On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (December 7, 2022) decided to: - Increase the policy repo rate under the liquidity adjustment facility (LAF) by 35 basis points to 6.25 per cent with immediate effect.

Consequently, the standing deposit facility (SDF) rate stands adjusted to 6.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 6.50 per cent. - The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. The main considerations underlying the decision are set out in the statement below. Assessment Global Economy 2. The global economic outlook is skewed to the downside. Global growth is set to lose momentum as monetary policy actions tighten financial conditions and as consumer confidence weakens with the rising cost of livelihood. Inflation remains elevated and persistent across countries as they grapple with food and energy price shocks and shortages. More recently, however, there are some signs of moderation in price pressures, which have raised expectations of an easing in the pace of monetary tightening. Alongside easing in sovereign bond yields, the US dollar has come off its highs. Capital flows to emerging market economies (EMEs) remain volatile and global spillovers pose risks to growth prospects. Domestic Economy 3. On the domestic front, real gross domestic product (GDP) increased by 6.3 per cent year-on-year (y-o-y) in Q2:2022-23 after an increase of 13.5 per cent in Q1. On the supply side, gross value added (GVA) rose by 5.6 per cent in Q2. 4. In Q3, economic activity is exhibiting resilience. In the agricultural sector, a pick-up in rabi sowing (6.4 per cent higher than a year ago on December 2) is supported by the good progress of the north-east monsoon and above average reservoir levels. Activity in the industry and services sectors is in expansion mode, as reflected in purchasing managers’ indices (PMIs) and other high frequency indicators. 5. Aggregate demand conditions have been supported by pent-up spending and discretionary expenditures during the festival season, although their evolution is somewhat uneven across sectors. Urban demand has remained buoyant, and rural demand is recovering. Investment activity is in modest expansion. Merchandise exports contracted in October after an expansion for 19 consecutive months. Growth in non-oil non-gold imports decelerated. 6. CPI inflation moderated to 6.8 per cent (y-o-y) in October 2022 from 7.4 per cent in September, with favourable base effects mitigating the impact of pick-up in price momentum in October. Food inflation softened, aided by easing inflation in vegetables and edible oils, despite sustained pressures from prices of cereals, milk and spices. Fuel inflation registered some easing in October, driven by softening of price inflation in LPG, kerosene (PDS) and firewood and chips. Core CPI (i.e., CPI excluding food and fuel) inflation persisted at elevated levels at 6 per cent, with price pressures across most of its constituent sub-groups. 7. The overall liquidity remains in surplus, with average daily absorption under the liquidity adjustment facility (LAF) at ₹1.4 lakh crore during October-November as compared with ₹2.2 lakh crore in August-September. On a y-o-y basis, money supply (M3) expanded by 8.9 per cent as on November 18, 2022 while bank credit rose by 17.2 per cent. India’s foreign exchange reserves were placed at US$ 561.2 billion as on December 2, 2022. Outlook 8. The inflation trajectory going ahead would be shaped by both global and domestic factors. In case of food, while vegetable prices are likely to see seasonal winter correction, prices of cereals and spices may stay elevated in the near-term on supply concerns. High feed costs could also keep inflation elevated in respect of milk. Adverse climate events – both domestic and global – are increasingly becoming a significant source of upside risk to food prices. Global demand is weakening. Unabating geopolitical tensions continue to impart uncertainty to the food and energy prices outlook. The correction in industrial input prices and supply chain pressures, if sustained, could help ease pressures on output prices; but the pending pass-through of input costs could keep core inflation firm. Imported inflation risks from the US dollar movements need to be watched closely. Taking into account these factors and assuming an average crude oil price (Indian basket) of US$ 100 per barrel, inflation is projected at 6.7 per cent in 2022-23, with Q3 at 6.6 per cent and Q4 at 5.9 per cent, and risks evenly balanced. CPI inflation for Q1:2023-24 is projected at 5.0 per cent and for Q2 at 5.4 per cent, on the assumption of a normal monsoon (Chart 1). 9. On growth, the agricultural outlook has brightened, with the prospects of a good rabi harvest. The sustained rebound in contact-intensive sectors is supporting urban consumption. Robust and broad-based credit growth and government’s thrust on capital spending and infrastructure should bolster investment activity. According to the RBI’s survey, consumer confidence is improving. The economy, however, faces accentuated headwinds from protracted geopolitical tensions, tightening global financial conditions and slowing external demand. Taking all these factors into consideration, the real GDP growth for 2022-23 is projected at 6.8 per cent with Q3 at 4.4 per cent and Q4 at 4.2 per cent, with risks evenly balanced. Real GDP growth is projected at 7.1 per cent for Q1:2023-24 and at 5.9 per cent for Q2 (Chart 2).  10. Inflation has ruled at or above the upper tolerance band since January 2022 and core inflation is persisting around 6 per cent. Headline inflation is expected to remain above or close to the upper threshold in Q3 and Q4:2022-23. It is likely to moderate in H1:2023-24 but will still remain well above the target. Meanwhile, economic activity has held up well and is expected to be resilient, supported by domestic demand. Net exports would remain subdued due to the drag from evolving external demand conditions. Further, the impact of monetary policy measures undertaken needs to be watched. On balance, the MPC is of the view that, further calibrated monetary policy action is warranted to keep inflation expectations anchored, break the core inflation persistence and contain second round effects, so as to strengthen medium-term growth prospects. Accordingly, the MPC decided to increase the policy repo rate by 35 basis points to 6.25 per cent. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. 11. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to increase the policy repo rate by 35 basis points. Prof. Jayanth R. Varma voted against the repo rate hike. 12. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted against this part of the resolution. 13. The minutes of the MPC’s meeting will be published on December 21, 2022. 14. The next meeting of the MPC is scheduled during February 6-8, 2023. (Yogesh Dayal)

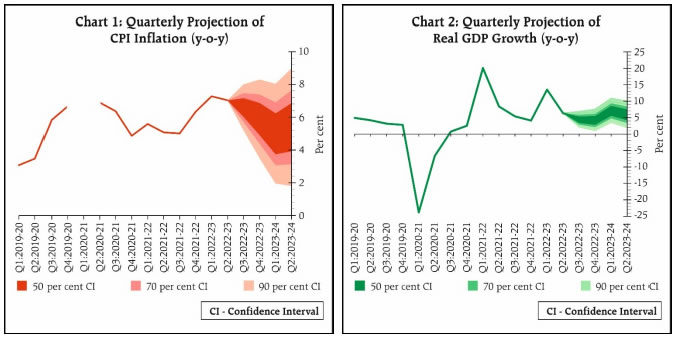

Chief General Manager Press Release: 2022-2023/1320 |