RBI/DOR/2025-26/326

DOR.CRE.REC.245/07-03-007/2025-26 November 28, 2025 Reserve Bank of India (All India Financial Institutions - Concentration Risk Management) Directions, 2025 In exercise of the powers conferred by Section 45L of the Reserve Bank of India Act, 1934, and all other provisions / laws enabling the Reserve Bank of India ('RBI') in this regard, RBI being satisfied that it is necessary and expedient in the public interest so to do, hereby, issues the Directions hereinafter specified. Chapter I - Preliminary A. Short Title and Commencement 1. These Directions shall be called the Reserve Bank of India (All India Financial Institutions - Concentration Risk Management) Directions, 2025. 2. These Directions shall come into effect immediately upon issuance. B. Applicability 3. These Directions shall be applicable to All India Financial Institutions (hereinafter collectively referred to as 'AIFIs' and individually as an 'AIFI') viz. Export Import Bank of India ('EXIM Bank'), National Bank for Agriculture and Rural Development ('NABARD'), Small Industries Development Bank of India ('SIDBI'), National Housing Bank ('NHB') and National Bank for Financing Infrastructure and Development ('NaBFID'). C. Definitions 4. In these Directions, unless the context states otherwise, the terms herein shall bear the meaning as assigned to them in the ensuing paragraphs. (1) "Central counterparty" or "CCP" means a system provider, who by way of novation interposes between system participants in the transactions admitted for settlement, thereby becoming the buyer to every seller and the seller to every buyer, for the purpose of effecting settlement of their transactions. (2) "Clearing member" means a member of, or a direct participant in, a CCP that is entitled to enter into a transaction with the CCP, regardless of whether it enters into trades with a CCP for its own hedging, investment or speculative purposes or whether it also enters into trades as a financial intermediary between the CCP and other market participants. Explanation: For the purpose of these Directions, where a CCP has a link to a second CCP, that second CCP is to be treated as a clearing member of the first CCP. Whether the second CCP's collateral contribution to the first CCP is treated as initial margin or a default fund contribution will depend upon the legal arrangement between the CCPs. In such cases, if any, the Reserve Bank should be consulted for determining the treatment of this initial margin and default fund contributions. (3) "Control" shall have the same meaning as assigned to it under clause (27) of Section 2 of the Companies Act, 2013 as amended from time to time. (4) "Derivative" shall have the same meaning as assigned to it in Section 45U(a) of the Reserve Bank of India Act, 1934. (5) "Eligible capital base" for the purposes of these Directions is the effective amount of Tier 1 capital fulfilling the criteria defined under Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025, as per the last audited balance sheet. The infusion of capital after the published balance sheet date may also be taken into account for the purpose of exposure norms. Further, profits accrued during the year will be reckoned as Tier I capital for the purpose after making necessary adjustments as prescribed under Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025. Provided that the AIFI shall obtain an external auditor's certificate on completion of the infusion of capital and submit the same to the RBI (DOS) before reckoning the additions to eligible capital base. (6) "Infrastructure projects / infrastructure lending" means any credit facility in whatever form extended by an AIFI to any infrastructure facility that is a project in any of the sectors incorporated in the latest updated Harmonized Master List of Infrastructure Sub-sectors published by the Government of India. (7) "Large Exposure" means the sum of all exposure value of an AIFI measured in terms of paragraphs 25 to 43 of these Directions, to a counterparty and / or a group of connected counterparties, if it is equal to or above 10 per cent of the AIFI's eligible capital base. (8) "Net worth" shall have the same meaning as assigned to it under clause (57) of Section 2 of Companies Act, 2013 as amended from time to time. (9) "Qualifying central counterparty" or "QCCP" means an entity that is licensed to operate as a CCP (including a license granted by way of confirming an exemption) and is permitted by the appropriate regulator / overseer to operate as such with respect to the products offered. This is subject to the provision that the CCP is based and prudentially supervised in a jurisdiction where the relevant regulator / overseer has established, and publicly indicated that it applies to the CCP on an ongoing basis, domestic rules and regulations that are consistent with the CPSS-IOSCO Principles for Financial Market Infrastructures. (10) "Subsidiary" shall have the same meaning as assigned under the extant Accounting Standards. (11) "Trade exposures" include the current and potential future exposure of a clearing member or a client to a CCP arising from OTC derivatives, exchange traded derivatives transactions or SFTs, and initial margin. For the purpose of this definition, the current exposure of a clearing member includes the variation margin due to the clearing member but not yet received. 5. All other expressions, unless defined herein, shall have the same meaning as have been assigned to them under the Banking Regulation Act, 1949 or the Reserve Bank of India Act, 1934 or the Companies Act, 2013, or any statutory modification or re-enactment thereto or other regulations issued by the Reserve Bank of India or the Glossary of Terms published by Reserve Bank or as used in commercial parlance, as the case may be. Chapter II - Large Exposures Framework A. Role of the Board 6. An AIFI shall formulate comprehensive Board-approved policies on the Large Exposures Framework that, inter alia, include provisions: (1) to determine credit exposure limits of its refinancing portfolio; (2) conditions under which exposure beyond 20 per cent of its eligible capital base to a single counterparty shall be permitted; (3) determining connectedness among counterparties; and (4) adopting internal ceiling, within the regulatory prescribed ceiling, for aggregate investment in equity of non-financial / commercial enterprises. 7. Additionally, an AIFI shall place an annual review of the implementation of exposure management measures before the Board by the end of June (September in the case of NHB). B. Scope 8. An AIFI shall apply the large exposure norms on an ongoing basis and in the same manner as applied for the risk-based capital requirements, i.e. (a) consolidated / Group level (after consolidating the assets and liabilities of its subsidiaries / joint ventures / associates, including overseas operations through AIFI's branches, except those engaged in insurance and any non-financial activities), and (b) solo level. These norms deal with only the counterparty exposures but not with the sector / industry exposures. C. Exemptions 9. An AIFI's exposure to all its counterparties shall be subject to the exposure limits as prescribed in Section D of this Chapter, except for those listed below: (1) The refinance portfolios of the AIFI. Provided that the AIFI shall frame a policy approved by its Board to determine credit exposure limits in respect of its refinancing portfolio. The policy framed and assessments made under such a policy shall be subject to supervisory scrutiny. (2) Exposures to the Government of India and State Governments which are eligible for zero per cent risk weight under Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025. (3) Exposures to the RBI. (4) Exposures where principal and interest are fully guaranteed by the Government of India. (5) Exposures secured by financial instruments issued by the Government of India, to the extent that the eligibility criteria for recognition of the credit risk mitigation (CRM) are met in terms of paragraph 26. (6) Intra-day exposures to banks. (7) An AIFI's clearing activities related exposures to QCCPs as detailed in Section H of this Chapter. 10. Where two (or more) entities falling outside the scope of the sovereign exemption are controlled by or are economically dependent on an entity that falls within the scope of the sovereign exemption [paragraphs 9 (2) and (3)], and are otherwise not connected, those entities will not be deemed to constitute a group of connected counterparties. D. Exposure Ceilings D.1 Single Counterparty 11. The sum of all the exposure values of an AIFI to a single counterparty shall not be higher than 20 per cent of the AIFI's available eligible capital base at all times. Provided that Board of the AIFI may allow additional five per cent exposure beyond 20 per cent but at no time higher than 25 per cent of the AIFI's eligible capital base, subject to the following conditions: (1) the AIFI shall put in place a specific Board-approved policy setting out conditions under which exposure beyond 20 per cent may be considered; and (2) the AIFI shall record in writing the exceptional reasons for which exposure beyond 20 per cent is being allowed for each specific case. Provided further that the AIFI may exceed the exposure limit by five per cent of its Tier-I capital for exposure to a single counterparty, if the additional exposure is on account of infrastructure 'loan and / or investment'. Provided further that single counterparty limit shall not exceed 25 per cent in any case for the AIFI. D.2 Group of Connected Counterparties 12. The sum of all exposure values of an AIFI to a group of connected counterparties shall not be higher than 25 per cent of the AIFI's available eligible capital base at all times. Provided that an AIFI may exceed the exposure limit by 10 per cent of its Tier I capital for exposure to a group of connected counterparties, if the additional exposure is on account of infrastructure 'loan and / or investment'. E. Definition of connected counterparties 13. In some cases, an AIFI may have exposures to a group of counterparties with specific relationships or dependencies such that, were one of the counterparties to fail, all of the counterparties would very likely fail. Such a group of connected counterparties shall be treated as a single counterparty. The sum of the AIFI's exposure to all the individual entities included within a group of connected counterparties shall be subject to the exposure limits, as mentioned in Section D.2 above, and to the regulatory reporting requirements. 14. Two or more natural or legal persons shall be deemed to be a group of connected counterparties if at least one of the following criteria is satisfied: (1) Control relationship: one of the counterparties, directly or indirectly, has control over the other(s) or the counterparties are, directly or indirectly, controlled by a third party (an AIFI may or may not have exposure towards this third party). In case of financial problems of the controlling entity, it is highly likely that the controlling entity could make use of its ability to extract capital and / or liquidity from the controlled entity, thereby weakening the financial position of the latter. Financial problems could be transferred to the controlled entity, with the result that both the controlling entity and the controlled entity would experience financial problems (domino effect). From the prudential perspective, these types of clients (connected by control) form a single risk. (2) Economic interdependence: if one of the counterparties were to experience financial problems, in particular funding or repayment difficulties, the other(s), as a result, would also be likely to encounter funding or repayment difficulties. Provided that in order to avoid cases where a thorough investigation of economic interdependencies will not be proportionate to the size of the exposures, the AIFI shall identify possible connected counterparties on the basis of economic interdependence in all cases where the sum of all exposures to one individual counterparty exceeds five per cent of the eligible capital base, and not in other cases. 15. In order to establish the existence of a group of connected counterparties, the AIFI shall assess the relationship amongst counterparties with reference to paragraphs 14 i(1) and i(2) above. Provided that if one entity owns more than 50 per cent of the voting rights of the other entity, the AIFI shall automatically consider that the control relationship criterion [paragraph 14(1)] is satisfied. Provided further that the AIFI shall assess connectedness between counterparties based on 'control' using the following evidences: (i) Voting agreements (e.g., control of a majority of voting rights pursuant to an agreement with other shareholders); (ii) Significant influence on the appointment or dismissal of an entity's administrative, management or supervisory body, such as the right to appoint or remove a majority of members in those bodies, or the fact that a majority of members have been appointed solely as a result of the exercise of an individual entity's voting rights; (iii) Significant influence on senior management, e.g., an entity has the power, pursuant to a contract or otherwise, to exercise a controlling influence over the management or policies of another entity (e.g., through consent rights over key decisions, to decide on the strategy or direct the activities of an entity, to decide on crucial transactions such as transfer of profit or loss); and (iv) The AIFI shall also assess the above criteria with respect to a common third party (such as holding company), irrespective of whether the AIFI has exposure to that entity or not. 16. The AIFI shall also refer to criteria specified in the extant accounting standards for further qualitative guidance when determining control. 17. While determining control relationship, an AIFI shall also examine cases where clients have common owners, shareholders or managers; for example, horizontal groups where an undertaking is related to one or more other undertakings because they all have the same shareholder structure without a single controlling shareholder or because they are managed on a unified basis. This management may be pursuant to a contract concluded between the undertakings, or to provisions in the memoranda or articles of association of those undertakings, or if the administrative management or supervisory bodies of the undertaking and of one or more other undertakings consist, for the major part, of the same persons. 18. Where control has been established based on any of the above criteria, in exceptional cases, an AIFI shall have an option to demonstrate to the RBI (e.g., existence of control between counterparties due to specific circumstances and corporate governance safeguards) that such control does not necessarily result in the entities concerned constituting a group of connected counterparties. For example, in specific cases where a special purpose entity (SPE) that is controlled by another client (e.g., an originator) is fully ring-fenced and bankruptcy remote (i.e., arrangements exist to the effect that assets of SPE are not available to lenders of parent undertaking in the event of insolvency of the parent undertaking) – so that there is no possible channel of contagion. Hence no single risk exists between the special purpose entity and the controlling parent entity. 19. In establishing connectedness based on economic interdependence, the AIFI shall consider, at a minimum, the following criteria: (1) Where 50 per cent or more of one counterparty's gross receipts or gross expenditures (on an annual basis) is derived from transactions with the other counterparty; (2) Where one counterparty has fully or partly guaranteed the exposure of the other counterparty, or is liable by other means, and the exposure is so significant that the guarantor is likely to default if a claim occurs; (3) Where a significant part of one counterparty's production / output is sold to another counterparty, which cannot easily be replaced by other customers; (4) When the expected source of funds to repay the loans of both counterparties is the same and neither counterparty has another independent source of income from which the loan may be serviced and fully repaid; (5) Where it is likely that the financial problems of one counterparty would cause difficulties for the other counterparties in terms of full and timely repayment of liabilities; (6) Where the insolvency or default of one counterparty is likely to be associated with the insolvency or default of the other(s); and (7) When two or more counterparties rely on the same source for the majority of their funding and, in the event of the common provider's default, an alternative provider cannot be found - in this case, the funding problems of one counterparty are likely to spread to another due to a one-way or two-way dependence on the same main funding source. 20. The illustrative examples of Economic Interdependence Criteria are as below: (1) Requirement: Both A and B are customers of an AIFI and the exposure of the AIFI to each of them is more than five per cent of its eligible capital base (i.e. Tier-1 capital). (i) Where 50 per cent or more of one counterparty's gross receipts or gross expenditures (on an annual basis) is derived from transactions with the other counterparty; Illustrative Example: Company A is a commercial space provider and company B utilises a major portion of this space and accounts for more than 50 per cent of gross receipts for Counterparty A. (ii) Where one counterparty has fully or partly guaranteed the exposure of the other counterparty, or is liable by other means, and the exposure is so significant that the guarantor is likely to default if a claim occurs; Illustrative Example: Company A fully or partly guarantees the loans undertaken by company B and the guarantee is so large that it could result in default in payments for A if it is invoked. The AIFI may consider parameters like networth, EBITDA, liquid assets, etc., to assess whether the guarantor will be in a position to honour the claim on an on-going basis. (iii) Where a significant part of one counterparty's production / output is sold to another counterparty, which cannot easily be replaced by other customers; Illustrative Example: When a significant part of product / output / services of Company A is sold to Company B and there are no alternate buyers who can be approached if B fails to buy, in such a case goods may remain unsold and could lead to default in loan repayment by A. An auto part supplier and auto manufacturing firm could be part of the same economically dependent group based on this criteria. For deciding if the criteria would be applicable to the counterparties under consideration, the AIFI may use financial criteria like unsold inventory leading to operating loss / default in repayment as well as subjective criteria like ability of the seller to find alternate buyer / market, R&D capability of the seller, etc. (iv) When the expected source of funds to repay the loans of both counterparties is the same and neither counterparty has another independent source of income from which the loan may be serviced and fully repaid; Illustrative Example: Two auto component manufacturers i.e. company A and company B are suppliers to a commercial vehicle manufacturer i.e. company C. Source of funds for repayment of loans taken by A and B is dependent on sales to C. In this case, A and B are connected to each other based on the criteria of economic interdependence. Important factors to consider would be extent of dependence of A and B on C, ability of A and B to find another buyer, etc. (v) Where it is likely that the financial problems of one counterparty would cause difficulties for the other counterparties in terms of full and timely repayment of liabilities; Illustrative Example: Company A supplies intermediate goods to Company C. Company C processes these goods and then sells it to company B. In such cases, difficulties at A could lead to difficulties for B. In such cases A and B are economically dependent. The AIFI may consider factors like financial strength of counterparty B to withstand the shock, its ability to find alternate supplier in place of C, etc. to decide on applicability of the criteria. (vi) Where the insolvency or default of one counterparty is likely to be associated with the insolvency or default of the other(s); Illustrative Example: Examples would include all such cases where insolvency or default of one company may lead to the insolvency or default of the other companies. The AIFI may use criteria such as intercorporate liabilities, significant trade receivables, etc. to decide on applicability of the criteria. (vii) When two or more counterparties rely on the same source for the majority of their funding and, in the event of the common provider's default, an alternative provider cannot be found - in this case, the funding problems of one counterparty are likely to spread to another due to a one-way or two-way dependence on the same main funding source. Illustrative Example: Company A and Company B rely on the same non-AIFI source for their funding requirements and may not have access to alternative sources of funds. In such cases, difficulties at common source could lead to difficulties at both the companies and thus these companies are interconnected based on economic interdependence. Important factors to consider would be strength of A and B to decide alternate source of funds, likelihood of failure of the non-AIFI source, etc. (2) Economic interdependence with two different entities: If an entity (C) is economically dependent on two (or more) other entities (A and B) then payment difficulty of any one of the entities (A or B) may cause payment difficulties to dependent entity (C). Thus, C needs to be added in two different groups (A and C; B and C). Since exposure to C is considered as single risk for two separate groups, it does not amount to double counting of exposure of C. 21. However, it is possible that there shall be circumstances where some of these criteria do not automatically imply an economic dependence that results in two or more counterparties being connected. In such a scenario, the AIFI shall not be required to combine these counterparties to form a group of connected counterparties. Provided that the AIFI can demonstrate that a counterparty which is economically closely related to another counterparty shall be able to overcome financial difficulties, or even the second counterparty's default, by finding alternative business partners or funding sources within an appropriate time period. 22. Relation between interconnectedness through control and interconnectedness through economic dependency: Group of counterparties based on control and economic interdependence are to be assessed separately. However, there may be situations where the two types of dependencies are interlinked and could therefore exist within one group of connected counterparties in such a way that all relevant clients constitute a single risk. Risk of contagion is present irrespective of type of connectedness (i.e., control or economic interdependence) between counterparties. The chain of contagion leading to possible default of all entities concerned is the relevant factor for the grouping and needs to be assessed in each individual case. 23. The following examples provide illustrations for formulation of groups in case of one-way dependency and two-way dependencies. (1) One way Dependency: Consider A controls A1 and A2, and B controls B1, and B1 is economically dependent on A2 (one-way dependency only i.e. financial difficulties at A2 could impact B1 but not vice versa). In this case, B1 should be part of two separate groups of A and B. (i) Three different groups of i) A, A1, A2, ii) B, B1, iii) A2, B1, may not be sufficient as financial difficulties of A2 is likely to cause difficulties for B1 also which is economically dependent on A2 (which in turn is dependent on A). (2) Two Way Dependency: Consider that A2 and B1 have two-way economic dependency i.e. both are economically dependent on each other, which means that financial difficulty at either entity could impact the other entity. (i) Downstream Contagion: Downstream contagion should be assumed when an entity is economically dependent on another entity and is itself the head of a 'control group'. If the other entity is part of a group of connected clients, the control group of the economically dependent entity should then be included in the group of connected counterparties to which the economic dependency relationship exists. To overcome its own pending payment difficulties, the economically dependent entity is likely to withdraw resources from controlled entities, thus extending the risk of contagion downstream. Consider A controls A1 and A2, and B controls B1, and B1 controls B2 and B3. Further, consider B1 has one-way economic dependency on A2. If A2 faces financial difficulty, it may impact B1 adversely, which then is likely to withdraw resources from its controlled entities B2 and B3. Grouping requirements: (ii) Upstream Contagion: On the other hand, upstream contagion of entities that control the economically dependent entity should be assumed only when the controlling entity is also economically dependent on the entity that constitutes the economic link between the two controlling groups. For instance, in the above example of downstream contagion, if B1 is so important to B that in a sense B is also dependent on B1, then contagion at A could also spread to B, through A→A2→B1→B and all these entities would form a single group.  (iii) Limitations in formulating groups of connected counterparties: If an AIFI is not having exposure to all the entities, it may be difficult to accurately form group of connected counterparties. Such groups shall be formed on best efforts basis and the AIFI should take reasonable steps to collect and use relevant information; this includes publicly available information (e.g. annual financial statements), information beyond institutions' clients and also soft information that typically exists at the level of individual loan officers and relationship managers. If there are interconnections among entities that are not clients of the AIFI, it may be difficult for the AIFI to formulate correct groupings. However, the AIFI should incorporate any information that may be available to it publicly or through other clients or entities outside its clientele. For instance, in illustration shown below, if an AIFI has exposure to A and B5 only, then it may be difficult to formulate correct groupings. 24. The AIFI shall frame a Board-approved policy for determining connectedness using the criteria mentioned above. The policies are subject to supervisory scrutiny. F. Values of Exposure 25. An exposure to a counterparty shall constitute both on and off-balance sheet exposures which shall be calculated according to the method prescribed for capital computation under Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025. The exposures shall be permitted to be offset with credit risk mitigation techniques permitted in Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025, Off-balance sheet items shall be converted into credit exposure equivalents through the use of credit conversion factors (CCFs) by applying the CCFs set out the Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025, with a floor of 10 per cent. F.1 Recognition of exposures to CRM providers 26. Where an AIFI reduces its exposure to the original counterparty on account of an eligible CRM instrument provided by another counterparty (CRM provider) with respect to that exposure, it shall also recognise an exposure to the CRM provider. The amount assigned to the CRM provider will be the amount by which the exposure to the original counterparty is reduced (except in the cases defined in paragraph 27 below). 27. When the credit protection takes the form of a credit default swap (CDS) and either the CDS provider or the referenced entity is not a financial entity, the amount to be assigned to the credit protection provider is not the amount by which the exposure to the original counterparty is reduced but will be equal to the counterparty credit risk exposure value calculated as per the extant method prescribed for the counterparty credit risk in Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025. Explanation: For the purpose of this paragraph, financial entities comprise: (i) Regulated financial institutions, defined as a parent and its subsidiaries where any substantial legal entity in the consolidated group is supervised by a regulator that imposes prudential requirements consistent with international norms. These include, but are not limited to, prudentially regulated insurance companies, broker / dealers, banks; and (ii) Unregulated financial institutions, defined as legal entities whose main business includes: the management of financial assets, lending, factoring, leasing, provision of credit enhancements, securitisation, investments, financial custody, central counterparty services, proprietary trading and other financial services activities identified by supervisors. F.2 Exposures to banks 28. The exposures to banks (excluding refinance exposure), except intra-day exposures, shall be subject to the large exposure limit of 25 per cent of an AIFI's Tier 1 capital. F.3 Collective Investment Undertakings (CIUs), securitisation vehicles and other structures - adoption of "Look Through Approach" (LTA) 29. There are cases when a structure lies between an AIFI and its exposures, that is, the AIFI invests in structures which themselves have exposures to assets underlying the structures (hereafter referred to as the "underlying assets"). Such structures include funds (such as mutual funds, alternative investment funds), securitisations and other structures (such as investment in security receipts, real estate investment trusts, infrastructure investment trusts) with underlying assets. The AIFI shall assign such exposure amount to specific counterparties of the underlying assets following the LTA described below. (1) Look-Through Approach - a flow chart (2) Look-Through Approach - An Illustrative example (i) AIFI's eligible capital base: 1000 (ii) Corpus of structure: 500 (iii) AIFI's investment in structure: 100 (which is 10 per cent of eligible capital base i.e. more than 0.25 per cent of eligible capital base) (iv) Exposure values as per look-through approach: | | Investment of structure in that underlying | AIFI's exposure to underlying through structure | AIFI's other direct / indirect exposure to underlying | Total exposure to underlying | | | Amount | as per cent of corpus | Amount | as per cent of eligible capital base | Amount | as per cent of eligible capital base | Amount | as per cent of eligible capital base | | Underlying 1 | 125 | 25.00% | 25 | 2.50% | 200 | 20.00% | 225 | 22.50% | | Underlying 2 | 10 | 20.00% | 20 | 2.00% | 150 | 15.00% | 170 | 17.00% | | Underlying 3 | 90 | 18.00% | 18 | 1.80% | 100 | 10.00% | 118 | 11.80% | | Underlying 4 | 75 | 15.00% | 15 | 1.50% | 80 | 8.00% | 95 | 9.50% | | Underlying 5 | 50 | 10.00% | 10 | 1.00% | 70 | 7.00% | 80 | 8.00% | | Underlying 6 | 30 | 6.00% | 6 | 0.60% | 50 | 5.00% | 56 | 5.60% | | Underlying 7 | 20 | 4.00% | 4 | 0.40% | 100 | 10.00% | 104 | 10.40% | | Underlying 8 | 10 | 2.00% | 2 | 0.20% | 150 | 15.00% | 152 | 15.20% | Note: (a) Exposure to underlying 8 (which is less than 0.25 per cent of eligible capital base) may be counted as exposure on structure itself. Consequently, for underlying 8 total exposure to underlying will be 15.00 per cent or 15.20 per cent at the option of the AIFI. (b) Had the AIFI been not able to identify underlying exposures, entire exposure to the structure (i.e. 100, which is greater than 0.25 per cent of eligible capital base) would be exposure on 'unknown client'. All such unknown clients would be treated as a single counterparty and single counterparty limit would apply on aggregate exposure to all such unknown clients. 30. The AIFI shall be permitted to assign the exposure amount to the structure itself, defined as a distinct counterparty: Provided that it can demonstrate that the AIFI's exposure amount to each underlying asset of the structure is smaller than 0.25 per cent of its eligible capital base, considering only those exposure to underlying assets that result from the investment in the structure itself and using the exposure value calculated according to paragraphs 35 and 36. In this case, an AIFI is not required to look through the structure to identify the underlying assets. 31. The AIFI shall look through the structure and in the case of underlying assets for which the underlying exposure value is equal to or above 0.25 per cent of its eligible capital base, the counterparty corresponding to each of the underlying assets shall be identified so that these underlying exposures can be added to any other direct or indirect exposure to the same counterparty. The AIFI's exposure amount to the underlying assets that are below 0.25 per cent of the AIFI's eligible capital base shall be assigned to the structure itself (i.e., partial look-through is permitted). 32. If the AIFI is unable to identify the underlying assets of a structure: (1) where the total amount of an AIFI's exposures to a structure does not exceed 0.25 per cent of its eligible capital base, it shall assign the total exposure amount to the structure itself, as a distinct counterparty. (2) Otherwise (i.e., if the exposure to the structure equals or exceeds 0.25 per cent of its eligible capital base), it shall assign this total exposure amount to the 'unknown client'. Provided that the exposure limits shall apply on the aggregate of all such exposures to 'unknown clients' as if they are a single counterparty. 33. Where the LTA is not required (paragraph 30 above), the AIFI shall demonstrate that regulatory arbitrage considerations have not influenced the decision whether to look through or not – e.g. that the AIFI has not circumvented the exposure limits by investing in several individually immaterial transactions with identical underlying assets. 34. If LTA need not be applied, an AIFI's exposure to the structure shall be the nominal amount it invests in the structure. 35. Any structure where all investors rank pari passu (e.g., CIU): When the LTA is required according to the sections above, the exposure value assigned to a counterparty is equal to the pro rata share that the AIFI holds in the structure multiplied by the value of the underlying asset in the structure. Thus, an AIFI holding a ₹1 investment in a structure, which invests in 20 assets each with a value of ₹5, shall assign an exposure of ₹0.05 to each of the counterparties. An exposure to such counterparty shall be added to any other direct or indirect exposures the AIFI has to that counterparty. 36. Any structure with different seniority levels among investors (e.g., securitisation vehicles): When the LTA (in terms of sections above) is required for an investment in a structure with different levels of seniority, the exposure value to a counterparty shall be measured for each tranche within the structure, assuming a pro rata distribution of losses amongst investors in a single tranche. To compute the exposure value to the underlying asset, an AIFI shall: (1) first, consider the lower of the value of the tranche in which the AIFI has invested and the nominal value of each underlying asset included in the underlying portfolio of assets (2) second, apply the pro rata share of the AIFI's investment in the tranche to the value determined in the first step above. 37. Identification of additional risks: (1) While taking exposures to structures, an AIFI shall identify such third parties which may constitute an additional risk factor, and which are inherent in the structure itself rather than in the underlying assets. Such a third party could be a risk factor for more than one structure that the AIFI invests in. Examples of roles played by third parties include originator, fund manager, liquidity provider and credit protection provider. The RBI as a part of its Pillar 2 supervisory review and evaluation process will look into this aspect and if required specify a specific course of action which may either include reduction in exposure or raising of additional capital. (2) It is conceivable that an AIFI may consider multiple third parties to be potential drivers of additional risk. In this case, the AIFI shall assign the exposure resulting from the investment in the relevant structures to each of the third parties. G. Exposures to NBFCs 38. An AIFI's exposure to NBFCs (excluding refinance exposure) shall be subject to the single and group of connected counterparty limits prescribed in paragraphs 11 and 12. H. Exposures to Central Counterparties 39. An AIFI's clearing exposure to QCCPs shall be exempt from the large exposures framework. However, these exposures shall be subject to the regulatory reporting requirements as prescribed in paragraph 48. 40. In the case of non-QCCPs, the AIFI shall measure its exposure as a sum of both the clearing exposures described in paragraph 42 and the non-clearing exposures described in paragraph 43, and the same shall be subject to the large exposure limit of 25 per cent of the eligible capital base. 41. The concept of connected counterparties described in paragraphs 13 to 24 does not apply in the context of exposures to CCPs that are specifically related to clearing activities. H.1 Calculation of exposures related to clearing activities 42. An AIFI shall identify exposures to a CCP related to clearing activities and sum together these exposures. The AIFI shall determine the counterparty to which exposures shall be assigned by applying the provisions of the risk-based capital requirements. Exposures related to clearing activities are listed in the table below together with the exposure value to be used: | Trade exposures | The exposure value of trade exposures shall be calculated using the exposure measures prescribed in other parts of these Directions for the respective type of exposures. | | Segregated initial margin | The exposure value is 0.

Explanation: When the initial margin (IM) posted is bankruptcy-remote from the CCP – in the sense that it is segregated from the CCP's own accounts, e.g., when the IM is held by a third-party custodian – this amount cannot be lost by the AIFI if the CCP defaults; therefore, the IM posted by the AIFI can be exempted from the large exposure limit. | | Non-segregated initial margin | The exposure value is the nominal amount of initial margin posted. | | Pre-funded default fund contributions | Nominal amount of the funded contribution. | | Unfunded default fund contributions | The exposure value is 0. | H.2 Other exposures 43. Other types of exposures that are not directly related to clearing services provided by the CCP, such as equity stake (If equity stakes in a CCP are deducted from the capital on which the large exposure limit is based, these shall not be included as exposure to the CCP), funding facilities, credit facilities, guarantees etc., shall be measured according to the rules set out in this framework, as for any other type of counterparty. These exposures will be added together and be subjected to the large exposure limit of 25 per cent of the eligible capital base. I. Reporting System and Disclosures 44. The AIFI shall undertake an annual review of the implementation of exposure management measures and place the same before its Board by the end of June (September in the case of NHB). A copy of the review report shall be forwarded to the concerned office of Department of Supervision. I.1 Breach 45. Breach of exposure limits, if any, shall be under exceptional conditions beyond the control of an AIFI, and needs to be rectified immediately. The breaches shall be reported to RBI (Department of Supervision, Central Office) immediately. 46. The AIFI, if under breach of exposure limits, cannot undertake any further exposure (at the entity or group level, as the case may be) until it is brought down within the limit. 47. Failure to comply with the exposure limit may lead to imposition of penalties on the AIFI by the supervisor. I.2 Regulatory reporting 48. The AIFI shall report its Large Exposures to the RBI (DOS, CO) as per the reporting template given in Annex I on a monthly basis. The reporting shall cover the following: (1) All exposures, meeting the definition of large exposure. (2) All other exposures, measured without offsetting exposure value with credit risk mitigation instruments, meeting the definition of large exposure. (3) All the exempted exposures meeting the definition of large exposure. (4) 20 largest exposures included in the scope of application, irrespective of the values of these exposures relative to the AIFI's eligible capital base. Chapter III – Other Permitted exposures and Prudential Limits A. Permitted exposures and limits 49. In addition to limiting exposures to a single borrower or a group of borrowers, an AIFI shall consider fixing internal limits for aggregate commitments to specific sectors e.g., textiles, chemicals, engineering, etc., to ensure diversified sectoral exposure. These sectoral limits shall be fixed based on the AIFI's assessment of perceived risks and performance of different sectors. The AIFI shall review and revise these limits periodically, as deemed appropriate. B. Cross Holding of Capital among Banks / Financial Institutions 50. An AIFI shall be guided by the Reserve Bank of India (All India Financial Institutions – Prudential Norms on Capital Adequacy) Directions, 2025. C. Exposure to capital markets C.1 Components of Capital Market Exposure (CME) 51. An AIFI's aggregate capital market exposure shall include both its direct and indirect exposures and shall constitute of the following: (1) direct investment in equity shares, convertible bonds, convertible debentures and units of equity-oriented mutual funds the corpus of which is not exclusively invested in corporate debt; (2) advances against shares / bonds / debentures or other securities or on clean basis to individuals for investment in shares (including IPOs / ESOPs), convertible bonds, convertible debentures, and units of equity-oriented mutual funds; (3) advances for any other purposes where shares or convertible bonds or convertible debentures or units of equity oriented mutual funds are taken as primary security; (4) advances for any other purposes to the extent secured by the collateral security of shares or convertible bonds or convertible debentures or units of equity oriented mutual funds i.e. where the primary security other than shares / convertible bonds / convertible debentures / units of equity oriented mutual funds does not fully cover the advances; (5) secured and unsecured advances to stockbrokers and guarantees issued on behalf of stockbrokers and market makers; (6) loans sanctioned to corporates against the security of shares / bonds / debentures or other securities or on clean basis for meeting promoter's contribution to the equity of new companies in anticipation of raising resources; (7) bridge loans to companies against expected equity flows / issues; and (8) all exposures to Alternative Investment Funds. C.2 Limit on aggregate exposure to capital markets and investments in non-financial / commercial enterprises C.2.1 Limit on aggregate exposure to capital markets 52. The aggregate exposure of an AIFI to the capital markets in all forms (both fund based and non-fund based, direct and indirect), on solo as well as consolidated basis shall not exceed 40 per cent of its net worth, as on March 31 of the previous year. Provided that the AIFI's direct exposure within this overall ceiling shall not exceed 20 per cent of its net worth. C.2.2 Limits on significant equity investments in non-financial / commercial enterprises 53. An AIFI's equity investment in a single company that is made in conformity with its statutory mandate shall not exceed 49 per cent of the equity of the investee company. Provided that in all other cases, the AIFI shall not hold more than 10 per cent of the equity of the investee company as direct investment. 54. An AIFI shall be permitted to hold up to 49 per cent of equity of a company as a pledgee. Provided that if the AIFI ends up acquiring this in satisfaction of its claims, it shall be brought down below 10 per cent limit within 3 years. C.2.3 Limits on aggregate exposure to capital markets 55. An AIFI's aggregate investment in equity of non-financial / commercial enterprises, other than that covered under paragraph 53, shall not exceed 10 per cent of the AIFI's net worth as on March 31 of the previous year. Provided that the Board of the AIFI shall have the freedom to adopt a lower ceiling for the AIFI, keeping in view its overall risk profile and corporate strategy. C.3 Exemptions 56. The following items shall be exempted from the capital market exposure limits: (1) An AIFI's investments in own subsidiaries, joint ventures, State Finance Corporations (SFCs) and investments in shares and convertible debentures, convertible bonds issued by institutions forming crucial financial infrastructure such as Acuité Ratings & Research Limited (Acuité), India SME Technology Services Ltd (ISTSL), India SME Asset Reconstruction Company Ltd (ISARC), North Eastern Development Finance Corporation Ltd (NeDFi), National Securities Depository Ltd. (NSDL), Central Depository Services (India) Ltd. (CDSL), National Stock Exchange (NSE), NSE Clearing Ltd., Clearing Corporation of India Ltd., (CCIL), a credit information company which has obtained Certificate of Registration from the RBI and of which the AIFI is a member, Multi Commodity Exchange of India Ltd. (MCX), National Commodity and Derivatives Exchange Ltd. (NCDEX), Indian Commodity Exchange Ltd., National Commodities Management Services Ltd. (NCML), National Payments Corporation of India (NPCI) and other Public Finance Institutions (PFIs) as defined under Section 2 (72) of Companies Act, 2013. After listing, the exposures in excess of the original investment (i.e., prior to listing) would form part of the Capital Market Exposure. (2) Tier I and Tier II debt instruments issued by banks / other AIFIs; (3) Investment in Certificate of Deposits (CDs) of banks / other AIFIs; (4) Preference Shares; (5) Non-convertible debentures and non-convertible bonds; (6) Units of Mutual Funds under schemes where the corpus is invested exclusively in debt instruments; (7) Shares acquired by the AIFI as a result of conversion of debt / overdue interest into equity as per the exemption provided under the Reserve Bank of India (All India Financial Institutions – Resolution of Stressed Assets) Directions, 2025, applicable to the AIFI, as amended from time to time; (8) Promoters' shares in the SPV of an infrastructure project pledged to the lending AIFI for infrastructure project lending; and (9) Exposure to brokers under the currency derivatives segment. C.4 Computation of exposure 57. For computing the exposure to the capital markets, loans / advances sanctioned shall be reckoned with reference to sanctioned limits or outstanding, whichever is higher. Provided that in the case of fully drawn term loans, where there is no scope for re-drawal of any portion of the sanctioned limit, an AIFI shall reckon the outstanding as the exposure. 58. The AIFI's direct investment in shares, convertible bonds, convertible debentures and units of equity-oriented mutual funds shall be calculated at their cost price. Chapter IV - Repeal and other provisions A. Repeal and saving 59. With the issue of these Directions, the existing Directions, instructions, and guidelines relating to Concentration Risk Management as applicable to All India Financial Institutions stand repealed, as communicated vide circular DOR.RRC.REC.302/33-01-010/2025-26 dated November 28, 2025. The Directions, instructions and guidelines already repealed shall continue to remain repealed. 60. Notwithstanding such repeal, any action taken or purported to have been taken, or initiated under the repealed Directions, instructions, or guidelines shall continue to be governed by the provisions thereof. All approvals or acknowledgments granted under these repealed lists shall be deemed as governed by these Directions. Further, the repeal of these directions, instructions, or guidelines shall not in any way prejudicially affect: (1) any right, obligation or liability acquired, accrued, or incurred thereunder; (2) any, penalty, forfeiture, or punishment incurred in respect of any contravention committed thereunder; (3) any investigation, legal proceeding, or remedy in respect of any such right, privilege, obligation, liability, penalty, forfeiture, or punishment as aforesaid; and any such investigation, legal proceedings or remedy may be instituted, continued, or enforced and any such penalty, forfeiture or punishment may be imposed as if those directions, instructions, or guidelines had not been repealed. B. Application of other laws not barred 61. The provisions of these Directions shall be in addition to, and not in derogation of the provisions of any other laws, rules, regulations or directions, for the time being in force. C. Interpretations 62. For the purpose of giving effect to the provisions of these Directions or in order to remove any difficulties in the application or interpretation of the provisions of these Directions, the RBI may, if it considers necessary, issue necessary clarifications in respect of any matter covered herein and the interpretation of any provision of these Directions given by the RBI shall be final and binding. (Vaibhav Chaturvedi)

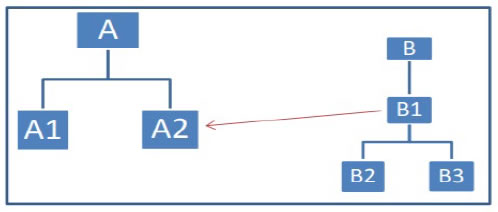

Chief General Manager |