Monetary Policy Decisions After assessing the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (October 9, 2024) decided to: - Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. - The MPC also decided to change the monetary policy stance to ‘neutral’ and to remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth.

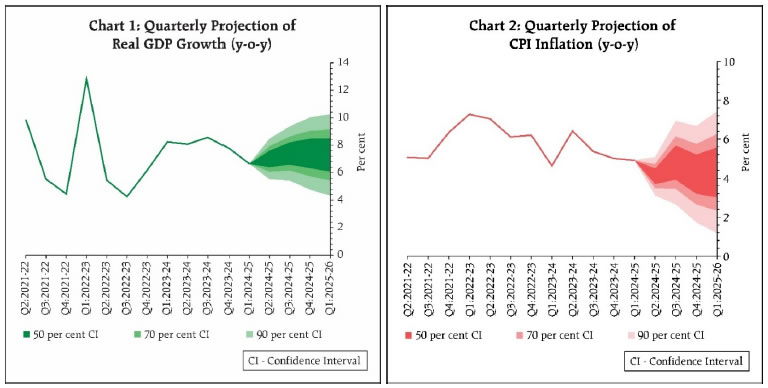

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. Growth and Inflation Outlook The global economy has remained resilient and is expected to maintain stable momentum over the rest of the year, amidst downside risks from intensifying geopolitical conflicts. In India, real gross domestic product (GDP) registered a growth of 6.7 per cent in Q1:2024-25, driven by private consumption and investment. Looking ahead, the agriculture sector is expected to perform well on the back of above normal rainfall and robust reservoir levels, while manufacturing and services activities remain steady. On the demand side, healthy kharif sowing, coupled with sustained momentum in consumer spending in the festival season, augur well for private consumption. Consumer and business confidence have improved. The investment outlook is supported by resilient non-food bank credit growth, elevated capacity utilisation, healthy balance sheets of banks and corporates, and the government’s continued thrust on infrastructure spending. External demand is expected to get support from improving global trade volumes. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent with Q2 at 7.0 per cent; Q3 at 7.4 per cent; and Q4 at 7.4 per cent. Real GDP growth for Q1:2025-26 is projected at 7.3 per cent (Chart 1). The risks are evenly balanced. Headline inflation declined sharply to 3.6 and 3.7 per cent in July and August respectively from 5.1 per cent in June. Going forward, the September inflation print may see a significant pick-up as base effects turn adverse and food prices register an upturn. Food inflation, however, is expected to ease by Q4:2024-25 on better kharif arrivals and rising prospects of a good rabi season. Sowing of key kharif crops are higher than last year and the long-period average. Sufficient buffer stocks for cereals are available for ensuring food security. Adequate reservoir levels, the likelihood of a good winter and favorable soil moisture conditions augur well for the ensuing rabi season, though adverse weather events remain a risk. Firms polled in the Reserve Bank enterprise surveys expect input cost pressures to ease; however, the very recent upturn in key commodity prices, especially metals and crude oil needs to be closely monitored. Taking all these factors into consideration, CPI inflation for 2024-25 is projected at 4.5 per cent with Q2 at 4.1 per cent; Q3 at 4.8 per cent; and Q4 at 4.2 per cent. CPI inflation for Q1:2025-26 is projected at 4.3 per cent (Chart 2). The risks are evenly balanced.  Rationale for Monetary Policy Decisions The MPC noted that the domestic growth outlook remains resilient supported by domestic drivers – private consumption and investment. This provides headroom for monetary policy to focus on the goal of attaining a durable alignment of inflation with the target. The MPC reiterates that enduring price stability strengthens the foundations of a sustained period of high growth. After a transient spike in the near term, headline inflation is expected to moderate as projected above. With better prospects for both kharif and rabi crops and ample buffer stocks of foodgrains, there is now greater confidence on the disinflation path later in the financial year. Keeping in view the prevailing and expected inflation-growth dynamics, which are well balanced, the MPC decided to change the monetary policy stance from withdrawal of accommodation to ‘neutral’ and remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth. The change in stance provides flexibility to the MPC while enabling it to monitor the progress on disinflation which is still incomplete. Risks stem from uncertainties relating to heightened global geo-political risks, financial market volatility, adverse weather events and the recent uptick in global food and metal prices. Hence, the MPC has to remain vigilant of the evolving inflation outlook. Accordingly, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. Shri Saugata Bhattacharya, Professor Ram Singh, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Dr. Nagesh Kumar voted to reduce the policy repo rate by 25 basis points. Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Professor Ram Singh, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted for a change in stance from withdrawal of accommodation to ‘neutral’ and to remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth. The minutes of the MPC’s meeting will be published on October 23, 2024. The next meeting of the MPC is scheduled during December 4 to 6, 2024.

|