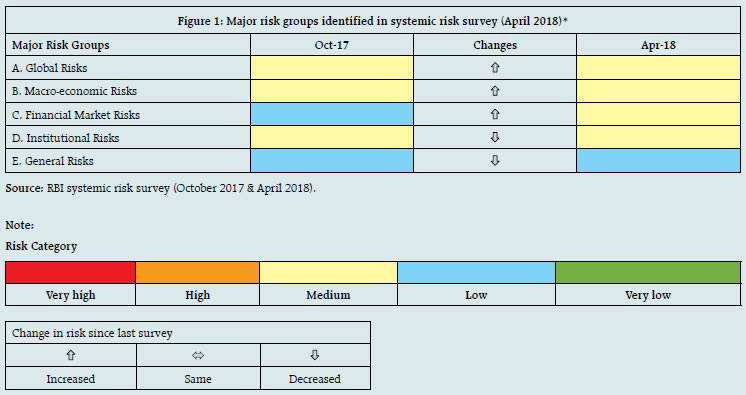

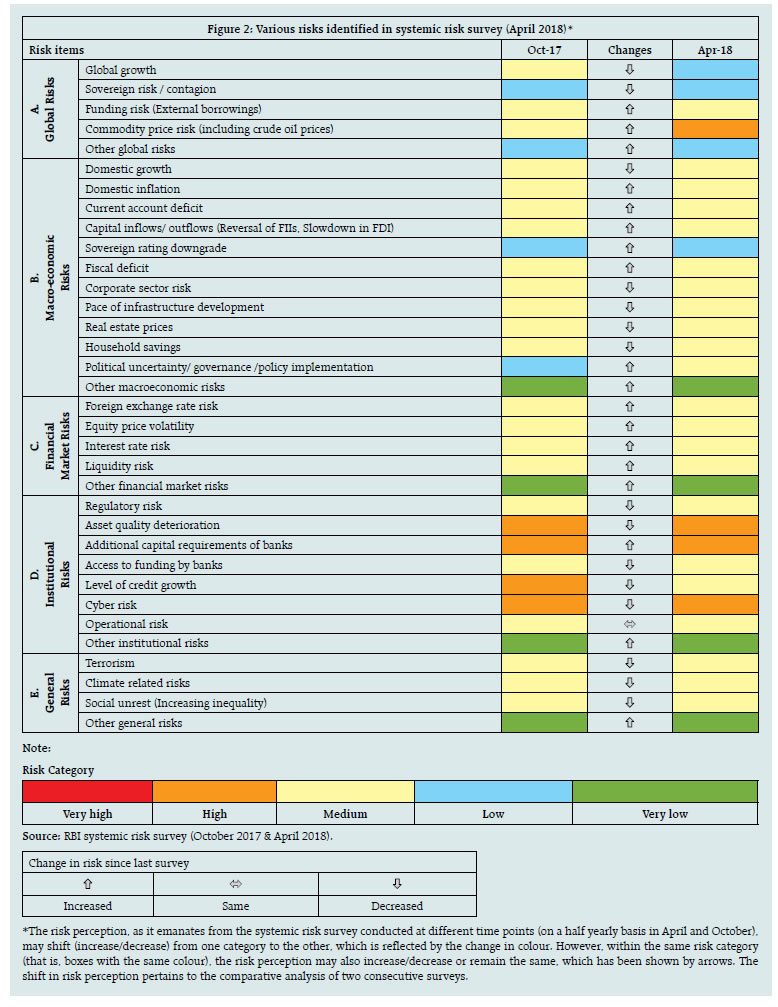

The systemic risk survey (SRS), the fourteenth in the series, was conducted during April-May 2018 to capture the perceptions of experts on the major risks presently faced by the financial system. The experts include market participants at financial intermediaries, academicians and rating agencies. According to the survey results, global risks, risk perception on macroeconomic conditions and institutional positions as well as market risks are perceived as medium risks affecting the financial system. Other general risk, however, remain to be perceived in low risk category (Figure 1). Within global risks, the risk on account of commodity prices (including crude oil prices) was categorised as high risk. Within the macroeconomic risks group, risk on account of political uncertainty/policy implementation moved from low to medium risk category. Risks on account of domestic growth, domestic inflation, current account deficit, capital flows, fiscal deficit, corporate sector, pace of infrastructure development, real estate prices and household savings continued to be in medium risk category in the current survey. Equity price volatility, interest rate risk and liquidity risk also continued to be in medium risk category within financial market risks. Foreign exchange risk, though still in the medium risk category, saw a substantial rise in the risk score in the current survey. Among the institutional risks, the asset quality deterioration of banks, risk on account of additional capital requirement and cyber risk continued to be perceived as high risk factors (Figure 2).

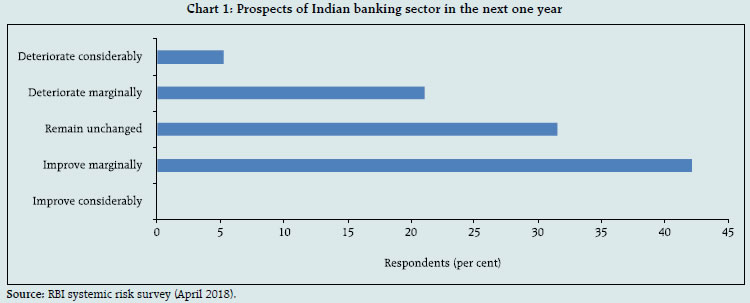

Geopolitical risks and the prospects of trade war turning into reality continued to be on the watch list of the participants of the survey. Participants opined that rise in commodity prices including crude oil price will impact inflation, current account deficit, as well as fiscal deficit and could impact domestic financial stability. Market participants expect increase in the volatility due to upcoming general elections and rise in FED rate. About 40 per cent of the respondents feel that the prospects of Indian banking sector are going to improve marginally in the next one year, while the other respondents still feel that the continuous rise in NPAs and faltering governance standards in banks continue to be a cause of concern (Chart 1).  Majority of the participants in the current round of survey expect possibility of occurrence of a high impact event in the global financial system and the Indian financial system in the short term (upto 1 year) as well as in the medium term (1 to 3 years) to be medium. There was a significant decrease in the respondents in the current survey who were fairly confident of the stability of the global financial system (Chart 2). Majority of the respondents were of the view that the demand for credit in the next three months would ‘increase marginally’ and average credit quality could ‘improve marginally’ in the next three months (Chart 3). |