advanced jurisdictions have set up “Innovation Accelerators”, which are partnership arrangements between innovators/Fin Tech providers and/or incumbent firms and official sector authorities to ‘accelerate’ growth. Adoption of technology by regulators popularly known as Reg Tech has been discussed in Box 3.2. Box 3.2: Reg Tech The increasing use of computational and network technologies in delivering different types of financial services while striving to protect the integrity of financial data and transactions through advanced applications such as cryptography, block-chain and machine learning (collectively referred to as ‘Fin Tech’) are resulting in a completely new approach to the business of finance. There is a need for all stakeholders including business firms, consumers, policymakers and regulators to understand and adopt the trends and developments in Fin Tech, along with the inherent risks as an essential first step. This has assumed greater significance for the authorities since apart from its potential for improving efficiency and financial inclusion, the fast-paced innovations (for example, virtual currency and P2P lending) have brought risks and concerns about data security and consumer protection on the one hand and the far-reaching potential impact of the effectiveness of monetary policy itself on the other. It may sound paradoxical but after the initial fretting over digital currencies many central banks around the world seem to be examining the feasibility of creating their own digital currencies. While Fin Tech is mainly pushed by the competitive forces brought by the new wave technology start-ups, the changing landscape of regulatory and supervisory reporting, especially coping with jurisdiction-specific and often conflicting or different regulatory frameworks poses additional challenges to financial sector participants as also to regulators. Apart from increasing the cost of compliance for regulated entities, the complexity and information intensive oversight requirements also pose challenges to regulators who look for a needle of wisdom amidst a stack of information. Reg Tech, which is an extension of Fin Tech is the market response to such challenges. IBM’s recent acquisition of Promontory, a leading ‘risk management and regulatory compliance’ consultancy firm whose staff includes former employees of SEC, the Fed and other regulators is one such effort to cater to the Reg Tech market through a man-machine symbiosis – expert human knowledge and the cognitive artificial-intelligence platform. From one perspective, as defined by the Financial Conduct Authority (FCA) of the UK1 Reg Tech can be seen as a part of the universe of Fin Tech, referring to the ‘technologies that may facilitate the delivery of regulatory requirements more efficiently and effectively than existing capabilities.’ However, from a broader perspective, Reg Tech may be seen as representing ‘the next logical evolution of financial services regulation and … offers the potential of continuous monitoring capacity, providing close to real-time insights, through deep learning and artificial intelligence filters, into the functioning of the markets nationally and globally, looking forward to identify problems in advance rather than simply taking enforcement action after the fact2. A report by the Institute of International Finance (IIF)3 suggests that developing Reg Tech solutions will help in processes related to risk data aggregation; modelling, scenario analysis and forecasting; monitoring payment transactions; identifying clients and legal persons; monitoring a financial institution’s internal culture and behaviour; trading in financial markets; and identifying new regulations applicable to financial institutions. Apart from regulatory evolution, as the Fin Tech process has made the finance industry far more vulnerable to cyber-attacks and other types of cyber frauds, Reg Tech will need to be seen as a response to such threats and risks. The automation of processes related to ‘know your customer’ (KYC) and ‘anti-money laundering’ (AML) can be considered examples of basic Reg Tech applications. The scope of Reg Tech is immense because as Fin Tech graduates from digitisation of money to monetisation of data, the regulatory framework, especially macroprudential policy tools, will need to be supported by developments in Reg Tech to address challenges such as data integrity, data sovereignty and algorithm supervision. References: 1. (FCA), UK, ‘Call for Input: Supporting the development and adoption of RegTech.’ (https://www.fca.org.uk/news/news-stories/call-input-supporting-development-and-adoption-regtech). 2. Arner, Douglas W., Jànos Barberis, and Ross P. Buckley (forthcoming), ‘FinTech, RegTech and the Reconceptualisation of Financial Regulation.’ (http://ssrn.com/abstract=2847806). 3. ‘Regtech in financial services: Technology solutions for compliance and reporting’, IIF Report, March 2016 (https://www.iif.com/.../regtech-financial-services-solutions-compliance-and-reporting). 3.23 One of the areas that is fast growing in the digital payments space is prepaid payment instruments (PPI) and it will be inevitable that the new developments come with some consumer protection issues. Recently the Consumer Financial Protection Bureau (CFPB) in the US decided to regulate one of the fastest-growing concerns of finance. Concerns emerged as customers were sometimes unable to access their money and account balances because of ‘technical problems.’ The free float of funds that is available with a PPI issuer is a major attraction for the entities operating in this space. However, it may be subject to misuse, especially if the unutilised funds are subject to forfeiture. In case of most of the advanced jurisdictions, the escheatment clauses are clear that where the unutilised funds as per the extant laws need to be transferred to the state as unclaimed property, the card company will deactivate the card and make available the funds to the owner on request and issue a new card. VI. Evolving insolvency and resolution framework 3.24 A Committee was set up in March 2016 as a follow up of the proposal made in the Union Budget 2016-17, to frame a ‘Code on Resolution of Financial Firms’ for a specialised resolution mechanism to deal with bankruptcy situations in banks, insurance companies and other financial sector entities. The committee has since come out with the draft Financial Resolution and Deposit Insurance (FRDI) Bill17, 2016 for public comments. 3.25 The draft Bill prescribes setting up of a Resolution Corporation (RC), which would help India to broadly adhere to the Financial Stability Board’s Key Attributes (FSB KAs) of Effective Resolution Regimes for Financial Institutions18 by addressing the gaps in the current resolution mechanism in India in terms of legal framework, resolution tools, liquidation, coverage of entities, cross border cooperation and oversight framework. The proposed RC would subsume the role of DICGC which currently undertakes only the ‘pay box’ function i.e., reimbursement of insured amount to the depositors of failed banks. This framework aims to position RC to play a vital role in maintaining financial stability. The other salient features of FRDI Bill, 2016 are given in Box 3.3. Box: 3.3: Financial Resolution and Deposit Insurance (FRDI) Bill 2016 1. Composition of the Board: The board of the RC would consist of eleven members headed by Chairperson having five ex-officio members representing Ministry of Finance, RBI, SEBI, IRDAI and PFRDA along with upto three whole time members and two independent members to be appointed by the Central Government. 2. Scope: The proposed RC intends to cover the financial sector entities viz., banks, insurance companies, non banking financial companies, holding companies, financial market infrastructures, systemically important financial institutions (SIFIs) and any other entity which may be notified by the Central Government for the purpose of resolution while confining the deposit insurance only to banks. The entities that will be covered under RC have been classified under two categories viz., Covered Service Providers (CSPs-all entities as mentioned above) for the purpose of resolution and Insured Service Providers (ISPs – only banks) for the purpose of Deposit Insurance. 3. Powers and functions of RC: The RC would provide Deposit Insurance, assign risk to viability of a CSP, inspect a CSP, resolve a CSP and act as liquidator for a CSP apart from any other operations as mentioned in the Bill. 4. Powers of Investigation, Search and Seizure and Inspections: The RC would have substantial powers to conduct searches and seizures and investigations of CSP when the CSP is classified as imminent or critical by the appropriate regulator or RC. RC has the power of independent inspection when there is difference of opinion with appropriate regulator in classifying the entity as material. It can also inspect an entity on continuous basis in imminent stage. 5. Defining Risk to Viability: Based on certain parameters, a five-stage “risk to viability framework” for CSPs, viz., (i) low, (ii) moderate, (iii) material, (iv) imminent, and (v) critical has been proposed. The Board shall, in consultation with the appropriate Regulator, specify objective criteria for classification of CSP into any of the five categories. The first two stages (“low risk to viability” and “moderate risk to viability”) would be such that the CSP’s probability of failure is below acceptable level. At these stages, the RC would have no powers of investigation, search or seizure on the CSPs. The only exceptions are SIFIs, which would submit “Resolution Plans” irrespective of their financial situation. This plan will help in devising optimal resolution strategies for these firms. Also, SIFIs may at any point be jointly inspected by the respective regulator(s) and the RC. 6. Material risk-to-viability: The CSPs categorised as material risk-to-viability would be more risk averse than those of the low and moderate risk-to-viability. This category signifies the first breach of threshold of acceptable probability of failure along with breach of prudential regulation requirements. When classified as ‘material risk-to-viability’, a CSP has to prepare a Resolution Plan and send to RC. The CSP also has to prepare a Restoration Plan to send to regulators. 7. Imminent risk-to-viability: The stage of the CSP is well above acceptable probability of failure. A CSP can also be categorised under this type of risk-toviability if it fails to submit/implement resolution plan or restoration plan or if it is determined that there has been a major fraud in the firm that significantly affects the viability of CSP. 8. Critical risk-to-viability: At this stage, the classification is done through an order in writing. As soon as this is done, the RC would become the Administrator for the CSP. 9. Resolution tools: Four major resolution tools are envisaged in the Bill which will be used after the CSP is categorised as “critical risk to viability”. They are: (i) Sale to or merger with another institution; (ii) Transfer of assets and liabilities to a Bridge Service Provider; (iii) Bail-in and (iv) Liquidation. These resolution tools would help to extend the mandate of the RC beyond ‘Pay box’ into ‘Pay box plus’. Liquidation option should be considered only when the other resolution tools are not optimal. Definite timelines have been prescribed under resolution mechanism. VII. Capital markets Redemption of mutual funds (MFs) 3.26 The assets under management (AUM) of the mutual fund industry increased by 33 per cent to ₹15,801 billion in September 2016 from ₹11,873 billion in September 2015 (Chart 3.4). However, trends in redemptions, which closely followed the total fresh mobilisations during the period April 2015 – July 2016 point towards risks to market equilibrium in the event of sudden and sizeable redemption pressures.  3.27 With a view to avoiding a systemic crisis from high redemptions, the AMCs are authorised to impose provisional restrictions on redemption in a specific scheme, after obtaining approval from the Board of Directors of the Asset Management Company (AMC) and the Trustees. The earlier guidelines in respect of restrictions on redemption were general in nature and did not specifically spell out the circumstances in which restriction on redemption was to be applied, leading to discretionary practices in the industry. In order to bring in more clarity while simultaneously protecting the interests of the investors, SEBI in May 2016 issued guidelines on circumstances under which AMCs can restrict the redemptions. Restriction may be imposed when there are circumstances leading to a systemic crisis or event that severely constricts market liquidity or the efficient functioning of markets such as (i) Liquidity issues – when market at large becomes illiquid affecting almost all securities rather than any issuer specific security, (ii)Market failures, exchange closures – when markets are affected by unexpected events which impact the functioning of exchanges or the regular course of transactions and (iii) Operational issues – when exceptional circumstances are caused by force majeure, unpredictable operational problems and technical failures. It also, inter-alia, prescribed that redemption requests up to ₹0.2 million shall not be subject to such restriction and restriction on redemption may be imposed for a specified period of time not exceeding 10 working days in any 90 days’ period. The possibility that an investor’s right to redeem may be restricted in such exceptional circumstances, needs to be disclosed prominently in scheme related documents. Investment through PNs/ODIs 3.28 For increasing transparency and to remove any possibility of misuse of investments though Offshore Derivative Instruments (ODIs)/Participatory Notes (PNs), it is essential to know more about the source and intent of the investments entering the country through this route. SEBI has been, from time to time, taking appropriate measures to effectively regulate the issuance of ODIs/PNs. Continuing the same trend SEBI has recently taken a few steps to streamline the process of issuance and reporting of ODIs, duly taking in-to consideration the recommendations of Special Investigation Team (SIT) on black money. 3.29 In August 2007 the total value of PNs as a share of Asset Under Custody (AUC) of foreign institutional investors (FIIs) was about 51 per cent which came down to around 20 per cent in December 2008; further it remained under 20 per cent and gradually came down to 16.5 per cent in January 2011 and subsequently to 8.8 per cent in October 2016. This clearly indicates the impact of the consistent policy initiatives taken by SEBI over the years including the recent one taken in the form of circular dated June 10, 2016 and amendment of SEBI (Foreign Portfolio Investor) Regulations, 2014. This shows that with the increasing transparency requirements, the chances of routing of black money though this route is insignificant. VIII. The insurance sector General Insurance 3.30 Occurrence of natural calamities/disasters/ contagious diseases in India at an increased frequency is a matter of concern. Given low level of awareness amongst the public regarding general insurance and lower penetration of non-life insurance cover for small businesses, such calamities may give rise to systemic risk. Insurance Pools-Terrorism Pool & Nuclear Insurance Pool 3.31 Insurance pools provide protection to insurance companies and strengthen the financial stability by providing cushion against large number of claims arising from catastrophic risks. In the Indian context, two such important pools were formed where international reinsurance were not available. 3.32 The Indian Market Terrorism Risk Insurance Pool was formed as an initiative by all the non-life insurance companies in India in April 2002, after terrorism cover was withdrawn by international reinsurers post 9/11. The Pool is administered by GIC Re and is applicable to insurance of terrorism risk covered under property insurance policies. With effect from April 1, 2014, the limit of indemnity per location has been enhanced to ₹15 billion from the previous level of ₹10 billion and the premium rates have been revised downward. 3.33 Nuclear risks are normally excluded from the traditional form of insurance globally and such requirements are met by the formation of nuclear pools. Nuclear operators are required to maintain an insurance coverage/financial security of ₹15 billion as stipulated under the Civil Liability for Nuclear Damage Act, 2010. Since India did not have any pool for nuclear risk cover, GIC Re, the Indian Reinsurer with other Indian general insurance companies formed the nuclear pool to meet the said requirements, in December 2015. The pool is administered by GIC Re. Health Insurance 3.34 The guidelines on product filing in health insurance business and guidelines on standardisation in health insurance were notified by IRDAI on July 29, 2016, which, inter-alia, cover additional norms for protection of interests of policyholders. These norms, inter-alia, prescribe the insurers to endeavour to design their underwriting policy to provide cover to sub-standard lives also. Denial of proposal shall be the last resort. However, denial of claims on account of pre-existing diseases remains a major concern. Trade credit insurance 3.35 Given the backdrop of enhanced need for trade credit insurance in the economy, especially in the MSME sector, IRDAI has issued revised guidelines on ‘trade credit insurance’ in March 2016. The guidelines intend to enhance the scope of trade credit business, and has cautiously inbuilt certain parameters to avoid misuse of the scope with restrictions like (i) insurer to mandatorily assess the credit risk of any buyer who contributes more than 2 per cent of the total turnover of the policyholder, (ii) trade credit policy not to grant an indemnity of more than 85 per cent of the trade receivables from each buyer, and (iii) aggregate net retentions of the insurer for trade credit insurance not to exceed 5 per cent of net-worth. IX. The pension sector Growth under National Pension System 3.36 The National Pension System (NPS) continued to gain traction in terms of the number of subscribers as well as assets under management (AUM). The total number of subscribers increased from 8.75 million in March 2015 to 12.12 million in March 2016 and stood at 13.77 million in October 2016. AUM increased from ₹809 billion in March 2015 to ₹1,177 billion in March 2016 and stood at ₹1,539 billion in October 2016. Increase in the coverage of the unorganised sector through the Atal Pension Yojana 3.37 A large proportion of the workforce (88 per cent) in India is engaged in the unorganised sector having tenuous labour market links, seasonal employment and low levels of income hence posing huge challenges for pension inclusion. The Finance Minister announced the Atal Pension Yojana (APY) in his Budget Speech for 2015-16 as a part of trinity of the Prime Minister’s financial inclusion schemes – the Pradhan Mantri Jan Dhan Yojana (PMJDY) and the Pradhan Mantri Jeevan Suraksha Bima Yojana (PMJSBY). Under APY, subscribers receive a fixed minimum pension of ₹1,000 to ₹5,000 per month at the age of 60 years, depending on their contribution, which itself varies according to the age when joining APY. The benefit of minimum pension will be guaranteed by the government. In case subscribers join before end-March 2016, the central government will co-contribute 50 per cent of the subscribers’ contribution or ₹1,000 per annum, whichever is lower, for a period of five years (that is, from 2015-16 to 2019-20), to each eligible subscriber’s account who is not a member of any statutory social security scheme and who is not an income tax payer. As on October 22, 2016, 394 banks had registered 36.15 lakh subscribers with a total AUM of ₹12.4 billion. X. Consumer protection 3.38 While risks to consumers from phishing and vishing remain high, instances of cheating where unregulated entities posing themselves to be regulated ones, were noticed. It is essential that public perceptions of regulated entities with different levels and degrees of regulation are retained and consumers are not misled into believing that they all belong to the same category.19 3.39 To combat the risks in the form of collective investment schemes, multi-level marketing and deemed public issues20 without the necessary regulatory approval, SLCCs21 have launched the webportal ‘Sachet’ which enables public access to information regarding entities that are allowed to accept deposits and lodge complaints. The portal also facilitates sharing of information regarding illegal acceptance of deposits by unscrupulous entities. However, such activities appear to have abated as seen in a decline in the number of interim and final orders passed by SEBI to such entities directing them to stop collecting funds from investors under unauthorised schemes22 (Table 3.2). Further the receipt of number of complaints by SEBI regarding unauthorised money collection activities have also declined over the period of time. | Table 3.2: Interim and final orders passed by SEBI | | Sl. No. | F.Y | Interim Orders | Final Orders | | No. of Orders (CIS) | No. of Orders (DPI) | Total | No. of Orders (CIS) | No. of Orders (DPI) | Total | | 1 | 2014-15 | 51 | 108# | 159 | 14 | 9 | 23 | | 2 | 2015-16 | 13 | 90 | 103 | 34 | 80 | 114 | | 3 | 2016-17* | 0 | 6 | 6 | 8 | 24 | 32 | | Total | | 64 | 204 | 268 | 56 | 113 | 169 | * Till September 2016 CIS – Collective Investment Scheme; DPI – Deemed Public Issue

# Includes 5 interim orders passed in 2013-14.

Source: SEBI |

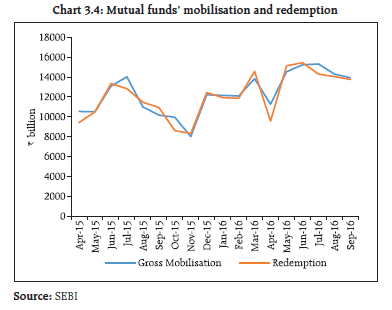

|