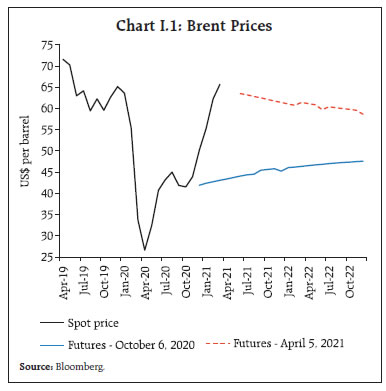

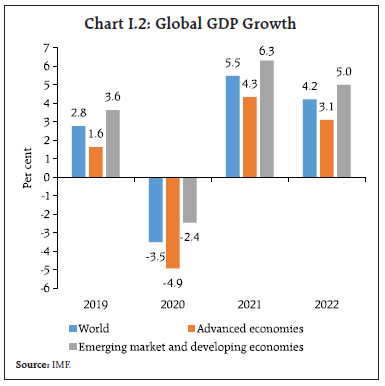

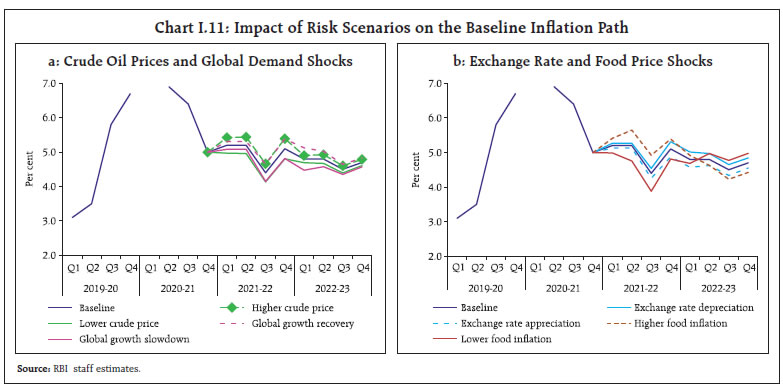

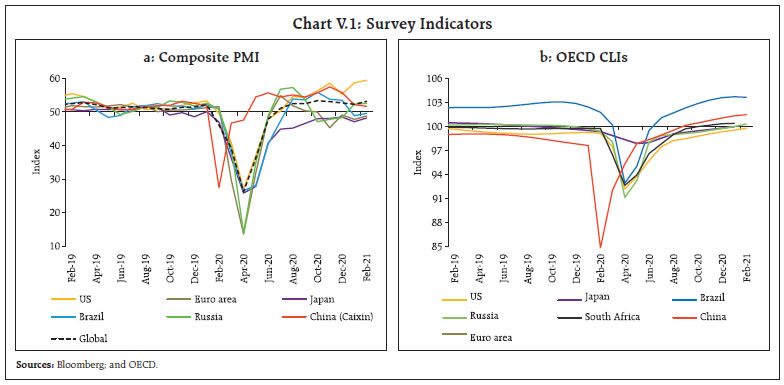

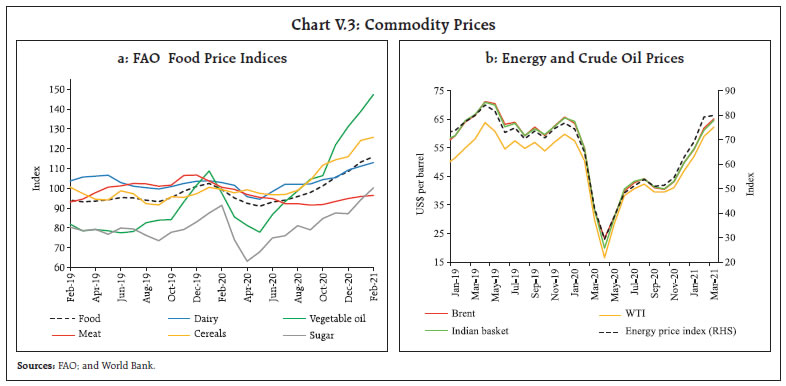

| I. Macroeconomic Outlook The rebound from the COVID-19 induced slump has been sharper than anticipated and economic activity is expected to rebound strongly in 2021-22. Headline consumer price index (CPI) inflation receded into the tolerance band beginning December 2020. Core inflation pressures remain elevated, reflecting pass-through from higher crude oil and non-oil commodity prices, high fuel and other taxes post-COVID and increased operating costs. The evolving COVID-19 trajectory and progress on vaccination remain the key drivers of economic activity and inflation, globally and in India. Section 45-ZA of the RBI Act, 1934 requires that the Central Government shall, in consultation with the Reserve Bank of India (RBI), determine the inflation target in terms of consumer price index (CPI), once in every five years. Accordingly, in a notification on March 31, 2021, the Central Government, in consultation with the RBI, retained the inflation target at 4 per cent (with the upper tolerance level of 6 per cent and the lower tolerance level of 2 per cent) for the 5-year period April 1, 2021 to March 31, 2026. The experience with successfully maintaining price stability and the gains in credibility for monetary policy since the institution of the inflation targeting framework in 2016 would be reinforced by the retention of the target and the tolerance band.1 The experience during the COVID-19 period has testified to the flexibility of the framework to respond to sharp growth-inflation trade-offs and extreme supply-side shocks. I.1 Key Developments since the October 2020 MPR Since the release of the Monetary Policy Report (MPR) in October 2020, domestic economic activity has turned out to be better than anticipated on the back of a turnaround in gross fixed capital formation and a much shallower contraction in private consumption than in the preceding quarters of the financial year. The global economy is pulling out of the loss of momentum in Q4:2020, driven by multiple vaccine approvals, the launch of inoculation drives in many countries and the extension of monetary and fiscal stimuli. On the other hand, new mutants of the COVID-19 virus, second/third waves of infections, renewed lockdowns in many countries and uneven access to vaccines across countries continue to weigh on the outlook. The resurgence of commodity price inflation, supported by abundant global liquidity, has fuelled reflation trade in global financial markets. Despite the promise of continued accommodative monetary policies by central banks, bond yields have firmed up from very low levels, spurred by inflation concerns and expectations of stronger growth. Amidst stretched valuations, equity prices have become sensitive to the hardening of yields. In turn, exchange rates have become volatile, with capital outflows from emerging economies in early March interrupting their earlier ebullience on risk-on sentiments. Crude oil prices jumped sharply on production cuts by the Organization of the Petroleum Exporting Countries (OPEC) plus and on anticipation of stronger demand. Non-oil commodity prices have risen substantially across the board, putting upward pressures on inflation in commodity importing countries. Gold prices eased from the highs reached in August 2020 on a stronger US dollar and expectations of economic recovery. While inflation is expected to remain subdued in advanced economies (AEs) and most of the emerging market economies (EMEs) on account of negative output gaps, the large fiscal and monetary stimuli and elevated commodity prices have raised inflation concerns over longer horizons in advanced economies and in the nearer-term in the case of EMEs. Turning to the domestic economy, the gross domestic product (GDP) shrugged off the contractions of preceding quarters and moved into expansion zone in Q3:2020-21 (+ 0.4 per cent, year-on-year). High frequency indicators point to the growth momentum gaining strength in Q4 although the surge in COVID-19 infections in a few states in March 2021 imparts uncertainty to the assessment. The outlook for the agriculture sector remains bright, with higher rabi sowing, above normal north-east monsoon and adequate reservoir levels. Inflation receded into the tolerance band beginning December 2020 after breaching the upper threshold of 6 per cent for six consecutive months (June-November 2020). The late winter easing of vegetable prices that caused this softening has dissipated, however. In its February 2021 print, headline inflation firmed up again, with upside pressures getting generalised across constituents of core inflation. Monetary Policy Committee: October 2020-March 2021 During October 2020-March 2021, the Monetary Policy Committee (MPC) met thrice. In the October 2020 meeting, the MPC noted that the revival of the economy from the unprecedented COVID-19 pandemic assumed the highest priority in the conduct of monetary policy. High inflation was seen as easing with the unlocking of the economy, restoration of supply chains and normalisation of activity. Hence, the MPC decided to look through the inflation spike and unanimously voted to keep the policy repo rate unchanged. It also voted to continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remained within the target going forward. In the run up to the December 2020 meeting, CPI inflation had increased to 7.6 per cent in October 2020 with food inflation surging to double digits across protein-rich items, edible oils, vegetables and spices on multiple supply shocks. Core inflation had remained sticky and was seen to firm up as economic activity normalised and demand picked up. At the same time, with the signs of economic recovery being far from broad-based and still dependent on sustained policy support, the MPC decided to maintain status quo on the policy rate and continue with the accommodative stance set out in the October resolution. By the time the MPC met in February 2021, CPI inflation had declined to 4.6 per cent in December 2020 on the back of a larger than anticipated deflation in vegetable prices. The MPC noted the sharp correction in food prices but was concerned that some pressures persisted, and core inflation remained elevated. As the recovery was still to gather firm traction and continued policy support remained crucial, the MPC unanimously decided to keep the policy repo rate unchanged and maintain its accommodative stance. The MPC’s voting pattern reflects the individual members’ assessments, expectations and policy preferences (Table I.1). The MPC’s unanimous vote on the policy rate in all the three meetings during October 2020-March 2021 was a reflection of the unprecedented pandemic and an unambiguous consensus on continued policy support. Macroeconomic Outlook Chapters II and III analyse macroeconomic developments during October 2020-March 2021. Turning to the outlook, the evolution of key macroeconomic and financial variables over the past six months warrants revisions in the baseline assumptions (Table I.2). | Table I.1 Monetary Policy Committees and Voting Patterns | | Country | Policy Meetings: October 2020 - March 2021 | | Total Meetings | Meetings with Full Consensus | Meetings without Full Consensus | | Brazil | 4 | 4 | 0 | | Chile | 4 | 4 | 0 | | Colombia | 5 | 3 | 2 | | Czech Republic | 4 | 4 | 0 | | Hungary | 5 | 5 | 0 | | India | 3 | 3 | 0 | | Israel | 4 | 0 | 4 | | Japan | 4 | 0 | 4 | | South Africa | 3 | 1 | 2 | | Sweden | 2 | 2 | 0 | | Thailand | 4 | 4 | 0 | | UK | 4 | 4 | 0 | | US | 4 | 4 | 0 | | Sources: Central bank websites. | First, global crude oil prices have hardened notably since November 2020 on the back of production cuts by the OPEC and non-OPEC allies (OPEC plus) and expected revival in demand with vaccine rollouts. Reflecting these developments as well as the attack on Saudi Arabia’s oil facilities, Brent crude crossed US$ 70 per barrel in early March. Prices, however, corrected to around US$ 65 in the second half of March over concerns of demand faltering on rising COVID-19 infections and increase in crude stockpiles. Taking into account these developments, crude prices (Indian basket) are assumed at US$ 64.6 per barrel for 2021-22 in the baseline, 58 per cent above the October MPR baseline for 2020-21 (Chart I.1). Second, the nominal exchange rate (the Indian rupee or INR vis-à-vis the US dollar) has moved in a range of INR 72-75 per US dollar since October 2020. The INR remained under depreciating pressure till mid-November 2020 due to COVID-related uncertainty, risk aversion and capital outflows. Subsequently, the INR appreciated, riding on the domestic recovery gaining traction, decline in the number of new infections, vaccine rollout, and the measures announced in the Union Budget 2021-22 to revive the economy. The INR depreciated sharply in late February on elevated global financial market volatility following the spike in sovereign bond yields in the US and other major AEs. Taking these developments into account, the exchange rate is assumed at INR 72.6 per US dollar for 2021-22 in the baseline. | Table I.2: Baseline Assumptions for Projections | | Indicator | MPR October 2020 | MPR April 2021 | | Crude oil (Indian basket) | US$ 40.9 per barrel during H2:2020-21 | US$ 64.6 per barrel during 2021-22 | | Exchange rate | ₹ 73.6/US$ during H2:2020-21 | ₹ 72.6/US$ during 2021-22 | | Monsoon | 9 per cent above long period average for 2020 | Normal for 2021 | | Global growth | (-) 4.9 per cent in 2020

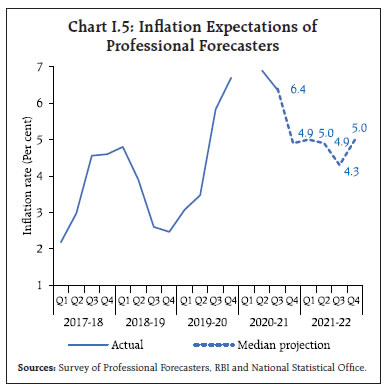

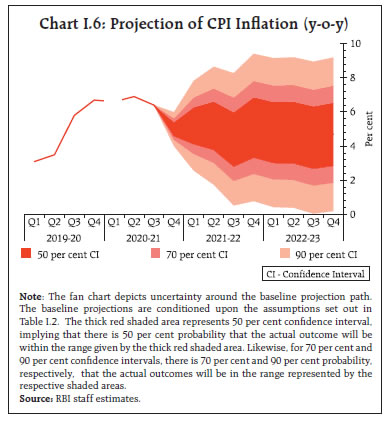

5.4 per cent in 2021 | 5.5 per cent in 2021

4.2 per cent in 2022 | | Fiscal deficit (per cent of GDP) | Given the Covid-19 impact on activity, revenues, and expenditures and factoring in the additional borrowings announced, fiscal deficits are expected to be significantly higher | To remain within BE 2021-22

Centre: 6.8

Combined: 10.8 | | Domestic macroeconomic/ structural policies during the forecast period | No major change | No major change | Notes: 1. The Indian basket of crude oil represents a derived numeraire comprising sour grade (Oman and Dubai average) and sweet grade (Brent) crude oil.

2. The exchange rate path assumed here is for the purpose of generating the baseline projections and does not indicate any ‘view’ on the level of the exchange rate. The Reserve Bank is guided by the objective of containing excess volatility in the foreign exchange market and not by any specific level of and/or band around the exchange rate.

3. BE: Budget estimates.

4. Combined fiscal deficit refers to that of the Centre and States taken together.

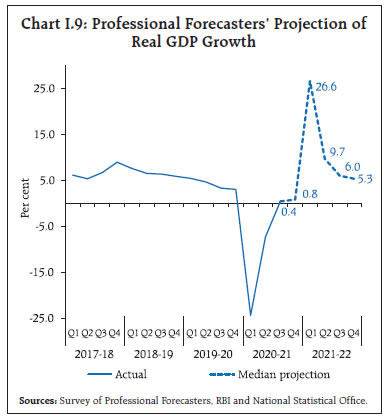

Sources: RBI estimates; Budget documents; and IMF. |  Third, global economic activity has improved relative to the outlook in October 2020 with vaccine rollouts and easing of lockdown restrictions, although it remains uneven across countries and sectors. The International Monetary Fund (IMF) in its January 2021 World Economic Outlook (WEO) update projected the global economy to expand by 5.5 per cent in 2021 (Chart I.2); the outlook remains heavily contingent upon the progress with COVID-19 containment measures and the scale and speed of the vaccination programme. The World Trade Organization’s (WTO) trade barometers suggest a moderation in global merchandise and services trade volumes from the marked improvement in Q4:2020. I.2 The Outlook for Inflation After breaching the upper tolerance threshold of 6.0 per cent for six consecutive months (June-November 2020), CPI inflation fell in December 2020 and eased further in January 2021 to 4.1 per cent on the back of a sharp correction in vegetable prices and softening of cereal prices. It rebounded to 5.0 per cent in February, however, driven primarily by base effects. Core inflation pressures remained elevated, with inflation excluding food and fuel at 6.0 per cent in February reflecting pass-through to retail prices from higher crude oil and non-oil commodity prices, high fuel and other taxes post-COVID and increased operating costs (Chapter II). Looking ahead, three months and one year ahead median inflation expectations of urban households rose by 80 basis points (bps) and 10 bps, respectively in the March 2021 round of the Reserve Bank’s survey2 in tandem with higher food and oil prices. The proportion of respondents expecting the general price level to increase by more than the current rate also increased for both three months and one year ahead horizons vis-à-vis the previous round (Chart I.3).  Manufacturing firms polled in the January-March 2021 round of the Reserve Bank’s industrial outlook survey3 expected further input cost pressures from raw materials in Q1:2021-22; moreover, positive sentiments on profit margins rose on the back of higher selling prices, suggesting a return of pricing power (Chart I.4). The IHS Markit’s purchasing managers’ index (PMI) survey for the manufacturing sector also reported strong increase in input prices in March 2021 along with higher output prices; for the services sector, input cost inflation was at an eight-year high while selling prices remained stable in February, reflecting efforts to boost sales. Professional forecasters surveyed4 by the Reserve Bank in March 2021 expected CPI inflation to ease from 4.9-5.0 per cent in H1:2021-22 to 4.3 per cent in Q3 and revert to 5.0 per cent in Q4 (Chart I.5). Taking into account the initial conditions, signals from forward-looking surveys and estimates from structural and other time-series models, CPI inflation is projected to average 5.0 per cent in Q4:2020-21, 5.2 per cent in Q1:2021-22 and Q2, 4.4 per cent in Q3, and 5.1 per cent in Q4, with risks broadly balanced (Chart I.6). The 50 per cent and the 70 per cent confidence intervals for headline inflation in Q4:2021-22 are 3.3-6.9 per cent and 2.4-7.8 per cent, respectively.   For 2022-23, assuming a normalisation of supply chains on the back of vaccine rollout, a normal monsoon and no major exogenous or policy shocks, structural model (Box I.1) estimates indicate that inflation will move in a range of 4.5-4.8 per cent. The 50 per cent and the 70 per cent confidence intervals for Q4:2022-23 are 2.9-6.5 per cent and 1.9-7.5 per cent, respectively. There are a number of upside and downside risks to the baseline inflation forecasts. The major upside risks include supply chain disruptions persisting for a longer period, rise in global crude oil and other commodity prices beyond what is currently in the baseline, and stronger pass-through of input costs amidst improvement in demand conditions and return of pricing power. Persistent structural demand-supply imbalances in key food items such as pulses, edible oils and fats, and eggs, meat and fish could also keep inflation elevated. The downside risks are mostly associated with a weaker than anticipated global and domestic demand in the case of another wave of infections and new mutants of the virus, fall in crude oil prices on weak demand and an early normalisation of supply chains. Prospects of a good rabi crop on top of a bumper kharif harvest in 2020-21 and effective supply management could keep food prices softer than in the baseline. I.3 The Outlook for Growth The rebound from the COVID-19 induced slump has been sharper than anticipated. Real GDP growth turned positive in Q3:2020-21 and a further strengthening is expected to have occurred in Q4:2020-21. Going forward, rural demand is likely to remain resilient on good prospects for the agriculture sector. Urban demand and demand for contact-intensive services is also expected to strengthen with the spread of vaccination. The fiscal stimulus under AtmaNirbhar 2.0 and 3.0 schemes and increased capital outlays and the investment-enhancing proposals in the Union Budget 2021-22 will likely accelerate public investment and crowd-in private investment. While the domestic financial conditions are expected to remain supportive in view of the guidance from RBI that systemic liquidity would continue to remain comfortable over the ensuing year, the risks of spillovers from volatility in global financial markets remain elevated. Box I.1: Quarterly Projection Model 2.0 The Quarterly Projection Model (QPM) in the RBI’s Forecast and Policy Analysis System (FPAS) is the workhorse model for generating medium term projections and undertaking policy scenario analysis, consistent with the central bank’s mandate under the flexible inflation targeting (FIT) framework (Benes et al., 2016). The QPM is a forward-looking, open economy, calibrated, new-Keynesian gap model, and incorporates specific characteristics of the Indian economy. With a view to enriching the model’s analytics and to capture monetary-fiscal-external-real sector interactions more comprehensively, the model structure has been expanded and the parameters of the QPM recalibrated, taking into account pre-COVID period data (up to Q4:2019) and latest empirical findings. In terms of its structure, the augmented QPM model (QPM 2.0) incorporates: a) fiscal-monetary dynamics, b) disaggregated fuel pricing (oil price, exchange rate and fuel taxes) and c) balance of payments and exchange rate interactions. The fiscal block in QPM 2.0 decomposes the primary deficit into structural (cyclically adjusted) and cyclical components, with shocks to the structural component impacting inflation through aggregate demand and country risk premia. The monetary policy stance affects the fiscal position through the interest rate channel (Escolano, 2010). The fuel block incorporates India’s complex system of pricing – items like petrol and diesel are priced on the basis of international oil prices, exchange rate and fuel taxes (excise duty and value added tax (VAT)); liquified petroleum gas (LPG) and kerosene prices are market determined but with lagged pass-through; and prices of electricity are administered by state governments. The cost-push implications are also incorporated in the enhanced aggregate supply block. Finally, the balance of payments module incorporates determinants of current and capital accounts and their interaction with the exchange rate management, guided by the objective of containing excess volatility in the foreign exchange market. This recognises the costs associated with spurts in volatility in the exchange rate (e.g., balance-sheet effects, dynamic Dutch disease) due to sudden surges or reversals in capital flows (Ghosh et al., 2016). The model properties of these features can be best represented through impulse response functions which trace out the impact on key macroeconomic variables in response to shocks. First, an expansionary structural fiscal shock contributes to demand pressures and creates a positive output gap. Increasing debt could contribute to depreciation of the currency through elevated country risk premia. The positive output gap and currency depreciation together lead to higher inflation, warranting monetary policy action (Chart I.1.1a). On the other hand, if the fiscal deficit shock is cyclical, it has a modest impact on inflation. Second, an increase in fuel taxes feeds into higher fuel prices and ex-food fuel inflation through the cost-push channel. Headline inflation goes up by 25 bps in response to a fuel tax increase of ₹10 per litre (Chart I.1.1b). Inflation expectations edge higher and remain entrenched, if tax reversals do not happen. Demand conditions also remain subdued for a longer period. Finally, the impact of capital flows depends, inter alia, on the RBI’s decision to intervene and sterilise. In case of a capital outflow shock of one percentage point (of nominal GDP) and assuming the RBI intervenes and sterilises 70 per cent of these capital outflows, the reserves will deplete by 0.7 percentage points of nominal GDP. The exchange rate will depreciate, inducing inflationary pressure (Chart I.1.1c). In the case of no intervention, the exchange rate depreciation will be relatively higher. A historical decomposition of the shocks suggests that the FIT framework helped in anchoring inflation expectations during 2016-20 leading to lower headline as well as core inflation. The disinflation during the post-FIT period was also supported by favourable supply shocks, both food and fuel, benign external factors and prudent fiscal policy (Chart I.1.2). References: Benes, J., K. Clinton, A. George, P. Gupta, J. John, O. Kamenik, D. Laxton, P. Mitra, G. Nadhanael, R. Portillo, H. Wang, and F. Zhang (2016), “Quarterly Projection Model for India: Key Elements and Properties”, RBI Working Paper Series No. 8. Ghosh, A. R., J. D. Ostry, and M. Chamon (2016), “Two Targets, Two Instruments: Monetary and Exchange Rate Policies in Emerging Market Economies”, Journal of International Money and Finance, 60, 172-196. Escolano, M. J. (2010), “A Practical Guide to Public Debt Dynamics, Fiscal Sustainability, and Cyclical Adjustment of Budgetary Aggregates”, International Monetary Fund. | Turning to the forward-looking surveys, consumer confidence5 for the year ahead dipped, although it was still in the optimistic zone, in the March 2021 round, driven by lower expectations on the general economic situation, the employment scenario and income conditions (Chart I.7). Sentiments in the manufacturing sector for the quarter ahead strengthened further in the January-March 2021 round of the Reserve Bank’s industrial outlook survey, reflecting optimism on production, order books, capacity utilisation, employment conditions and the overall business situation (Chart I.8). Surveys by other agencies also indicate optimism on future business expectations (Table I.3). According to the purchasing managers’ survey for March 2021, the one year ahead business expectations of firms in the manufacturing sector exhibit confidence; optimism of firms in the services sector strengthened to a one-year high in February. Professional forecasters polled in the March 2021 round of the Reserve Bank’s survey expected a sharp uptick in real GDP growth in Q1:2021-22, driven by base effects before tapering in subsequent quarters (Chart I.9 and Table I.4).

| Table I.3: Business Expectations Surveys | | Item | NCAER Business Confidence Index (February 2021) | FICCI Overall Business Confidence Index (February 2021) | Dun and Bradstreet Composite Business Optimism Index (January- March 2021) | CII Business Confidence Index (March 2021) | | Current level of the index | 84.8 | 74.2 | 79.9 | 68.7 | | Index as per previous survey | 65.5 | 70.9 | 46.2 | 62.9 | | % change (q-o-q) sequential | 29.6 | 4.7 | 72.9 | 9.2 | | % change (y-o-y) | -23.7 | 25.8 | 26.8 | 28.7 | Notes:

1. NCAER: National Council of Applied Economic Research.

2. FICCI: Federation of Indian Chambers of Commerce & Industry.

3. CII: Confederation of Indian Industry.

Sources: NCAER, FICCI, CII and Dun & Bradstreet Information Services India Pvt. Ltd. |

Overall, economic activity is gathering strength, supported by the recovery in both demand and supply channels, sustained rollout of the vaccination programme, growth-enhancing proposals in the Union Budget and highly accommodative monetary conditions. Taking into account the baseline assumptions, the survey indicators, and model forecasts, real GDP growth6 is projected to pick up from (-) 8.0 per cent in 2020-21 to 10.5 per cent in 2021-22 – with a quarterly path of 26.2 per cent in Q1, 8.3 per cent in Q2, 5.4 per cent in Q3, and 6.2 per cent in Q4 – with risks evenly balanced (Chart I.10 and Table I.4). For 2022-23, assuming a normal monsoon, and no major exogenous or policy shocks, the structural model estimates indicate real GDP growth at 6.8 per cent, with quarterly growth rates in the range of 6.2-7.3 per cent. | Table I.4: Projections - Reserve Bank and Professional Forecasters | | (Per cent) | | | 2020-21 | 2021-22 | 2022-23 | | Reserve Bank’s Baseline Projections | | | | | Inflation, Q4 (y-o-y) | 5.0 | 5.1 | 4.7 | | Real GDP growth | -8.0 | 10.5 | 6.8 | | Median Projections of Professional Forecasters | | | | | Inflation, Q4 (y-o-y) | 4.9 | 5.0 | | | Real GDP growth | -7.5 | 11.0 | | | Gross domestic saving (per cent of GNDI) | 28.9 | 29.6 | | | Gross capital formation (per cent of GDP) | 27.7 | 30.1 | | | Credit growth of scheduled commercial banks | 6.4 | 8.0 | | | Combined gross fiscal deficit (per cent of GDP) | 14.0 | 10.5 | | | Central government gross fiscal deficit (per cent of GDP) | 9.5 | 6.8 | | | Repo rate (end-period) | 4.00 | 4.00 | | | Yield on 91-days treasury bills (end-period) | 3.3 | 3.9 | | | Yield on 10-year central government securities (end-period) | 6.2 | 6.5 | | | Overall balance of payments (US$ billion) | 97.2 | 50.6 | | | Merchandise exports growth | -10.3 | 15.0 | | | Merchandise imports growth | -19.0 | 24.1 | | | Current account balance (per cent of GDP) | 1.0 | -0.8 | | Note: GNDI: Gross National Disposable Income.

Sources: RBI staff estimates; and Survey of Professional Forecasters (March 2021). | There are upside as well as downside risks to the baseline growth path. A faster decline in COVID-19 infections helped by a rapid vaccination drive, large pent-up demand for contact-intensive services, and stronger global demand provide an upside to the baseline growth path. The uncertainty associated with the spread of COVID-19, including new mutants of the virus, deviation of the south-west monsoon from the baseline assumption of a normal monsoon, and elevated crude oil prices and global financial market volatility pose downside risks. I.4 Balance of Risks The baseline projections of inflation and growth are conditional on the assumptions of key domestic and international macroeconomic and financial conditions described in the previous sections. The inherent uncertainties associated with such assumptions have exacerbated due to the COVID-19 pandemic and could have a significant bearing on the inflation and growth trajectories. This section explores plausible alternative scenarios to assess the balance of risks around the baseline projections. (i) Global Growth Uncertainties The COVID-19 pandemic induced the severest global recession in decades in 2020. Global growth is expected to recover to 5.5 per cent in 2021, reflecting base effects, the expected moderation in new infections, the rollout of the vaccination programme and large monetary and fiscal support. However, the uncertainty about the pandemic’s spread and its containment continues to pose high risks to the global outlook on both sides. A faster spread of mutated coronavirus variants across the world and an unequal access to vaccines across countries can result in a shallower and delayed global recovery. A surge in global bond yields – as experienced in February 2021 on reflation trade – could induce large global financial market volatility, disorderly adjustment in asset prices and disrupt global demand. In such a scenario, if global recovery is 100 bps below the baseline, domestic growth and inflation could be lower by around 40 bps and 30 bps, respectively, from the baseline trajectories. Conversely, success in containing the spread of new mutants, widespread and equitable distribution of vaccines across the world, and additional policy stimulus could provide a boost to global economic activity. In this scenario, assuming that global growth surprises by 100 bps on the upside, domestic growth and inflation could edge higher by around 40 bps and 30 bps, respectively (Charts I.11a and I.12a). (ii) International Crude Oil Prices International crude oil prices have risen sharply on production cuts and hopes of demand revival. For a net energy importer like India, the dynamics of international crude price movements have significant macroeconomic implications. A quicker containment of COVID-19 inducing higher global growth than the baseline and a faster closing of the global output gap along with sustained production cuts by the OPEC plus could lead to a sharper increase in international crude oil prices. Assuming crude oil price to be 10 per cent above the baseline, domestic inflation and growth could be higher by 30 bps and weaker by around 20 bps, respectively, over the baseline. Conversely, crude oil prices could soften if the recovery is more subdued owing to a faster spread of virus mutations, the delays in vaccination or improved supplies of shale gas. As a result, if the price of the crude falls by 10 per cent relative to the baseline, inflation could ease by around 30 bps with a boost of 20 bps to growth (Charts I.11a and I.12a).  (iii) Exchange Rate The INR has exhibited two-way movements over the past six months, reflecting both global and domestic factors. Looking ahead, heightened volatility in global financial markets, especially a snapback in global sovereign bond yields – as observed in February 2021 – could lead to a broader risk aversion to EME assets and net capital outflows. In such a scenario, should the INR depreciate by 5 per cent from the baseline, inflation could move up by around 20 bps while GDP growth could be higher by around 15 bps through increased net exports (Charts I.11b and I.12b). On the other hand, given India’s relatively better growth outlook and expectations of strong capital inflows, there could be INR appreciation. If the INR appreciates by 5 per cent relative to the baseline, inflation and GDP growth could moderate by around 20 bps and 15 bps, respectively, vis-à-vis the baseline. (iv) Food Inflation Food inflation has softened since December 2020, largely led by the sharp fall in prices of vegetables and moderation in prices of cereals. Going forward, the bumper kharif harvest, record rabi sowing, further easing of supply chains and effective supply management measures could moderate food inflation by 100 bps below the baseline. Conversely, the recent hardening of global food prices and domestic demand-supply gaps in key food items like pulses, edible oils and fats, and eggs, fish and meat could lead to persistent upward pressures of around 100 bps on food inflation. Higher inflation expectations could then add to sustained pressures on headline inflation. The baseline assumes a normal south-west monsoon in 2021 and any deviations in the actual outturn on either side would be a critical factor in determining the food as well as headline inflation (Charts I.11b and I.12b). I.5 Conclusion Domestic economic activity is widely expected to rebound strongly in 2021-22. Rapid vaccination drive, large pent-up demand, investment enhancing measures by the government and better external demand provide an upside to the baseline growth path while surge in infections, new mutants, deviation of the south-west monsoon from the baseline assumption of a normal monsoon, higher crude oil and non-oil commodity prices and global financial market volatility impart downside risks to the baseline growth path. Lingering supply chain disruptions, rising global crude oil prices and stronger pass-through of input costs could push headline inflation above the baseline. There is also the probability of softer international crude oil prices on the back of a weaker than anticipated global demand, bountiful foodgrains production and effective supply management coming together to ease inflation more than anticipated. The evolving COVID-19 trajectory and progress on vaccination remain the key drivers of economic activity and inflation, globally and in India. _________________________________________________________

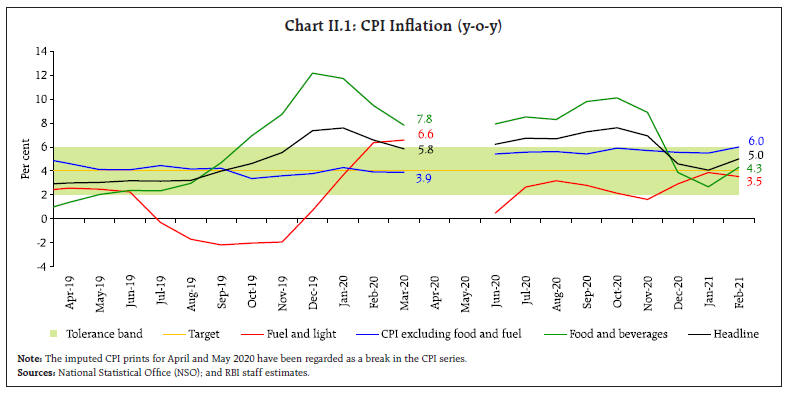

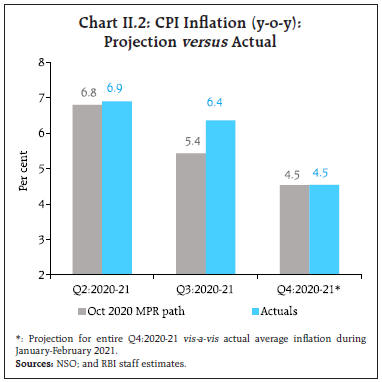

II. Prices and Costs In 2020-21, inflation breached the upper tolerance band of 6 per cent for six consecutive months in the post-lockdown period (June-November 2020) due to a series of cost-push shocks – supply chain disruptions; weather shocks; higher crude oil and other commodity prices; and higher taxes. The sharp correction during December-January was reversed on adverse base effects in February. Core inflation remained sticky at elevated levels. Costs of farm and industrial inputs recovered with the gradual unlocking of the economy and rural wage growth moderated although it remained higher than in the pre-lockdown period. In the months following the publication of the October 2020 MPR, inflationary pressures got accentuated and headline inflation1 remained above the upper tolerance threshold. Core inflation also stayed sticky at elevated levels. During December 2020-January 2021, however, there was a sharp correction and inflation eased significantly, moving closer to the target, only to reverse to 5.0 per cent in February 2021, primarily due to adverse base effects. Core inflation (CPI inflation excluding food and fuel) surged to a 28-month high of 6.0 per cent in February 2021 under the combined effects of rising industrial raw material prices, record high petroleum product prices and the higher cost of doing business in the post-lockdown period (Chart II.1). The Reserve Bank of India (RBI) Act enjoins the RBI to set out deviations of actual inflation outcomes from projections, if any, and explain the underlying reasons thereof. The October 2020 MPR had projected moderation in CPI inflation from 6.8 per cent in Q2:2020-21 to 5.4 per cent in Q3 and 4.5 per cent in Q4. In Q3, actual inflation was 100 basis points (bps) above projection (Chart II.2). A sharp, unanticipated increase in food inflation – double-digit inflation in eggs, meat and fish (due to fragmented supply chains), pulses (tight demand supply balance), edible oils (high international prices), and vegetables (unseasonal rains) – led to this substantial overshoot. Retail price margins for food also increased, with the persistence of supply chain disruptions. International crude oil prices (Indian basket) jumped from the baseline assumption of US$ 40.9 per barrel for H2:2020-21 to US$ 61.2 per barrel by February 2021. Gold prices remained elevated in Q3:2020-21 over COVID-19 concerns, supported by highly accommodative monetary policies in the major advanced economies. Cost-push pressures also impinged on core inflation more than anticipated. In Q4 (January-February), the correction in food prices resulted in actual inflation aligning with the projection (Chart II.2).

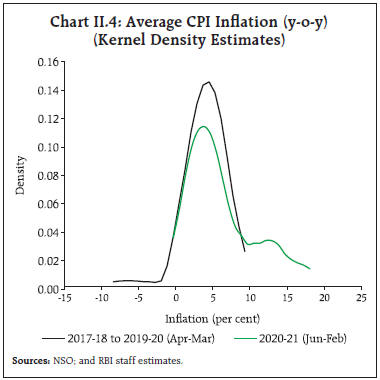

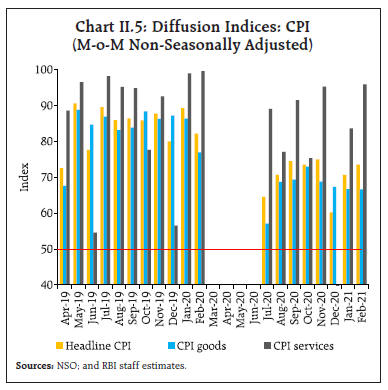

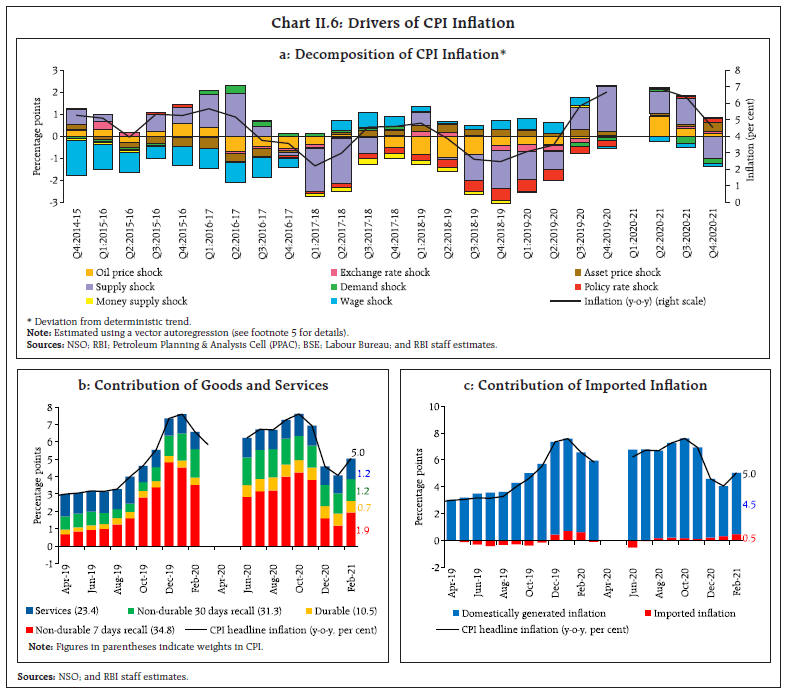

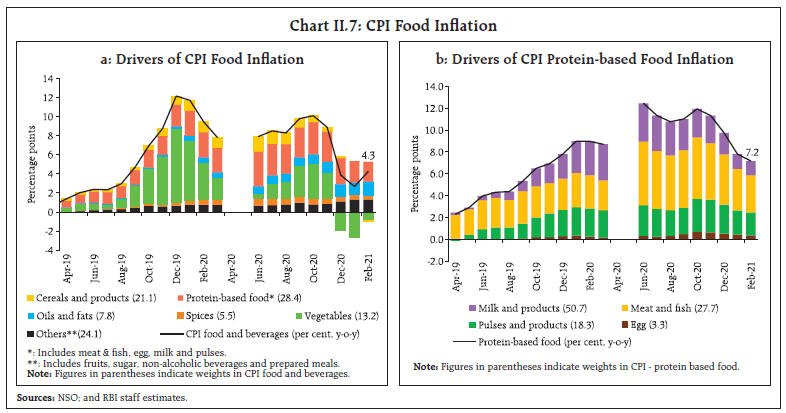

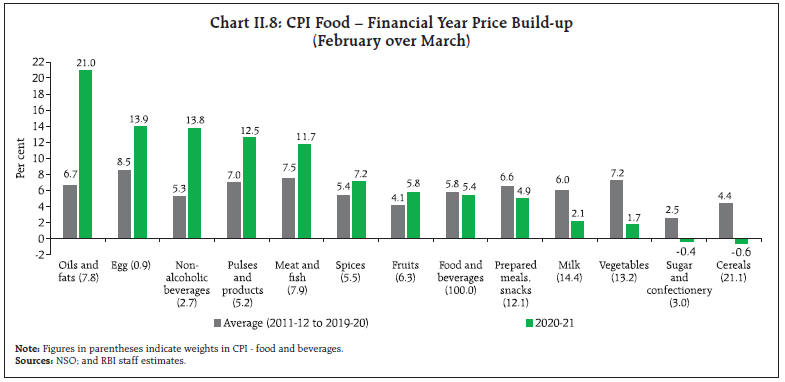

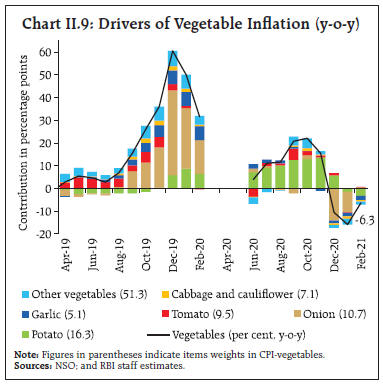

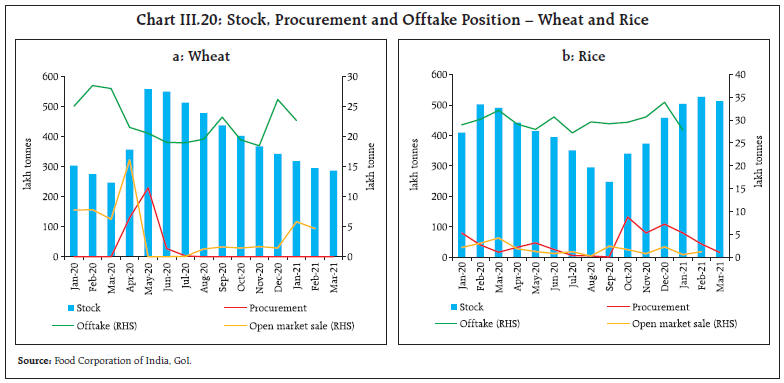

II.1 Consumer Prices The sharp upward movement of inflation to a peak of 7.6 per cent in October 2020 came about from a pick-up in price momentum in food as well as in the core category.2 Thereafter, strong favourable base effects brought about a moderation in headline inflation to 6.9 per cent in November 2020, more than offsetting positive momentum in all these components. In December 2020, a negative momentum in headline inflation due to a sharp decline in food prices, along with favourable base effects, resulted in headline inflation declining by 2.3 percentage points. In January 2021, headline inflation moderated further due to a large negative momentum engendered by food prices. In February 2021, an adverse base effect of around 70 bps resulted in a substantial pick-up in inflation (Chart II.3). Reflecting broad-based price pressures, the distribution of CPI group/sub-group inflation in 2020-21 was centred at 4.9 per cent, higher than the sub-4 per cent levels seen in recent years (Chart II.4). With several sub-groups exhibiting double-digit inflation, the inflation distribution also exhibited a fat tail, pushing mean headline inflation in excess of 6.0 per cent. The diffusion indices of price changes in CPI items on a non-seasonally adjusted basis3 increased in January-February 2021, indicative of price pressures across the CPI basket (Chart II.5).4 II.2 Drivers of Inflation The relative role of various demand and supply shocks impinging upon the inflation dynamics can be captured through vector autoregression (VAR) estimates and historical decomposition.5 The high inflation episode in Q3:2020-21 was predominantly due to supply shocks. In Q4, supply side factors turned benign pulling down headline inflation. On the other hand, easy monetary conditions and the firming up of asset and crude oil prices contributed positively to the deviation of inflation from trend levels in Q3 and Q4. Muted demand conditions and moderation in rural wage growth pulled down inflation in Q3 and Q4, offsetting these effects (Chart II.6a).  High volatility in perishable goods (non-durable goods with a 7-day recall6) from supply shocks in both directions had a significant bearing on the inflation trajectory. With the surge in vegetable prices, the contribution of perishables to overall inflation increased to 55.3 per cent during September-November 2020 from 46.8 per cent in June-August 2020. Subsequently, as vegetable prices corrected, perishables’ contribution decreased sharply to 32.0 per cent during December 2020-January 2021. In February 2021, following the lower rate of deflation in the prices of vegetables, perishables’ share increased to 38.6 per cent. Reflecting the increase in prices of protein-based food, edible oils and other food items, the contribution of semi-perishable goods (non-durable goods with a 30-day recall) remained elevated (Chart II.6b). Imported components contributed 0.5 percentage points to headline inflation in February 2021, driven by gold, silver, edible oils and higher domestic taxes on petroleum products (Chart II.6c).  Food Group Food inflation rose sharply to 10.1 per cent in October 2020 and remained above 6 per cent for 14 consecutive months till November 2020. It moderated quickly in the subsequent months to 2.7 per cent in January 2021 before picking up to 4.3 per cent in February 2021. These large variations were primarily driven by movements in prices of vegetables (Chart II.7). The softening of inflation in respect of cereals and products, milk and sugar and confectionery also aided the easing in food inflation. On the other hand, there were upward pressures from oils and fats, non-alcoholic beverages, prepared meals and snacks and fruits. Despite a sizeable moderation, inflation in five out of twelve food sub-groups was still in double digits in February 2021. Seven of the twelve sub-groups recorded increases above the historical average (Chart II.8). Rural and urban food inflation exhibited broadly similar movements, with no significant difference between month-over-month changes in prices of food and its sub-groups in rural and urban areas.7  In the case of cereals (weight of 9.7 per cent in the CPI and 21.1 per cent in the food and beverages group), a bumper kharif rice production and record buffer stocks – around 6.7 times the norms for rice and 2.1 times for wheat as on March 16, 2021 – led to easing in inflation to (-)0.3 per cent in February 2021 from 7.9 per cent in June 2020. Higher rabi sowing has kept the price pressures subdued despite higher procurement and exports of both rice and wheat.  Inflation in prices of vegetables (weight of 6.0 per cent in the CPI and 13.2 per cent in the food and beverages group) rose steeply to a peak of 22.1 per cent in October 2020 and then corrected rapidly to move into deflation during December 2020-February 2021, driven primarily by a large fall in onion, tomato and potato prices (Chart II.9). Potato price inflation reached a peak of 107.0 per cent in November 2020. Higher imports and fresh arrivals of early rabi production in the market led to a sharp easing in prices during December 2020-February 2021, with a deflation of (-) 21.3 per cent in February 2021.

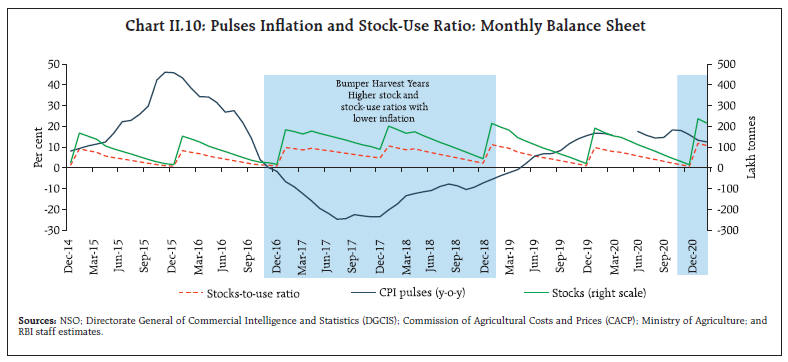

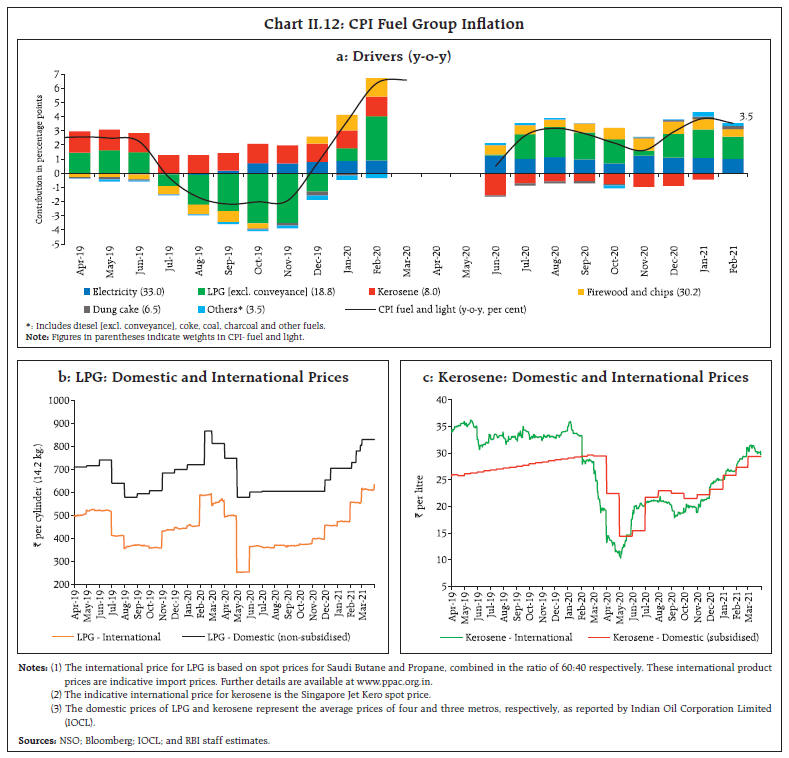

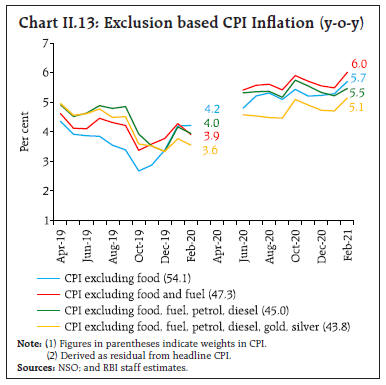

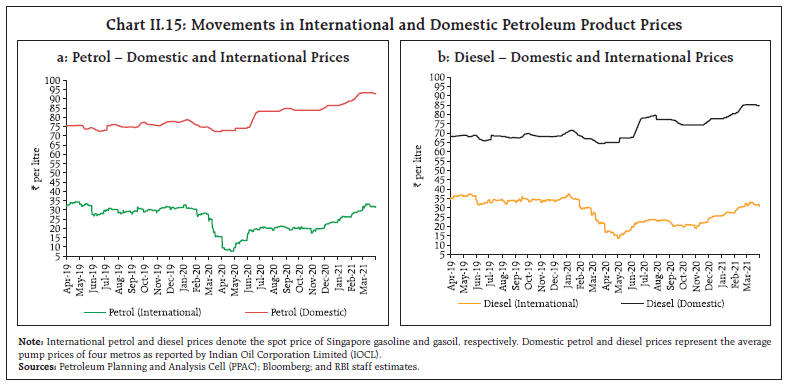

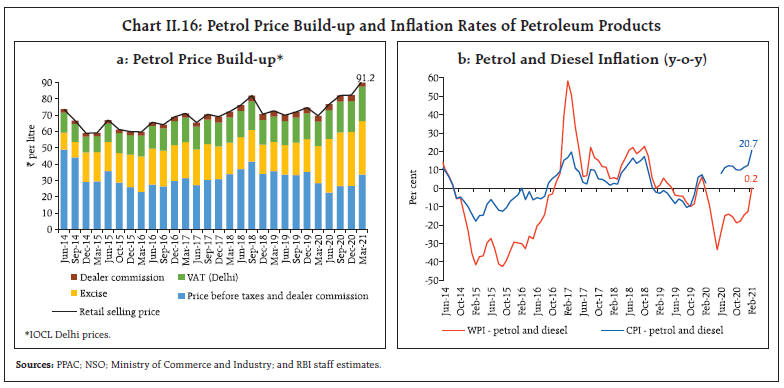

Inflation in onion prices, which was in negative territory during August-September 2020, witnessed substantial price pressures during September-November 2020 as excess rainfall in major producing regions of Madhya Pradesh, Gujarat, Karnataka and Maharashtra damaged the kharif crop and impacted late kharif production, resulting in lower market arrivals. To contain the escalation in prices, the Government imposed an export ban on onions in September 2020 (removed in January 2021), increased imports, released buffer stocks and imposed stock holding limits on wholesalers and retailers. These steps, along with fresh arrivals, led to onion prices moving into deflation during November 2020-January 2021. Onion prices picked up again in February 2021, however, due to drop in arrivals on account of unseasonal rainfall in January 2021 in Maharashtra. In the case of the third key vegetable, i.e., tomatoes, low arrivals from the key producing regions in Karnataka and Maharashtra on the back of excess rainfall pushed inflation to a peak of 54.5 per cent in September 2020. Thereafter, with an increase in fresh arrivals, prices eased beginning October 2020. In protein-based food items, inflation in pulses (weight of 2.4 per cent in the CPI and 5.2 per cent in the food and beverages group) was in double digits throughout 2020-21. To improve domestic supplies, the government eased restrictions and issued licenses for imports, reduced import duties on masur, released 2 lakh tonnes of tur (arhar) from the buffer stock and extended the time limit for import of tur under the import quota of 4 lakh tonnes for 2020-21. Reflecting these measures, as well as the arrival of kharif pulses and favourable base effects, pulses inflation moderated to 12.5 per cent in February 2021 from 18.3 per cent in October 2020. The production of pulses at 244 lakh tonnes in 2020-21 (second advance estimates for 2020-21) is expected to augment the domestic availability and improve the stock-use ratio (Chart II.12). Pulses inflation can thus be expected to moderate in the coming months, given the past relationship between production/stocks and prices8, although pressures may persist in some items like tur and urad. Among animal protein-rich items, inflation in egg, meat and fish also remained in double digits during most of 2020-21. It eased during November 2020 - February 2021, largely due to the fall in prices of chicken from improved supplies and a decline in demand due to bird flu during January 2021. Prices of mutton and pork, however, remained high due to supply bottlenecks and higher demand for protein-based food items.  Prices of milk and products (weight of 6.6 per cent in the CPI and 14.4 per cent in the food and beverages group) remained muted in H2:2020-21, reflecting a quick restoration of supply chains of the well-established system of cooperatives amidst lower demand from the bulk segment. Prices of sugar and confectionery (weight of 1.4 per cent in the CPI and 3.0 per cent in the food and beverages group) eased during September 2020 - February 2021 on the back of expectations of a bumper crop and higher domestic production even as international sugar prices increased due to concerns over lower global availability in 2020-21.9 Prices of oils and fats (weight of 3.6 per cent in the CPI and 7.8 per cent in the food and beverages group) remained one of the major pressure points throughout the year. Higher demand for mustard oil coupled with elevated international prices10 (particularly palm oil and soybean oil) resulted in oils and fats inflation peaking at around 20 per cent in December 2020-February 2021. The government reduced the basic customs duty (BCD) on crude palm oil from 37.5 per cent to 27.5 per cent effective November 27, 2020 and then revised it to 32.5 per cent [including the Agricultural Infrastructure Development Cess (AIDC)] effective February 2, 2021. Mustard oil and refined oil were the highest contributors to elevated edible oil inflation. Retail Margins Average retail price margins over wholesale prices increased across all the major sub-groups (cereals, vegetables, edible oils and pulses) during the post-lockdown period, pulling up headline inflation. The margins were higher in edible oils, vegetables and pulses than in the other two sub-groups (Chart II.11).11 CPI Fuel Group Inflation in fuel prices initially moderated from 3.2 per cent in August 2020 to 1.6 per cent in November 2020, due to a decline in LPG and PDS kerosene prices and favourable base effects. Fuel inflation then increased to 3.5 per cent in February 2021, led by prices of LPG, kerosene and dung cake (Chart II.12a). The movements in LPG inflation largely reflected the lagged impact of international prices (Chart II.12b). PDS-kerosene prices were in deflation throughout 2020-21, as international prices to which they are linked have been below pre-COVID levels since April 2020 (Chart II.12c). CPI excluding Food and Fuel CPI inflation excluding food and fuel, or core inflation, remained sticky and hovered between 5.4 per cent and 6.0 per cent during September 2020 to February 2021. Excluding petrol, diesel, gold and silver also, core inflation remained elevated (between 4.5 per cent and 5.1 per cent) over this period (Chart II.13). While the price build-up in the core categories was similar to the historical average, considerable variation was observed across subgroups: transport and communication, pan, tobacco and intoxicants, personal care and effects, health and recreation and amusement exhibited substantially higher build-up than the long-term average whereas clothing and footwear, housing, household goods and services and education exhibited subdued build-ups (Chart II.14).  In H2:2020-21, crude oil prices (Indian basket) jumped by nearly 50 per cent – from around US$ 41 per barrel in September 2020 to US$ 61 per barrel in February 2021. This sharp rise in international prices, along with the non-reversal of the substantial post-lockdown hike in excise duties and value added taxes (VATs), resulted in domestic petrol and diesel pump prices reaching historical highs by February 2021 (Chart II.15b). The combined share of central excise and states’ value added tax (VAT) in petrol prices has risen from ₹22 per litre (31 per cent) in mid-2014 and ₹38 per litre (54 per cent) in March 2020 to ₹53 per litre (61 per cent) in February 2021 (Chart II.16a). While the WPI measures basic prices less trade discounts, thereby leaving out indirect taxes, retail prices are inclusive of taxes. CPI petrol and diesel inflation has been in double digits since July 2020 and was at 20.7 per cent in February 2021; in contrast, WPI petrol and diesel prices were in sharp double digit deflation for most part of the financial year, with February 2021 seeing a reading of only 0.2 per cent (Chart II.16b).

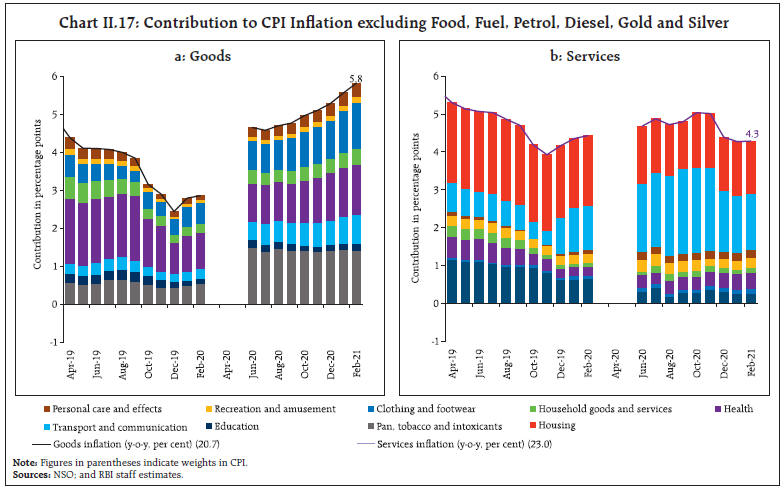

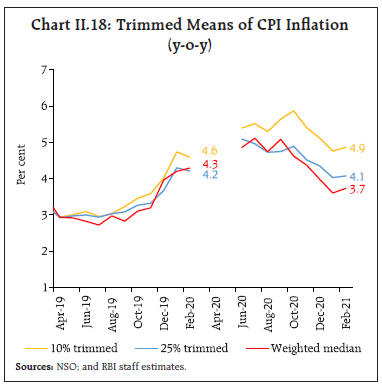

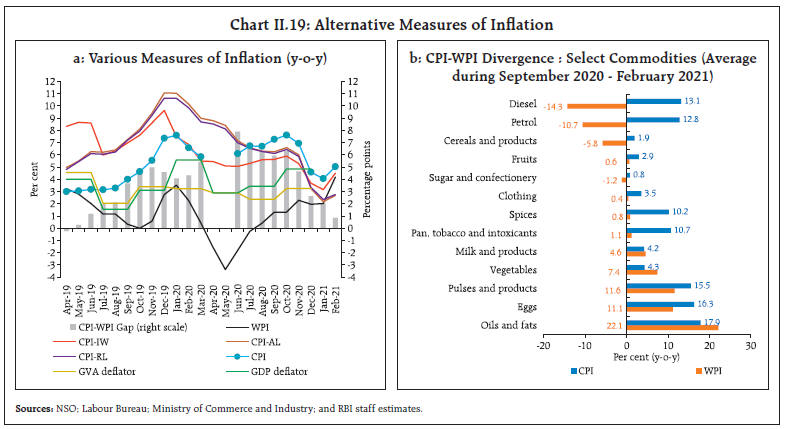

Compared to pre-COVID levels, measures of core inflation remain elevated, indicative of significant cost-push pressures across sectors in the post-lockdown period. Price inflation in the goods component, i.e., excluding food, fuel, petrol, diesel, gold and silver (with a weight of 20.7 per cent in CPI) rose to 5.8 per cent in February 2021 from 4.7 per cent in August 2020, driven by health care goods – particularly medicines, clothing and footwear goods and transportation goods like motor vehicles (Chart II.17a). Core services inflation (weight of 23.0 per cent in CPI) rose from 4.0 per cent in August 2020 to 5.0 per cent in November 2020, primarily due to higher prices of recreation, education, transportation and communications services. Subsequently, core services inflation moderated to 4.3 per cent in January-February 2021 as inflation in prices of communication dropped sharply due to favourable base effects along with some moderation in education and recreation services inflation. Housing inflation, which primarily includes rental charges, at 3.2 per cent during November 2020 - February 2021 was lower than the pre-COVID levels; however, it was the second largest contributor to core services inflation (Chart II.17b).

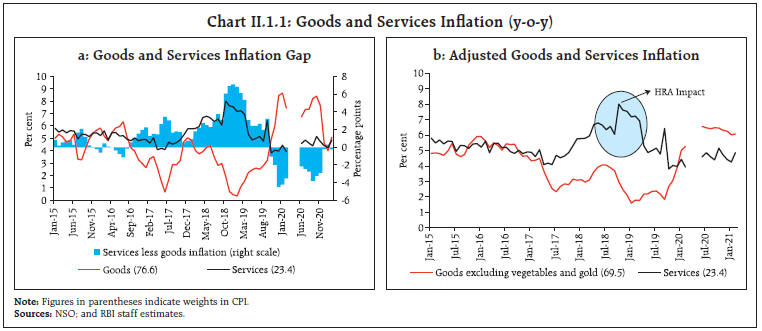

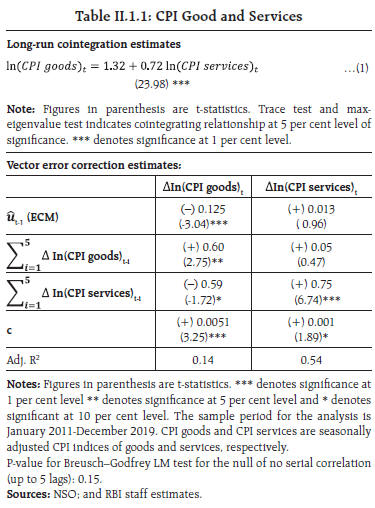

In sum, headline inflation dynamics in the post-lockdown period were primarily driven by goods inflation. Services inflation is the more durable component of the CPI and drives goods inflation over time (Box II.1). Box II.1: CPI Goods and Services: Do they Converge after Shocks? Cross-country evidence suggests that services inflation, on average, exceeds goods inflation due to a variety of factors such as lower productivity in non-tradable services (Balassa-Samuelson effect), higher mark-ups in services due to reduced competition and increased demand for services as per capita income rises (Ferrara 2019, Zaman 2015). In the post-lockdown period, however, CPI goods inflation (with a weight of 76.6 per cent in the CPI basket) exceeded CPI services (weight of 23.4 per cent) inflation substantially, with the gap increasing from 2.2 percentage points in June 2020 to 3.8 percentage points in September 2020. In February 2021, the gap narrowed to around 30 bps. In the past too, there have been episodes of goods and services inflation exhibiting divergent patterns, as during September 2016 to September 2019. Movements in CPI goods inflation excluding vegetables and gold and CPI services inflation (barring the period influenced by the statistical HRA12 impact), however, tend to show greater co-movement (Chart II.1.1). For India, the evidence suggests that prices of goods and services exhibit co-movement over time, i.e., the two series are cointegrated (Table II.1.1). This is consistent with the cross-country evidence (Peach, 2004). Given the evidence of long-run cointegration, the short-run dynamics can be further explored through a Vector Error Correction Model (VECM). The VECM analysis indicates a significant error correction (EC) term in CPI goods prices, while it was found to be insignificant in the case of CPI services prices. This suggests that following a shock resulting in a divergence from the long run equilibrium, it is goods prices that make the necessary adjustment to restore equilibrium.

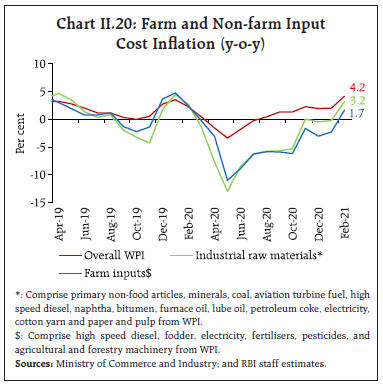

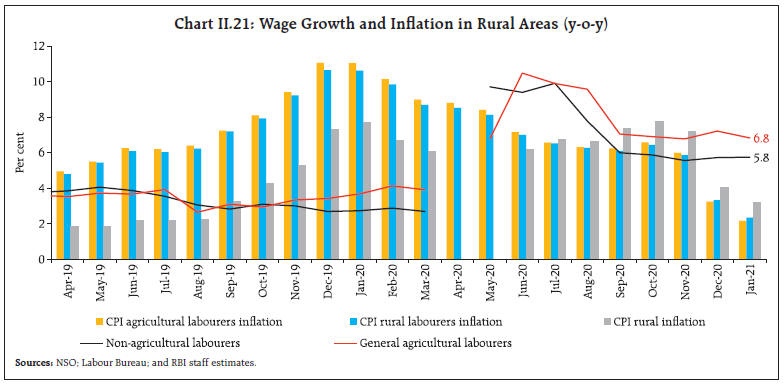

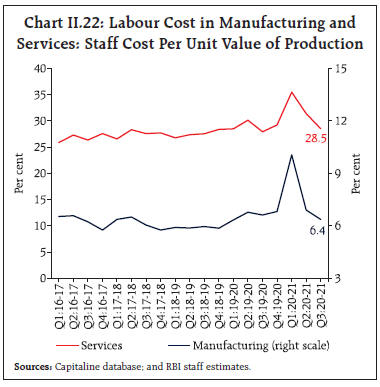

CPI goods prices are considerably influenced by the volatility induced by perishables such as vegetables and can result in divergences from CPI services prices over short periods. Services inflation, on the other hand, represents the relatively sticky component in the CPI basket and can spill over to goods inflation, resulting in generalised inflationary pressures. References: Ferrara, L. (2019), “What is Behind the Change in the Gap between Services Price Inflation and Goods Price Inflation?”, ECB Economic Bulletin Boxes, 5. Peach, R.W., Rich, R., and Antoniades, A. (2004), “The Historical and Recent Behavior of Goods and Services Inflation”, Federal Reserve Bank of New York, Economic Policy Review, December. Zaman, S. (2015), “The Gap Between Services Inflation and Goods Inflation”, Economic Trends, Federal Reserve Bank of Cleveland. | In addition to exclusion-based measures, trimmed means of inflation provide a measure of underlying inflation dynamics and are computed by statistically eliminating items with extremely positive and negative inflation. The trimmed mean indicators showed easing of inflation over the period under review in view of the omission of a few large outliers – such as vegetables, pulses, edible oils, transport fare, and pan, tobacco and intoxicants – in either direction. In contrast, exclusion-based measures, which capture persistent trends in inflation by eliminating ex-ante identified idiosyncratic and volatile components, suggest stickiness in inflation (Charts II.13 and II.18). Other Measures of Inflation Inflation measured by sectoral CPIs for agricultural labourers (CPI-AL) and rural labourers (CPI-RL) remained below headline CPI inflation in H2:2020-21. Lower inflation in food items along with their higher weight in CPI-AL and CPI-RL and subdued inflation in fuel, and clothing and footwear groups contributed to the relatively lower inflation prints for CPI-AL and CPI-RL. Inflation in terms of CPI for industrial workers (CPI-IW) though their gap narrowed. also remained below the headline CPI during H2.13 The price build-up in CPI-IW for clothing, housing and miscellaneous groups was lower relative to the headline CPI; that of fuel, and pan, tobacco and intoxicants groups was higher; and the fall in food prices was muted.14  WPI inflation also remained below CPI inflation in H2:2020-21, although it has quickly inched up close to CPI inflation in recent months (Charts II. 19a). From its trough in May 2020, WPI inflation charted a V-shaped uptrend in view of a sharp rise in fuel and non-food commodity prices. In contrast, WPI food inflation decelerated continuously from September 2020 and fell into negative territory in January 2021 before moving up in February 2021 to 3.3 per cent. Average WPI food inflation during September 2020 to February 2021 at 3.7 per cent was way lower than average CPI food inflation at 6.6 per cent, with inflation across major food sub-groups, except vegetables, milk and products, oils and fats, recording lower prints in the WPI than in the CPI. The largest deviation between CPI and WPI emanated from inflation in petroleum products, especially in petrol and diesel, reflecting the wedge due to tax components. Similarly, tax implications were visible in prices for pan, tobacco and intoxicants – while CPI for these items remained in double digits (average 10.7 per cent), inflation in WPI beverages, and tobacco products averaged 0.2 and 2.5 per cent, respectively, during September 2020 to February 2021 (Chart II.19b).  Inflation measured in terms of gross value added (GVA) and gross domestic product (GDP) deflators clocked a pick-up from Q1:2020-21 to Q3, broadly in alignment with WPI inflation. II.3 Costs The measures of cost inflation – farm inputs and industrial raw materials derived from WPI – moved higher with the gradual unlocking of the economy, albeit with transient dips (Chart II.20). The firming up of global crude oil prices during H2:2020-21 impacted the prices of inputs such as high-speed diesel, naptha, aviation turbine fuel, and furnace oil. Minerals and non-food articles also generally rose during October 2020-February 2021. Prices of fibres emerged out of deflation in January 2021 in line with a pick-up in raw cotton and raw silk prices. Reflecting this, inflation in cotton yarn price registered sharp uptick.  Within farm sector inputs, fodder price inflation remained elevated in double digits, during October 2020 to February 2021 due to the damage from excess rains during September-October 2020. Inflation in fertilisers remained muted in line with subdued cost of raw materials such as natural gas. Prices of electricity – a key constituent of both industrial and farm inputs – remained in deflation on an average during H2, barring a transient spike in November. Inflation in prices of agricultural machinery and implements recorded a modest increase during November 2020-February 2021. Nominal rural wages for both agricultural and non-agricultural labourers hardened during H1:2020-21, reflecting labour shortages during the lockdown period and the hike in wages by ₹20 under the Mahatma Gandhi National Rural Employment Guarantee (MGNREGA) scheme effective April 1, 2020. As the unlock phase progressed and labour availability improved, wage growth moderated in H2 although it remained higher than in the pre-lockdown period (Chart II.21). Growth in the value of production in Q3:2020-21 for listed firms in the manufacturing and services sectors outpaced the rise in staff costs. As a result, unit labour costs (measured as a ratio of staff cost to value of production) decreased during Q3:2020-21, reverting towards pre-COVID levels. Unit labour costs moderated from 6.9 per cent in Q2:2020-21 to 6.4 per cent in Q3:2020-21 for firms in the manufacturing sector and from 31.4 per cent to 28.5 per cent respectively, for the services sector firms (Chart II.22). Manufacturing, services and infrastructure firms polled in Reserve Bank’s enterprise surveys15 reported an increase in salary outgo in Q4:2020-21, with expectations of a further rise in Q1:2021-22 as the level of employment is likely to gradually edge up. Input costs were also expected to intensify further in Q1 and continue in Q2 and Q3 of 2021-22 with the pace of increase moderating a tad for the manufacturing sector. The surveyed firms reported passing through the costs to their selling prices in Q4:2020-21. Selling prices are expected to gain further traction in Q1:2021-22 and remain firm in Q2 and Q3 for all the three sectors (Chart II.23).

Manufacturing firms polled for the purchasing managers’ index (PMI) reported an increase in input prices in Q3:2020-21, with a further firming up in Q4 from higher costs of chemicals, metals, minerals, cotton and plastic; higher cost pressures were passed through to the clients resulting in an increase in selling prices. PMI services firms also reported continued increase in input prices in Q3 and Q4, driven by fuel, with the sharpest increase reported in prices of consumer services. Despite an increase in input costs, services sector firms reported lower selling prices in efforts to boost sales. II.4 Conclusion In 2020-21, inflation breached the upper tolerance band of 6 per cent for six consecutive months in the post-lockdown period (June-November 2020) due to a series of cost-push shocks – supply chain disruptions; weather shocks; higher crude oil and other commodity prices; and higher taxes. Inflationary pressures persisted despite a bumper kharif harvest. The increase in petrol and diesel prices is showing up in trade and transport costs, taxi and auto fares, and its second-round effects could push-up the prices of goods and services further in a broad-based manner, with firms regaining pricing power. Effective supply measures and tax rationalisation are critical to help anchor inflation expectations. If inflation remains close to the target on a durable basis, it can then provide monetary policy the space to adequately support the nascent recovery. _________________________________________________________

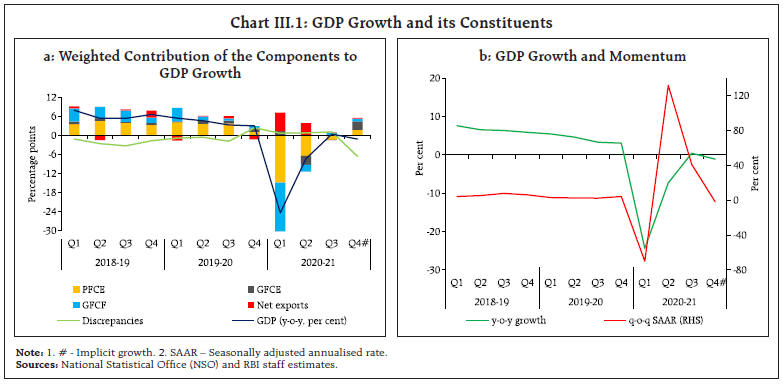

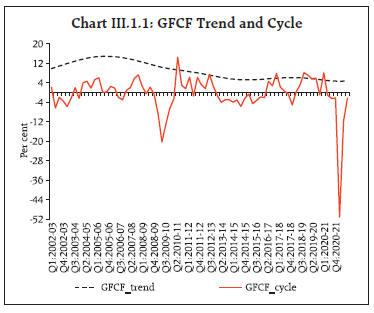

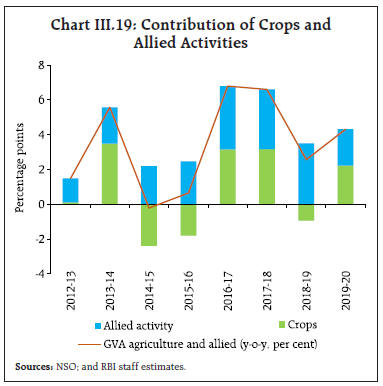

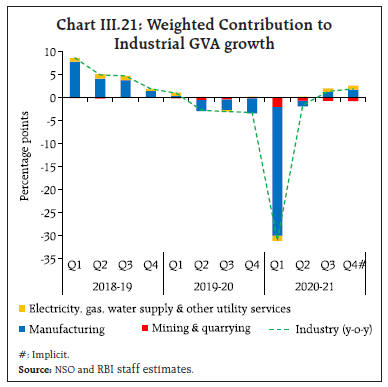

III. Demand and Output After the unprecedented contraction in Q1, real gross domestic product (GDP) recorded sequential upturn in Q2 and regained positive territory in Q3 with the ambit of the recovery broadening to encompass a wider spectrum of sectors, supported by a significant decline in COVID-19 infections. The recent increase in COVID infections, if not contained, could push back the normalisation process and impede the broader revival of economic activity. Economic activity in India in H2:2020-21 turned out to be more resilient than anticipated in the October 2020 MPR, supported by a significant decline in new COVID-19 infections from the mid-September 2020 peak and the rollout of the vaccination drive from mid-January 2021. After the unprecedented contraction in Q1, real gross domestic product (GDP) recorded sequential upturn in Q2 and regained positive territory in Q3 with the ambit of the recovery broadening to encompass a wider spectrum of sectors since then. On the supply side too, the sustained resilience of agriculture and allied activities was complemented by manufacturing and services sector activity gaining some momentum. As a result, real gross value added (GVA) recorded positive growth in Q3 and is expected to be positive in Q4 also. III.1 Aggregate Demand Real GDP contracted by 8.0 per cent in 2020-21, according to the National Statistical Office’s (NSO) second advance estimates (SAE), although some slack can be attributed to on-budgeting of past subsidy payments in Q4 (Chart III.1a and Table III.1). The recovery in H2:2020-21 was on the back of revival in government expenditure and fixed investment and easing of the contraction in private consumption. Quarter-on-quarter seasonally adjusted annualised (qoq-SAAR) growth rates, however, moderated in Q3 and Q4 suggesting some flattening of momentum (Chart III.1b).

| Table III.1: Real GDP Growth | | (y-o-y, per cent) | | Item | 2019-20 | 2020-21 | Weighted Contribution* | 2019-20 | 2020-21 | | 2019-20 | 2020-21 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4# | | Private final consumption expenditure | 5.5 | -9.0 | 3.1 | -5.1 | 7.6 | 6.5 | 6.4 | 2.0 | -26.3 | -11.3 | -2.4 | 3.1 | | Government final consumption expenditure | 7.9 | 2.9 | 0.8 | 0.3 | 1.8 | 9.6 | 8.9 | 12.1 | 12.8 | -24.0 | -1.1 | 29.2 | | Gross fixed capital formation | 5.4 | -12.4 | 1.7 | -4.0 | 13.3 | 3.9 | 2.4 | 2.5 | -46.4 | -6.8 | 2.6 | 2.8 | | Exports | -3.3 | -8.1 | -0.7 | -1.6 | 3.0 | -1.3 | -5.4 | -8.8 | -22.0 | -2.1 | -4.6 | -3.7 | | Imports | -0.8 | -17.6 | -0.2 | -4.0 | 9.4 | -1.7 | -7.5 | -2.7 | -41.1 | -18.2 | -4.6 | -4.3 | | GDP at market prices | 4.0 | -8.0 | 4.0 | -8.0 | 5.4 | 4.6 | 3.3 | 3.0 | -24.4 | -7.3 | 0.4 | -1.1 | *: Component-wise contributions to growth do not add up to GDP growth because change in stocks, valuables and discrepancies are not included,

#: Implicit growth.

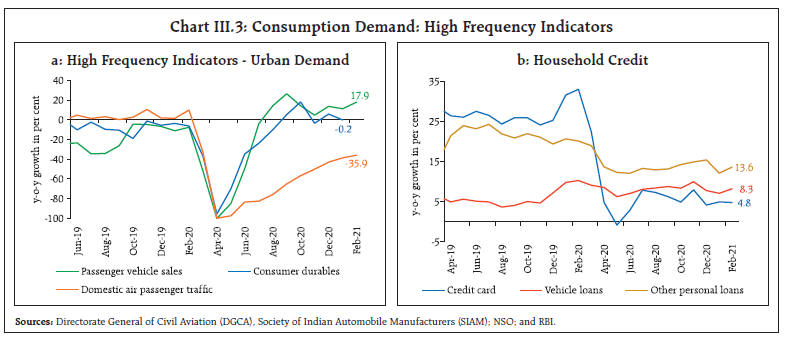

Source: National Statistical Office (NSO). | GDP Projections versus Actual Outcomes The October 2020 Monetary Policy Report (MPR) projected GDP growth at (-) 9.8 per cent for Q2:2020-21, (-) 5.6 per cent for Q3 and 0.5 per cent for Q4, with risks tilted to the downside. Actual outcomes in terms of the NSO’s SAE overshot these projections by 250 and 600 basis points in Q2 and Q3, respectively (Chart III.2), which may be largely attributed to faster than anticipated reduction in new COVID-19 infections in the country. The upside surprise in Q2 and Q3 largely stemmed from a better-than-expected performance in gross fixed capital formation. Data for Q4:2020-21 are expected on May 31, 2021. III.1.1 Private Final Consumption Expenditure Private final consumption expenditure (PFCE) – the mainstay of aggregate demand, severely dented during the pandemic – revived in H2:2020-21 as spending expanded from essential commodities and services towards discretionary items on the back of gradual relaxation of restrictions. The contraction in real PFCE moderated to 2.4 per cent in Q3 from 11.3 per cent in Q2. Spending on transport, hotels and restaurants, recreation and culture, which together contribute around 20 per cent to PFCE, also began improving in Q4. Several high frequency indicators of private consumption crossed pre-COVID levels, attesting to a broad-based momentum. Drilling down further reveals a divergence between urban and rural demand, with the former suffering the maximum damage and taking longer time to recover due to the loss of employment and heightened uncertainty. Some coincident and proximate high frequency indicators show that urban consumption started inching up from Q3:2020-21 and gained further strength in Q4 with the easing of restrictions. Passenger vehicle sales remained robust since August and posted double-digit growth in January and February 2021, partly reflecting shifting of preferences towards own vehicles over public transportation in the wake of the pandemic. The production of consumer durables, that had collapsed during H1, got revitalised and surpassed pre-COVID levels in December 2020 (Chart III.3a). Credit card outstanding and other personal loans, however, remained subdued (Chart III.3b). Domestic air passenger traffic, is still tepid and around two-third of pre-COVID-19 levels, reflecting lackluster activity related to tourism and entertainment, and with business meetings increasingly preferring the virtual mode.  Rural consumption recouped quickly and remained resilient on the back of record kharif production, sustained employment under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), and cash transfers under PM Kisan Samman Nidhi Yojana and other schemes. The households that sought employment under the MGNREGA scheme were 63 per cent higher in Q3:2020-21 and remained elevated in Q4. Indicators of rural demand – improved rabi acreage during 2020-21; higher production of fertilisers; and accelerated tractor sales during November-February – augur well for a brighter outlook. Motorcycle sales have remained in expansion zone since August 2020 (Chart III.4). The consumer non-durables output witnessed expansion in December 2020, before contracting in January 2021. Unemployment rates in both rural and urban areas recorded declines during H2 and supported private consumption. The labour force participation rate improved considerably in H2 vis-à-vis H1 but remains below pre-COVID levels. Nonetheless, the available data from different sources indicate that employment conditions have improved considerably in H2 (Chart III.5).

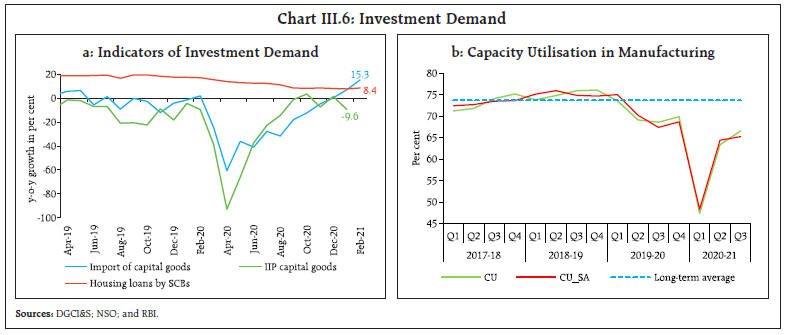

III.1.2 Gross Fixed Capital Formation The upturn in fixed investment gained traction during H2:2020-21, although it continues to be weighed down by surplus capacity and uncertainty surrounding the outlook. Congenial financial conditions are expected to continue supporting the recovery in fixed investment (Box III.1). Gross fixed capital formation (GFCF) expanded by 2.6 per cent on year-on-year basis in Q3 and is estimated to rise by 2.8 per cent in Q4. For the full year 2020-21, GFCF is estimated to have contracted by 12.4 per cent, given the sharp downturn in H1. The share of GFCF in aggregate GDP inched up to 32.8 per cent in H2 from 28.5 per cent in H1 and 31.9 per cent in H2:2019-20. Real estate and construction activity gained some momentum from Q3 – particularly in rural and semi-urban areas and affordable segments in urban areas – benefitting from lower mortgage rates, favourable pricing and a slash in stamp duty across several states. Among its proximate coincident indicators, steel consumption rose at a robust pace in January and February 2021 on top of double-digit growth in the preceding two months. Investment in machinery and equipment is also recovering as reflected by imports of capital goods remaining in the positive zone since December 2020 (Chart III.6a). The production of capital goods attained positive territory in December 2020 but shrank in January 2021. The capacity utilisation (CU) in the manufacturing sector improved to 66.6 per cent in Q3 from the previous quarter (Chart III.6b). Seasonally adjusted CU also increased to 65.2 per cent in Q3 from 64.4 per cent in the previous quarter.

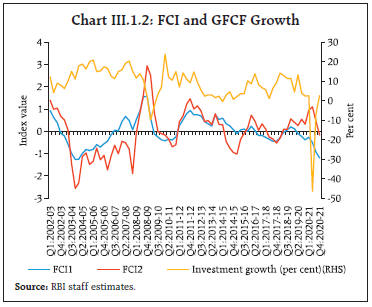

Box III.1: Investment and Financial Conditions Domestic financial conditions eased considerably with the onset of the pandemic as reflected in large drops in interest rates/spreads across the spectrum and ample surplus liquidity in the system on the back of conventional and unconventional policy measures by the Reserve Bank. The availability and cost of finance are amongst the important drivers of investment. A financial condition index (FCI) that is a summary indicator of financial conditions, helps to gauge their impact on investment activity. Following Kongsamut et. al. (2017), a FCI for India is constructed with variables drawn from equity, debt, money and forex markets. Using data from Q1:2002 to Q1:2020, the FCI includes the following five standardised variables – government securities (G-Sec) 10-year benchmark yield, corporate AAA bond spread over G-Sec yield, Nifty-50 return, repo rate and net foreign portfolio inflows – based on a preliminary analysis of their correlation and impact on investment. Dynamic factor model (DFM)1 and vector auto regression (VAR)2 approaches are used to construct FCIs (FCI1 and FCI2, respectively) for a robust analysis. Negative values of FCIs denote easier financial conditions while positive values indicate tighter financial conditions. Both the FCIs exhibit broadly similar directional changes (Chart III.1.2). The FCIs capture the tightening of financial conditions during the global financial crisis in 2008 and later in 2012-13 (associated with the period of high inflation and monetary tightening) as well as the recent easing of financial conditions after the pandemic. In terms of the DFM-based FCI, financial conditions at present are at their easiest since 2003.

Both the measures of FCIs are negatively correlated (statistically significant) with growth in gross fixed capital formation (GFCF) and the correlation is higher for lagged FCI, i.e., the easing of financial conditions is associated with a subsequent rise in investment growth (Table III.I.1). Granger causality tests confirm that the financial conditions have a statistical significant impact on investment growth (Table.I.2). The role of financial conditions in supporting investment activity is also corroborated by regression analysis with controls for expected economic activity (Table III.I.3). | Table III.I.1: Correlation Coefficient of FCIs with Investment Growth (y-o-y) | | | FCI1 | FCI2 | | Lag 0 | -0.26* | -0.52* | | Lag 1 | -0.43* | -0.57* | | Lag 2 | -0.57* | -0.59* | | Lag 3 | -0.61* | -0.52* | | Lag 4 | -0.54* | -0.38* | * indicates significant at 1% level

Source: RBI staff estimates. |

| Table III.I.2: Granger Causality Test | | Hypothesis | FCI1 (DFM) | FCI2 (VAR) | | F-statistic | Prob | F-statistic | Prob | | FCI does not Granger cause investment growth | 2.04 | 0.14 | 3.76*** | 0.03 | | FCI (-1) does not Granger cause investment growth | 1.54 | 0.22 | 1.08 | 0.34 | | FCI (-2) does not Granger cause investment growth | 2.45*** | 0.09 | 2.33 | 0.11 | | FCI (-3) does not Granger cause investment growth | 0.37 | 0.69 | 0.29 | 0.75 | | FCI (-4) does not Granger cause investment growth | 0.02 | 0.98 | 0.39 | 0.68 | ***indicates significant at 10% level.

Source: RBI staff estimates. |

| Table III.I.3: Regression Estimates | | Dependent Variable: Investment Growth | | | Coefficient | t-Statistic | | Investment growth (-1) | 0.54 | 4.67* | | FCI1(-2) | -3.05 | -2.98* | | GDP growth(+2) | 0.58 | 2.69* | | Constant | 0.27 | 0.14 | | R2 | 0.59 | | | Prob (J-statistic) | 0.79 | | Q-statistic (upto 4 lags) (p-value) | 0.23 | *: Significant at 1 per cent level.

The equation is estimated through generalised method of moments approach with the following instruments: lags of the endogenous variables as well as lag of world GDP growth, Brent crude prices and annual deviation rainfall in India from its long period average.

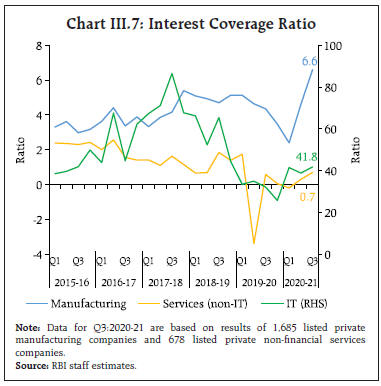

Source: RBI staff estimates. | References: Hatzius, J., Hooper, P., Mishkin, F., Schoenholtz, K., Watson, M. (2010), ‘Financial Conditions Indexes: A Fresh Look after the Financial Crisis’, NBER Working Papers, No. 16150. Kongsamut, P., C. Mumssen, A. Paret, T. Tressel (2017), ‘Incorporating Macro-Financial Linkages into Forecasts Using Financial Conditions Indices: The Case of France’ IMF Working Paper No. 17/269. Gulati, S., Ghosh, B., Deepmala and Kumar, S. (2021), ‘Investment and Financial Conditions’, Mimeo. | Half-yearly unaudited financial statements of listed non-government non-financial (NGNF) companies indicate that companies reduced their assets and used funds to reduce liabilities and build-up cash holdings – the former signifying deleveraging while the latter is indicative of precautionary saving in uncertain times. The debt to equity ratio of these firms dropped by 4.4 percentage points to 39.7 per cent in H1:2020-21, although it was still higher than its level in the previous two years. Investment by these companies remained subdued (Table III.2). At the same time, the interest coverage ratio of listed non-financial private companies increased in Q3, indicating improved debt servicing capacity of these companies (Chart III.7). The deleveraging and improved debt service capacity along with congenial financial conditions, recovery in capacity utilisation, resuscitation of private consumption and the expanded scope of the Production-Linked Incentive (PLI) Scheme offer a conducive environment for capex spending by non-financial private companies. Bank lending to micro, small and medium enterprises (MSMEs) segment has improved with increased utilisation under the government’s Emergency Credit Line Guarantee Scheme (ECLGS) to meet working capital requirements. As on February 28, 2021, the utilisation under ECLGS stood at 82 per cent. The PLI, covering 13 sectors with a commitment of the government support amounting to nearly ₹1.97 lakh crore, has begun attracting investment, including FDI, in the manufacturing sector. The significantly higher allocation for capital expenditure in the Union Budget 2021-22 is expected to crowd in private investment, and hence, augurs well for the revival of the private sector investment cycle. At the same time, possible stress in the balance sheet of banks – once special dispensations related to moratorium, asset classification and restructuring wane – could weigh on the investment outlook. Capital infusion and efficient and effective handling of loan delinquencies should be accorded priority, so that impediment to credit availability does not undermine revival in the investment cycle. | Table III.2: Listed Private Manufacturing Companies | | (Per cent) | | Period | Debt to Equity Ratio | Debt to Assets Ratio | Cash to Total Assets Ratio | Fixed Assets (y-o-y growth) | | H2:2017-18 | 36.9 | 19.3 | 2.9 | | | H1:2018-19 | 37.9 | 19.5 | 2.6 | | | H2:2018-19 | 37.7 | 19.8 | 3.0 | 4.6 | | H1:2019-20 | 34.7 | 18.6 | 3.1 | 7.8 | | H2:2019-20 | 44.1 | 21.9 | 3.8 | 8.2 | | H1:2020-21 | 39.7 | 21.0 | 4.7 | 2.1 | Note: Based on data of 1,249 common listed private manufacturing companies.

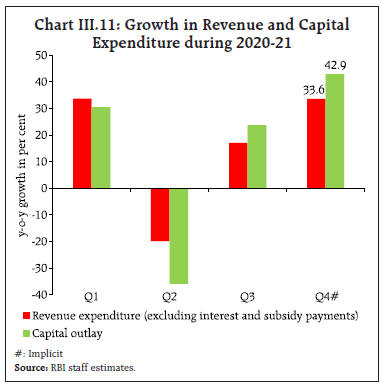

Source: RBI staff estimates. |  As per the first revised estimates for 2019-20, the gross domestic saving rate increased to 31.4 per cent of GDP from 30.6 per cent a year ago. Net household financial saving – a major source of funds for the economy – increased to 8.0 per cent of GDP in 2019-20 from 7.2 per cent in the preceding year. While the public sector was reliant on household surpluses for financing its deficit, the private sector depended primarily on internal resources for financing its investment needs (Chart III.8). According to preliminary estimates, the household financial savings rate spiked to 21.0 per cent of GDP in Q1:2020-21 as consumption waned amidst lockdowns and nearly normalised back to 10.4 per cent in Q2 as consumption recovered reinforced by pent-up demand3. III.1.3 Government Expenditure The contraction in Government Final Consumption Expenditure (GFCE) narrowed sharply from 24.0 per cent during Q2 to 1.1 per cent in Q3. GFCE support to aggregate demand revived in Q4 (the implicit growth in the SAE of NSO is 29.2 per cent). Overall, the fiscal support to aggregate demand remained substantial in H2. Excluding government expenditure, the economy would have recorded a contraction of 9.3 per cent in 2020-21. In 2021-22, the growth in revenue expenditure excluding interest and subsidy payments has been budgeted at 4.8 per cent, considerably on the lower side as compared with 13.1 per cent in 2020-21 (RE), indicating lower support to aggregate demand (Table III.3). | Table III.3: Key Fiscal Indicators – Central Government Finances | | Indicator | Per cent to GDP | | 2019-20 | 2020-21

(RE) | 2021-22

(BE) | | 1. Revenue receipts | 8.3 | 8.0 | 8.0 | | a. Tax revenue (Net) | 6.7 | 6.9 | 6.9 | | b. Non-Tax revenue | 1.6 | 1.1 | 1.1 | | 2. Non-debt capital receipts | 0.3 | 0.2 | 0.8 | | 3. Revenue expenditure | 11.6 | 15.5 | 13.1 | | a. Interest payments | 3.0 | 3.6 | 3.6 | | b. Major subsidies | 1.1 | 3.1 | 1.5 | | 4. Revenue expenditure excluding interest payments and subsidies | 7.3 | 8.6 | 7.8 | | 5. Capital expenditure | 1.7 | 2.3 | 2.5 | | 6. Capital outlay | 1.5 | 1.7 | 2.3 | | 7. Total expenditure | 13.2 | 17.7 | 15.6 | | 8. Gross fiscal deficit | 4.6 | 9.5 | 6.8 | | 9. Revenue deficit | 3.3 | 7.5 | 5.1 | | 10. Primary deficit | 1.6 | 5.9 | 3.1 | | Sources: Union Budget 2021-22 and RBI staff estimates. | During 2020-21, the fiscal position of the central government remained under stress due to revenue shortfalls and increase in COVID-19-related discretionary spending. Revenue collections gathered pace in H2, however, on the back of the pick-up in economic activity. The centre’s net tax revenue increased by 9.1 per cent during April-February 2020-21 and stood at 90.4 per cent of revised estimates (RE) for the full year (Chart III.9). Except excise and customs duties, tax collections witnessed declines across the board. Total GST collections were severely hit by the lockdown during H1:2020-21 but crossed the previous year’s level from September 2020 onwards (Chart III.10). In March 2021, GST collections were recorded at ₹1.24 lakh crore. Direct tax collections during April-February 2020-21 were 81.6 per cent of RE, down by 9.9 per cent over the previous year’s level. Total tax revenue is budgeted to be higher in 2021-22 than in the previous year (Table III.4). The revenue expenditure for the full year 2020-21 was revised upward by 14.5 per cent from the BE, mainly due to spending on major subsides. Outgoes on food subsidy in RE were over three and half times of the BE (2.2 per cent of GDP) because of distribution of free foodgrains to over 80 crore people and on-budgeting of past subsidy payments to the Food Corporation of India (FCI) in the form of National Small Saving Fund (NSSF) loans. The revenue expenditure, excluding interest and subsidy payments, is estimated to step-up by 33.6 per cent in Q4 (Chart III.11). The capital expenditure of the central government also inched up by 6.6 per cent in RE 2020-21 from BE on the back of higher spending on central sector schemes, railways, defence, transfers to the States, health and MSMEs. Higher capital expenditure in RE that is attributed to discretionary spending gave a thrust to fixed investment in the economy. The increased government expenditure reflects the fiscal policy push necessitated by the pandemic to save lives and livelihood and nurture the economic recovery. Reflecting decline in revenues and higher expenditures, the fiscal deficit (FD) and revenue deficit (RD) edged up considerably to 9.5 per cent and 7.5 per cent of GDP, respectively in 2020-21(RE). | Table III.4: Central Government Tax Collections | | Indicator | Per cent to GDP | | 2019-20 | 2020-21

(RE) | 2021-22

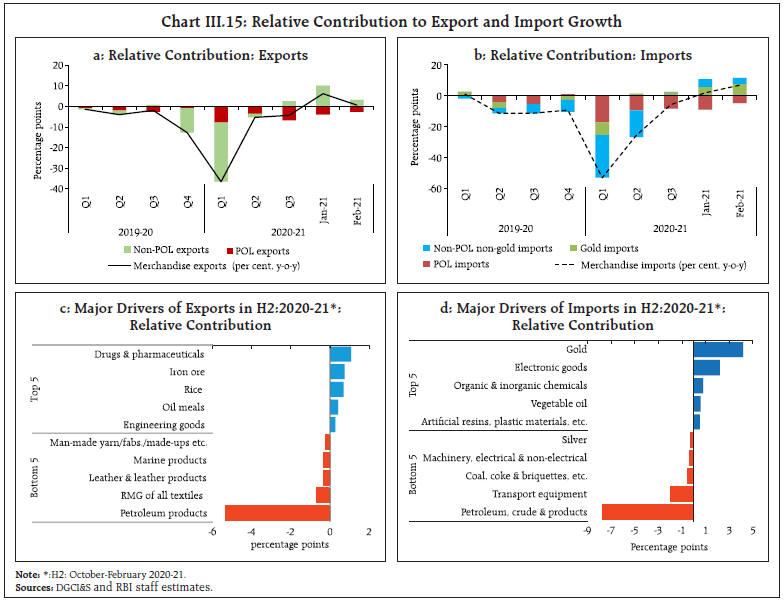

(BE) | | 1. Direct tax | 5.1 | 4.6 | 5.0 | | (i) Corporation | 2.7 | 2.3 | 2.5 | | (ii) Income | 2.4 | 2.3 | 2.5 | | 2. Indirect tax | 4.6 | 5.1 | 5.0 | | (i) GST | 2.9 | 2.6 | 2.8 | | (ii) Customs | 0.5 | 0.6 | 0.6 | | (iii) Excise | 1.2 | 1.8 | 1.5 | | 3. Gross tax revenue (1+2) | 9.7 | 9.7 | 9.9 | | 4. Net tax revenue | 6.6 | 6.9 | 6.9 | Note: BE: Budget Estimates. RE: Revised Estimates.