Executive Summary Global growth remained resilient but below its historical average, with AI-driven investment and accommodative financial conditions somewhat offsetting tariff and geopolitical headwinds. Renewed inflation risks, driven by energy prices and volatile financial markets impart greater uncertainty to the global macroeconomic and financial outlook. Amidst heightened uncertainty and volatile capital flows, domestic financial markets fluctuated intermittently in the second half of 2025-26. System liquidity remained in surplus during H2. Money market rates evolved largely in sync with system liquidity and monetary policy actions. A combination of domestic and global cues hardened long-term government bond yields and rendered equity markets volatile. The depreciation pressures in INR accentuated at the tail end of H2, breaching its previous record lows amidst concerns over West Asia conflict. While bank credit growth continued to improve and remained supportive of real economic activity, financing from non-bank sources also increased. Transmission of the policy rate to both lending and deposit rates continued in H2 and remained robust during the current easing cycle, albeit with some frictions. In recent months, the combination of sustained credit demand and persistent gap between credit and deposit growth prompted banks to increase their term deposit rates, in addition to resource mobilisation through certificate of deposits, to bridge the funding gap. Domestic economic activity also remained resilient in the second half of 2025–26, primarily driven by private consumption, supported by both rural and urban demand, GST rate rationalisation and monetary easing. Structural reforms, favourable financial conditions and government’s thrust on infrastructure spending aided investment activity. On the supply side, services remained buoyant, and manufacturing strengthened, although agricultural activity moderated due to weather disruptions. The underlying momentum in economic activity, buoyed by further progress on trade deals with major economies, bodes well for India’s overall growth outlook. Global headwinds from geopolitical tensions, volatile commodity prices and supply-chain disruptions pose downside risks to the outlook. Specifically, intensification of the West Asia conflict could strain input supplies to various downstream sectors that may be growth inhibiting. Headline inflation in India increased from historical low levels seen in October 2025 but remained below the target thereafter. The pick-up in inflation was driven by the food group where the waning of base effects led to a turnaround from deflation. Fuel group inflation remained moderate and core inflation remained contained barring precious metals. Major methodological changes brought about by the introduction of the new series have significant implications for inflation, such as higher food group inflation and lower core. The realised cost conditions: input costs, wage costs, and margins showed no major pressures up to February 2026. Contribution of imported inflation, however, has been rising and imported input cost pressures have accentuated in March. The impact of conflict-driven spikes in global energy prices is also likely through multiple channels. Going forward, India’s macroeconomic outlook remains resilient despite elevated geopolitical tensions and lingering global trade frictions. Strong fundamentals, including sustained growth, low inflation, and fiscal consolidation, provides India the wherewithal to withstand the adverse impact of heightened global uncertainties. The surge in global crude oil prices since the West Asia conflict, exacerbated by significant supply disruptions, have tilted risks to inflation on the upside and growth on the downside, which have been communicated through asymmetric fan charts, scenario, and sensitivity analysis. In navigating through these turbulent times, monetary policy in India will continue to focus on reinforcing price stability while remaining growth supportive.

I. External Environment Global growth remains below its long‑term average amidst prolonged geopolitical tensions and trade‑related uncertainty. AI‑related investment and still‑accommodative financial conditions are supporting activity, even as bouts of heightened asset price volatility reflect shifting market sentiment. Monetary policy stances in major economies remain cautious, with central banks closely monitoring these developments. Recent energy price increases due to the West Asia conflict have heightened upside inflation risks and clouded the global growth outlook. Global growth was revised upwards by multilateral agencies prior to the onset of the West Asia conflict. However, in its March Economic Outlook, the Organisation for Economic Co-operation and Development (OECD) retained its 2026 growth projection but marginally trimmed its 2027 forecast, reflecting increased medium‑term risks from the conflict. Global growth is still projected to remain below its historical average. The outlook is highly contingent on the evolving situation in West Asia: an early resolution would likely limit the damage, whereas further escalation and a protracted conflict could have a more severe impact on the global economy. At the same time, ongoing trade and policy imbroglio is reinforcing uncertainty about the outlook. Inflation outcomes remain mixed, with some key advanced economies (AEs) remaining above target amidst renewed price pressures, fuelling expectations of a faster than anticipated pivot towards policy tightening. Global equity markets have remained largely resilient, mainly supported by AI‑related technology stocks. Concerns about stretched valuations, potential spillovers on other software industries, and escalating geopolitical tensions have, however, generated episodes of turbulence. The US dollar generally depreciated till February which eased financing conditions for emerging market economies (EMEs), but strengthened after the outbreak of the West Asia conflict on safe-haven demand. Gold repeatedly scaled new highs on safe-haven demand and central bank buying, but much of the gain reversed as the West Asia conflict intensified and the dollar strengthened. Base metal prices have increased on the back of supply disruptions and a strong demand outlook. I.1 Global Economic Conditions In 2025, global economic activity displayed resilience despite high tariffs, elevated policy uncertainty and geopolitical tensions as the overall impact of tariff measures turned out to be less severe than initially anticipated. US trade deals with major partners provided relief, but the US Supreme Court’s tariff ruling, and subsequent new tariff announcements in February, have rekindled uncertainty. In its January 2026 World Economic Outlook update, the International Monetary Fund (IMF) revised up its global growth projection for 2026 by 20 bps to 3.3 per cent, mainly reflecting stronger AI-related investment and fiscal spending. It kept its 2027 projection unchanged at 3.2 per cent. After the outbreak of the conflict, the OECD presented a more cautious picture. In its March economic outlook, it retained its growth forecast at 2.9 per cent for 2026 as the adverse effects of the West Asia conflict are expected to be offset by strong momentum in tech related investment and supportive fiscal and monetary policies. However, it marginally lowered its 2027 projection by 10 bps to 3.0 per cent. Among key AEs, US real GDP growth fluctuated over the course of 2025, reflecting the impact of tariff uncertainty, geopolitical tensions, and the partial government shutdown in the fourth quarter. The underlying economic activity, however, remained broadly resilient. After strong growth in Q3:2025, GDP growth decelerated in Q4, falling short of expectations due to weaker exports and lower government spending (Table I.1). Since October 2025, nonfarm payroll gains have slowed markedly, while the unemployment rate has remained broadly stable. In March, the composite PMI declined to its 2023 lows, as robust manufacturing activity was offset by a contraction in services. Consumer sentiment, as measured by the University of Michigan survey, improved for three consecutive months through February before easing slightly in March. It, however, remains subdued relative to historical standards as inflation and job worries remain persistent. | Table I.1: Real GDP Growth | | (Per cent) | | Country | Q1-2025 | Q2-2025 | Q3-2025 | Q4-2025 | 2025(E) | 2026(P) | 2027(P) | | Quarter-on-quarter, seasonally adjusted, annualised rate (q-o-q, saar) | | Canada | 2.1 | -0.9 | 2.4 | -0.6 | 1.6 | 1.6 | 1.9 | | Euro area | 2.4 | 0.6 | 1.2 | 0.8 | 1.4 | 1.3 | 1.4 | | Japan | 1.1 | 2.4 | -2.6 | 1.3 | 1.1 | 0.7 | 0.6 | | South Korea | -0.9 | 2.7 | 5.4 | -0.6 | 1.0 | 1.9 | 2.1 | | UK | 2.6 | 0.8 | 0.3 | 0.2 | 1.4 | 1.3 | 1.5 | | US | -0.6 | 3.8 | 4.4 | 0.7 | 2.1 | 2.4 | 2.0 | | Year-on-year | | Brazil | 3.2 | 2.4 | 1.8 | 1.8 | 2.5 | 1.6 | 2.3 | | China | 5.4 | 5.2 | 4.8 | 4.5 | 5.0 | 4.5 | 4.0 | | India | 7.0 | 6.7 | 8.4 | 7.8 | 7.3 | 6.4 | 6.4 | | Indonesia | 4.9 | 5.1 | 5.0 | 5.4 | 5.0 | 5.1 | 5.1 | | Philippines | 5.4 | 5.5 | 3.9 | 3.0 | 5.1 | 5.6 | 5.8 | | Russia | 1.4 | 1.1 | 0.6 | | 0.6 | 0.8 | 1.0 | | South Africa | 0.9 | 0.7 | 2.1 | 0.8 | 1.3 | 1.4 | 1.5 | | Thailand | 3.1 | 2.8 | 1.2 | 2.5 | 2.1 | 1.6 | 2.2 | | Memo: | | World | 2025 (E) | 2026 (P) | 2027 (P) | | Year-on-year | | Output | 3.3 | 3.3 | 3.2 | | Trade volume | 4.1 | 2.6 | 3.1 | E: Estimate. P: Projection.

Notes: 1. India’s data correspond to fiscal year (April-March); e.g., 2025 pertains to April 2025-March 2026.

2. Projections for 2026 and 2027 are taken from the IMF WEO, January 2026 update.

Sources: Official statistical agencies; Bloomberg; World Economic Outlook Update, January 2026, IMF; and RBI staff estimates. | Among other AEs, Japan’s GDP was adversely affected by US tariffs, contracting in Q3:2025 as exports declined and residential investment fell due to stricter energy-efficiency standards. In Q4, GDP grew marginally supported by a rebound in residential investment and government expenditure. Fiscal expansion by the new government is expected to support near-term growth. Expansion in the PMI eased for both services and industrial activity in March. In the euro area, GDP rose in Q3 on the back of stronger investment and government spending despite a drag from net exports. Growth weakened in Q4 as investment and government outlays slowed. In Q1:2026 so far, composite PMI in the euro area signalled expansion in February, with manufacturing rebounding amid rising new factory orders. In the UK, GDP growth remained subdued in both Q3 and Q4 due to weak services activity and a decline in construction. The November UK budget is expected to support revenues and ease concerns over rising public debt. The labour market has softened, with unemployment rising to a nearly five-year high of 5.2 per cent in December and January 2026, despite recent signs of robust business activity as indicated by PMI readings. Among major EMEs, China faced headwinds in 2025 from higher tariffs, a stagnant property market, and weak domestic consumption, yet realised its 5.0 per cent growth target. Real GDP growth moderated in Q3 and Q4 as front-loaded trade effects unravelled, and gross fixed capital formation declined. Government stimulus measures helped support consumption, even as the downturn in the property sector persisted. Notably, China’s external trade registered a record surplus in 2025, driven by diversification into new markets amid higher US tariffs. However, in March 2026, the pace of PMI expansion moderated as activity softened across both manufacturing and services. Brazil’s GDP growth remained stable at 1.8 per cent (y-o-y) in Q4 as growth in services and agriculture was offset by contraction in manufacturing. Household consumption remained weak despite a fall in the unemployment rate in Q4:2025 reflecting tighter financial conditions. The composite PMI contracted in March on falling sales across both manufacturing and services. Russia’s growth weakened in Q3 due to softer net exports amidst dampened domestic demand due to increased sanctions and high interest rates. In South Africa also, GDP growth softened in Q4 due to contractions in manufacturing and mining while the services and agriculture sectors remained resilient. After a weak Q4, however, the composite PMI remained at a neutral level in Q1:2026 (up to February), indicating stable business conditions. Growth in ASEAN1 economies was revised upwards by the Asian Development Bank (ADB) in December, raising its 2025 projection by 20 bps to 4.5 per cent from the September forecast, reflecting strong Q3 performance across key economies. Growth projections for 2026 were also revised up by 10 bps to 4.4 per cent in the wake of an improved external environment and supportive public spending. Turning to high-frequency indicators, the OECD's composite leading indicators (CLIs) showed that most economies remained above their long-term trend during Q4:2025 and Q1:2026 (up to February) (Chart I.1a). The global composite PMI stayed firmly in expansion territory in February, driven by growth in both manufacturing and services sector (Chart I.1b). However, in March manufacturing activity lost momentum as output and new orders slowed. Despite disruptions from the rising tariff-related uncertainty brought about by the Liberation Day US tariff announcements, global merchandise trade volumes expanded for nine consecutive quarters through Q4:2025. The expansion was supported by bilateral trade arrangements and front-loading of exports and imports by both emerging market and advanced economies (Chart I.2a). As per the WTO (March 2026), trade volume grew by 4.6 per cent (year-on-year) in 2025, driven by stronger trade in AI-related products that are largely exempt from tariffs and favourable macroeconomic conditions. However, the WTO projects global trade growth to decelerate sharply to 1.9 per cent in 2026 due to persistent policy uncertainty and weaker global demand. During 2025, freight rates, as reflected in the Freightos Baltic Global Index stayed below 2024 average, suggesting lower pressures on shipping cost (Chart I.2b). I.2 Commodity Prices and Inflation Since Q3:2025, commodity prices, as captured by the Bloomberg Commodity Index, have gradually moved higher with intermittent spikes led by precious metals on strong safe‑haven demand (Chart I.3a). Commodity prices have diverged largely owing to sector-specific fundamentals as precious and industrial metals witnessed a sharp increase (Box I.1). Agricultural prices remained largely unchanged on ample supplies. Global food prices rose marginally in Q1:2026 as compared to Q4:2025, driven by meat, cereals and vegetable oils (Chart I.3b). Energy prices rose in Q1:2026 relative to the previous quarter, largely driven by crude oil in the wake of supply disruptions. Brent crude ended Q4:2025 on a weaker note amid ample supply but rebounded sharply in Q1:2026 on escalating tensions in West Asia in March (Chart I.3c). Gold prices rose through Q4:2025 and the first two months of 2026, supported by safe‑haven demand on persistent trade tensions, central bank buying and a softer US dollar. However, it receded in March on the back of shifting expectations on US monetary policy, dollar appreciation, higher US yields, and profit booking. Copper rose on tighter supply and uncertainty around tariff, which increased the risk premium. Aluminium and zinc rose on supply constraint and a bearish US dollar. Base metals were further supported by an improved demand outlook from China underpinned by new government stimulus measures and the economy’s shift towards green technologies. Broader West Asia tensions added to uncertainty in global commodity markets. The metal price rally, however, faded as the US dollar strengthened in March amid rising US yields and safe-haven flows (Chart I.3d).

Consumer Price Inflation Global disinflation continued, albeit at an uneven pace across advanced and emerging economies. A subdued US dollar helped ease imported inflation pressures, particularly in emerging markets with sizeable foreign‑currency exposures. As per the latest OECD Economic Outlook, heightened uncertainty around the ongoing West Asia conflict has firmed up energy prices, which is expected to increase headline inflation in 2026 and raise medium‑term inflation expectations. Box I.1 Bubble Dynamics in Gold Prices? Gold prices rose sharply since 2024, driven by escalating geopolitical tensions, a weakening US dollar, and growing expectations of monetary policy easing across major economies following the end of the global tightening cycle. Prices underwent a sharp appreciation – increasing by more than twice within a relatively short span from around US$2,060 at end-2023 to US$5,000 per ounce by February 2026 while repeatedly scaling new highs. During this period, gold ranked among the best-performing assets globally (Chart I.1.1). While part of this increase reflects strong safe-haven demand and heightened uncertainty, the pace and persistence of the rise suggest the possibility of the build-up of bubble-like dynamics during 2025. Bubbles typically feature rapid, accelerating price surges- usually referred to as explosive behaviour – followed by sharp corrections (Phillips et al., 2011). Yet, their detection remains tricky: there is no conclusive evidence that post‑surge crashes are predictable, making it difficult to distinguish irrational exuberance from rational responses to changes in fundamentals that may be latent or unobserved (Shiller, 2000). To avoid these identification issues, statistical methods focus on the time‑series properties of prices rather than directly modelling fundamentals. In particular, they exploit hallmark explosiveness of bubbles, where the data‑generating process becomes non‑stationary with an upward drift, producing increasingly rapid price increases (Evans, 1991). This has motivated the use of methodology akin to unit‑root in which the presence of a bubble corresponds to autoregressive roots exceeding unity, signalling explosive dynamics (Phillips et al., 2015). The empirics concentrate on detecting such explosive episodes in observed price series rather than inferring bubbles solely from fundamentals.  To examine this, the Right-tailed Augmented Dickey–Fuller (RADF) methodology, implemented through rolling ADF regressions on monthly data from 1960 onwards, is used to identify episodes of explosive price behaviour. While the approach is useful in detecting periods of exuberance, it is not a conclusive test for identifying asset price bubbles. It suggests explosive behaviour even when rapid price increases are driven by shifts in fundamentals, structural breaks or volatility clustering. It also does not predict the precise timing of a potential reversal. The results show that the test statistics moved above the 95 per cent critical threshold in 2025, indicating a period of statistically significant explosive dynamics in gold prices (Chart I.1.2). A sharp correction in gold prices can trigger margin calls and liquidation of leveraged positions, forcing investors to sell other financial assets and imparting volatility across markets. It can also affect portfolio allocation and market sentiment, leading to broader repricing in equities, bonds, and currencies. Overall, the evidence suggests that gold prices entered a significant phase of price escalation in 2025, consistent with bubble-like behaviour, with the sharp and persistent price surge pointing to pronounced market exuberance and a possible increase in underlying risks. References: 1. Evans, G. W. (1991). Pitfalls in testing for explosive bubbles in asset prices. American Economic Review, 81(4), 922–930. 2. Phillips, P. C. B., Wu, Y., & Yu, J. (2011). Explosive behavior in the 1990s NASDAQ: When did exuberance escalate asset values? International Economic Review, 52(1), 201–226. 3. Phillips, P. C. B., Shi, S., & Yu, J. (2015). Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. International Economic Review, 56(4), 1043–1078. 4. Shiller, R. J. (2000). Irrational exuberance. Princeton University Press. |

Headline CPI inflation has gradually eased but remains above target in some major AEs. Inflation in the US, measured by the personal consumption expenditure (PCE) price index — the Federal Reserve’s preferred inflation metric — has been broadly stable but above target. PCE inflation has witnessed a slight uptick in recent months, reflecting higher energy prices and shelter cost amid persistent services inflation. In the UK, headline inflation has been trending lower since H2:2025, mainly due to easing services inflation amid slower wage growth, although it remains above target. In the euro area, headline inflation, which had remained close to the 2.0 per cent target in Q4:2025, dipped to 1.7 per cent in January 2026, but rose thereafter to 2.5 per cent in March, largely on account of higher energy inflation. Japan’s inflation has generally eased since the last MPR with easing food and lower electricity prices (Chart I.4a). In key emerging markets, CPI inflation has generally declined since the last MPR. In Brazil, headline CPI has been gradually converging towards target on the back of monetary tightening undertaken earlier. In South Africa, headline inflation has remained within the target band with the recent decline driven by transportation costs. In Russia, CPI inflation has been on a disinflationary path. China’s headline CPI inflation remained positive, with February posting the sharpest rise since January 2023 due to Chinese New Year related spending (Chart I.4b). Since the last MPR, inflation has edged lower in some advanced economies supported by easing of services’ inflation, while inflation in key emerging markets remain contained. However, renewed pressure on energy prices has emerged as a fresh upside risk to the inflation outlook. Overall, while inflation remains contained in many economies, the recent rise in energy prices has increased upside risks, calling for cautious adjustments of monetary policy paths. I.3 Monetary Policy Stance Since October 2025, the global easing cycle has slowed. Major central banks in AEs have largely paused, while the Bank of Japan (BoJ) and Australia have embarked on a gradual tightening cycle. A few EM central banks continued easing as inflation fell, resulting in the plateauing of policy rates. Among major AEs, the Fed reduced the policy rate by 25 basis points each in its October and December meetings as a calibrated response to the downside risks to employment. It then kept rates unchanged in Q1:2026 as inflation stayed somewhat elevated, choosing to wait and assess how earlier moves and the oil shock affect the economy before adjusting policy. In this regard, the opinions of the FOMC members have increasingly diverged in recent meetings. This reflects greater uncertainty over inflation, labour-market strength, and the timing of policy easing, with policymakers divided between guarding against persistent inflation and avoiding the costs of overtightening (Chart I.5). Since September 2025, the Bank of England has shifted from active easing to a cautious pause, cutting the Bank Rate in December but pausing thereafter as inflation trends toward target. The European Central Bank has largely completed its policy easing cycle, while maintaining a flexible and data dependent approach, with decision calibrated on a meeting-by-meeting basis. Since the last MPR, the BoJ moved from holding rates at 0.5 per cent to hiking by 25 basis points to 0.75 per cent, its highest level in three decades, as confidence grew that inflation and wages were firmer on a durable basis. The BoJ kept rates unchanged in Q1:2026, choosing to wait for clearer evidence on wage growth and underlying inflation while gauging the impact of weaker activity and the oil‑price shock from West Asia tensions before considering further tightening. Among other AEs, the Reserve Bank of Australia embarked on policy tightening with rate hikes both in February and March to counter elevated inflation amid a tighter labour market. In contrast, the Bank of Canada cut the rate by 25 bps in October 2025 to support the economy and the soft labour market. It, however, kept the policy rates unchanged in its last three meetings amidst tariff related uncertainty and elevated geopolitical tensions. Likewise, New Zealand has moved from cutting rates in Q4:2025 amid slowing growth to holding policy rate steady in 2026 so far, adopting a wait‑and‑watch stance (Chart I.6a).  Among key EMEs, Brazil’s central bank unanimously lowered the Selic rate by a quarter point in March, its first cut in almost two years as economic activity remained subdued. The Bank of Russia has gradually lowered its key rate as economic growth has moved to a more balanced pace while inflation has moved closer to target. China has held its benchmark rate at 3.0 per cent for almost a year. South Africa has moved from a target range to a point target of 3.0 per cent (±1 percentage point). With improving inflation prospects, the MPC cut the policy rate by 25 bps to 6.75 per cent in November but paused in 2026 so far due to upside risks to inflation. Thailand cut its policy rate twice to support a fragile recovery and ease debt burden. Mexico also delivered a cumulative 75 basis points rate reduction as weaker growth, and projections of inflation gradually converging toward target allowed policy normalisation (Chart I.6b). I.4 Financial Markets Notwithstanding trade tensions and geopolitical flashpoints, global risk sentiment remained buoyant in late 2025 and early 2026 as inflation eased, monetary policy stayed accommodative and AI‑related optimism persisted. In contrast, March 2026 witnessed a broad correction in equities with a shift from risk‑on sentiment as the outbreak of conflict in West Asia and renewed inflation worries prompted investors to reduce exposure to risky assets. Sovereign bond yields remained elevated amid fiscal concerns, with the recent West Asia conflict adding further upward pressure. Currency markets also reflected this shift in sentiment with the US dollar strengthening on safe-haven demand recently. Most advanced and emerging market currencies came under depreciation pressure. Global equity markets gained in Q4:2025 with gains being observed in both advanced and emerging economies (Chart I.7a). Equity markets were supported by solid earnings growth, easing inflationary pressures and expectations that systemically important central banks would continue to lower interest rates in 2026. Over the Q4 of 2025, US equities registered gains, despite the longest government shutdown. The quarterly gains helped the market to deliver a double-digit return for the third straight year. The S&P 500 Index posted a nearly 16.0 per cent return for 2025 on AI related optimism, accomodative monetary policy and some progress on trade deals, though investors remained concerned over high valuations of tech stocks. Euro area also delivered positive gains in Q4 on easing inflation and improved outlook as GDP forecast for 2025 was revised upward. Japanese equities also gained in Q4 on expectations of strong growth in generative AI and higher defence spending. The formation of the new Government in Japan was perceived as that providing greater political stability and supportive of more fiscal stimulus.  In Q1:2026, equities declined as risk sentiment deteriorated amid escalating West Asia tensions that weighed on major indices. A rising US dollar has further reinforced the risk-off tone, even as overall conditions remain supported by accommodative monetary and fiscal policies in several jurisdictions. Emerging markets have outperformed developed markets, helped by dollar weakness and country‑specific factors, despite political tensions and shifting rate expectations. More recently, both advanced and emerging markets came under selling pressure following the latest FOMC decision and minutes as investors interpreted Fed policy to be hawkish, reassessed stretched technology stock valuations, and reacted to the ongoing West Asia conflict. Japanese shares initially rose on optimism about generative‑AI demand even as domestic interest rates firmed up across the curve, reflecting higher growth and inflation along with mounting concerns over fiscal discipline. Equities, however, have since slumped as rising oil prices have clouded the economic outlook. Emerging market equity benchmarks have generally remained supported by a soft US dollar, capital inflows in specific jurisdictions, and improved sentiment around artificial intelligence (with EM Asia – particularly Korea and Taiwan – benefiting from their role in the chip and memory supply chain). China’s domestically developed AI model has kept market attention on the region’s AI potential, even as renewed trade‑policy uncertainty and rising geopolitical tensions in March sparked risk‑off sentiment, leading to decline in equities in Q1:2026. Emerging markets still trade at lower forward P/E ratios than the S&P 500, supported by benign inflation and generally accommodative monetary and fiscal policies in many economies. However, global uncertainty persists driven by tensions in West Asia, uncertain tariff landscape, and risks to future path of inflation. As crude oil prices rise, there is a growing risk that the disinflation process could pause or reverse, complicating the outlook for both inflation and monetary policy (Chart I.7b). Sovereign debt levels remain high across major advanced economies, exerting upward pressure on bond yields and intensifying the imperative for central banks to rein in inflation. In most cases, this objective has either been largely achieved or is nearing completion, although the latest energy‑price shock is again posing upside risks to inflation. In the US, yields briefly softened in October 2025 on safe‑haven demand during the shutdown. However, they soon hardened, driven by hawkish Fed communication, sticky inflation prints, and monetary policy normalisation in Japan. Sovereign bond yields across major AEs largely traded in a narrow range in Q4:2025, reflecting persistent fiscal pressures and cautious monetary policy stances. In Q1:2026, bond yields generally traded with a downward bias till February amid rotation risks following the tech sell‑off, escalating geopolitical tensions, and soft Q4:2025 GDP data of the US. Markets took comfort from clearer policy signals in Japan, easing inflation across several major economies, and episodic safe‑haven demand driven by geopolitical tensions and concerns over stretched technology valuations. In March, however, yields reversed course partially and edged higher amid renewed inflation worries following the outbreak of the conflict in West Asia, prompting investors to reassess the path of global interest rates and term premia. Japanese government bond yields rose on the back of BoJ policy normalisation, persistent inflation, and expectations of expansionary fiscal policy under the new government. In March, bond yields firmed on higher crude prices (Chart I.8a). Emerging‑market bond yields were mixed through Q4:2025 and most of Q1:2026, while lower domestic inflation and expectations of easier policy in some advanced economies supported carry in several markets, yields elsewhere rose as investors reassessed inflation risks, the likely pace of rate cuts, and the impact of the West Asia conflict on fiscal and risk premia. In March, yields picked up notably in many economies amid renewed fears of energy‑driven inflation (Chart I.8b).  Currency markets remained turbulent in 2025, especially the US dollar, which stayed subdued and highly sensitive to risk sentiment and policy expectations, though investor enthusiasm in AI and the resulting capital flows into US equities provided some support to the dollar. The US dollar fell over 9.0 per cent in 2025 against major currencies, as looming Fed rate cuts narrowed yield differentials even as worries over US fiscal deficit and political uncertainty intensified. The US dollar remained broadly unchanged in Q4:2025, with intermittent rallies driven by a hawkish Fed tone, the release of strong Q3 GDP data and safe‑haven flows. Thereafter, it has traded with a depreciating bias, reflecting weak data and deteriorating sentiment, though receiving support from safe‑haven demand during the West Asia conflict. Overall, after remaining subdued for most of Q1:2026, the dollar firmed toward the end of the quarter on renewed safe‑haven demand and still‑elevated inflation. Higher forex volatility in G7 currencies often coincided with a weaker US dollar, but this negative correlation has waned in March as safe‑haven flows and a hawkish repricing of Fed expectations have produced several recent positive readings, with volatility spikes often accompanying a stronger dollar (Chart I.9). The MSCI emerging market currency index posted gains in Q4:2025 but declined in Q1:2026, as the West Asia conflict in March triggered renewed currency pressures and portfolio outflows amid a strengthening US dollar. While AI‑related optimism and expansionary fiscal policies – provide a supportive backdrop, capital flows remain volatile amid headwinds from tariff uncertainty, geopolitical tensions, and shifting Fed policy expectations (Chart I.10 a & b).

I.5 Conclusion The global economy faces significant headwinds from escalating geopolitical tensions, persistent trade frictions, rising public debt, and volatility around AI‑driven equity valuations. Global growth has been resilient but remains below its historical average, while disinflation is uneven and could be reversed by the recent rise in energy prices. Overall, the outlook for 2026 points to a moderate expansion and it remains highly sensitive to shifts in the geopolitical landscape and energy‑driven inflation risks. The balancing of conflicting objectives would require cautious calibration of monetary policy paths while minimising the cost of adjustment. _________________________________________________________________________________

II. Liquidity Conditions and Financial Markets System liquidity remained in surplus during H2 supported by the Reserve Bank’s liquidity augmenting measures. Domestic financial markets exhibited bouts of volatility amidst global uncertainty. Overnight rates in the money market evolved in sync with policy rate and prevailing liquidity conditions. Transmission to lending and deposit rates continued and bank credit growth improved in H2. Sectoral trends indicate strengthening of credit growth across segments. Introduction During H2:2025-26, global financial markets generally remained resilient, before turning volatile amidst heightened geopolitical tensions due to conflict in West Asia. Domestic financial markets displayed intermittent volatility amidst global uncertainties and volatile capital flows. The Monetary Policy Committee (MPC) reduced the policy rate by 25 basis points (bps) during H2, taking the cumulative reduction to 125 bps since February 2025. Moderation in system liquidity surplus in early H2 was reversed through calibrated injections of durable liquidity. Overnight money market rates largely moved in line with the evolving liquidity conditions. Monetary policy transmission was aided by a healthy passthrough to lending and deposit rates during H2. Bank credit growth continued to improve and remained supportive of real economic activity. The financing from non-bank sources also increased. II.1 Liquidity Conditions and the Operating Procedure of Monetary Policy The Reserve Bank of India (RBI) Act, 1934 requires the Reserve Bank to place the operating procedure relating to the implementation of monetary policy and changes thereto from time to time, if any, in the public domain.1 During H2:2025-26, the MPC reduced the policy repo rate by 25 bps in the December meeting. Moreover, the MPC decided to maintain the neutral stance adopted in June 2025. The Reserve Bank also reduced the cash reserve ratio (CRR) by 100 bps to 3.0 per cent of net demand and time liabilities (NDTL) in a staggered manner during September-November 2025.2 The CRR cuts supported system liquidity during H2. Effective December 15, 2025, the definition of reporting fortnight for banks was changed along with a change in the CRR maintenance cycle. As per the new definition, a reporting cycle is defined as the period from the first day to the fifteenth day of each calendar month and the sixteenth day to the last day of each calendar month, both days inclusive. The changes in reporting cycle imply that the number of days in the first reporting cycle of the month (15 days) may be different from the second reporting cycle (which can vary from 13-16 days) with attendant implications for demand for reserves within the reserve maintenance period. Moreover, the number of reporting cycles in a year is now standardised to 24 as against 26-27 reporting fortnights in the earlier system. Drivers and Management of Liquidity System liquidity, as measured by the net balances under the liquidity adjustment facility (LAF), moderated in H2:2025–26 from a large surplus in H1 (Chart II.1). On a net basis, average daily absorption under the LAF declined to ₹1.43 lakh crore in H2, as compared with ₹2.29 lakh crore in H1. The expansion in currency in circulation (CiC) and volatile capital flows were principal drivers of liquidity conditions in H2. System liquidity remained in surplus during H2:2025- 26, except for a few intermittent occasions when tax payments withdrew liquidity from the banking system.3 System liquidity moderated in Q3, reflecting the increase in CiC during the festive season and the Reserve Bank's foreign exchange operations. It was partly offset by the reduction in the CRR and the Reserve Bank's purchase of securities through open market operations (OMOs). Liquidity conditions improved in Q4, as a sharp rise in CiC was more than offset by liquidity injection through OMO purchases, long-term USD/INR Buy/Sell swap auctions, and term repo auctions (Table II.1).

| Table II.1: Liquidity – Key Drivers and Management | | (₹ crore) | | | 2024-25 | 2025-26 | | H1 | H2 | H1 | Q3 | Q4* | H2* | | Drivers | | | | | | | | (i) CiC [withdrawal (-) /return (+)] | 29,247 | -2,42,234 | -74,052 | -1,25,023 | -2,08,489 | -3,33,512 | | (ii) Net Forex Purchases (+)/ Sales (-) | 70,402 | -3,61,635 | -1,41,591 | -3,28,665 | 14,632 | -3,14,033 | | (iii) GoI Cash Balances [build-up (-) / drawdown (+)] | -2,04,802 | 2,98,531 | -3,44,103 | 74,298 | 26,974 | 1,01,272 | | (iv) Excess Reserves [build-up (-) / drawdown (+)] | -15,839 | 16,655 | 14,376 | 17,884 | -6,663 | 11,221 | | Management | | | | | | | | (i) Net OMO Purchases (+)/ Sales (-) | -24,040 | 2,83,386 | 2,39,223 | 1,81,435 | 4,06,900 | 5,88,335 | | (ii) Required Reserves [including both change in NDTL and CRR] | -55,613 | 76,450 | 15,674 | 1,67,530 | -17,776 | 1,49,754 | | (iii) Term Repo Auctions | - | 1,82,964 | 25,731 | - | 1,36,504 | 1,62,235 | | Memo Item | | | | | | | | (i) Long term Forex Swaps Buy/Sell (+)/ Sell/Buy (-)^ | - | 2,19,245 | - | 46,147 | 1,80,738 | 2,26,885 | | (ii) Net Absorption (+)/ Injection (-) as at end-period | 84,651 | 1,30,261 | 56,274 | 28,123 | 2,15,148 | 2,15,148 | Notes: 1. (+) / (-) sign suggests accretion to / depletion of banking system liquidity.

2. Data pertain to the last reporting day of the respective period.

3. *: Data for Q4 and H2:2025-26 are up to Mar 15, 2026.

4. ^: approximate values.

Source: RBI. | With liquidity conditions remaining in surplus, banks’ recourse to the marginal standing facility (MSF) averaged at ₹0.02 lakh crore during H2:2025-26, same as in H1, while daily balances under the standing deposit facility (SDF) increased from an average of ₹1.84 lakh crore in H1 to ₹2.20 lakh crore in H2. The Reserve Bank remained nimble and agile in its liquidity management operations to ensure sufficient liquidity in the banking system and facilitate transmission in money market (Box II.1). On a review of liquidity conditions and the outlook, the Reserve Bank undertook several measures including OMO purchases, buy/sell forex swaps and long term repos during H2 to inject durable liquidity into the banking system (Table II.2). | Table II.2: Reserve Bank’s Liquidity Measures during 2025-26 | | (₹ crore) | | Measures | H1:2025-26 | H2:2025-26 | FY:2025-26 | | CRR Cut | 62,500* | 1,87,500* | 2,50,000* | | OMO Purchase Auctions | 2,39,203 | 5,00,000 | 7,39,203 | | USD/INR Buy/Sell Swap Auctions | | 2,26,885* | 2,26,885* | | Term Repo Auctions | 25,731 | 1,36,504 | 1,62,235 | | Total | 3,27,434 | 10,50,889 | 13,78,323 | Note: * indicates approximate value.

Source: RBI. |

Box II.1: Optimal Level of Liquidity Central banks actively manage liquidity conditions in the banking system to ensure that the operating target remains aligned to the policy rate, hovering within the interest rate corridor. The guiding principle of liquidity management of the Reserve Bank, as reiterated in the revised liquidity management framework of September 2025, is to align the weighted average call rate (WACR) with the policy repo rate. Liquidity mismatches could lead to deviation of the operating target from the policy rate, hampering monetary policy transmission (Kavediya and Pattanaik, 2016). Excessive liquidity surplus over a prolonged period runs the risk of driving short term interest rates to ultra-low levels, distorting risk perceptions and engendering asset price bubbles. Moreover, persistently large surplus liquidity tends to lull market participants to a state of complacency in which they get accustomed to large liquidity. In contrast, large deficit (shortage) in the banking system liquidity raises borrowing costs for banks, which constricts lending capacity, impede monetary transmission and potentially undermine financial stability. Therefore, it becomes essential to assess the optimal level of system liquidity in consonance with the monetary policy stance. Against this backdrop, an attempt is made to estimate the adequate level of liquidity in the banking system which is consistent with the guiding principle of RBI’s liquidity management, ie., aligning the spread (weighted average call rate over policy repo rate) with the prevailing liquidity conditions (Liq) – net LAF. Considering the well-known asymmetry in transmission across surplus and deficit regimes (RBI, 2021), two separate estimations, each for the phase of surplus and deficit liquidity have been undertaken based on daily data for the period January 2012 to March 2026. Since the extent of the impact of liquidity may vary within a particular phase depending on the initial conditions, this heterogeneous impact is estimated by fitting a non-linear function. Accordingly, fractional polynomial model is fitted using the standard eight-element powers set separately for surplus and deficit liquidity conditions.4 The best-fit model for each regime is selected using Royston-Sauerbrei closed testing procedure (Royston and Sauerbrei, 2008) based on likelihood ratio tests. The fitted curves are specified below. Spread = 0.58-0.5*log (Liq+3.3); for Liq < 0 (Deficit phase) Spread = -0.03-0.07 Liq2 + 0.01 Liq3; for Liq > 0 (Surplus phase) Accordingly, the best-fit curves for the surplus and deficit liquidity period are plotted in Chart II.1.1. The relationship shows that the increase in liquidity is inversely related to the spread; moreover, the relationship is found to be non-linear. The impact of excess liquidity on the spread diminishes significantly beyond a point. The curve flattens as excess liquidity rises, suggesting that large excess liquidity does not have substantial incremental impact on the spread beyond a threshold. However, under deficit conditions, the spread becomes unbounded at higher levels of deficit. The findings suggest that surplus liquidity in the range of 0.6 to 1.1 per cent of NDTL is likely to keep the spread between 5 to 10 bps below the repo rate, while liquidity deficit in the range of 0.4 to 0.7 per cent of NDTL is likely to keep the WACR above the repo rate between 5 to 10 bps. As evident from the findings, keeping the WACR aligned to the repo rate entails different levels of liquidity in deficit and surplus conditions. Moreover, the extent of alignment is also contingent on the level of the surplus/ deficit. References: 1. Kavediya, R. and Pattanaik, S. (2016), “Operating Target Volatility: Its Implications for Monetary Policy Transmission”, Reserve Bank of India Occasional Papers Vol. 37, No. 1&2, 2016. 2. Reserve Bank of India, (2021), “Report on Currency and Finance”. 3. Royston, P. and Sauerbrei, W. (2008). Multivariable Model-Building: A Practical Approach to Regression Analysis Based on Fractional Polynomials for Modelling Continuous Variables. John Wiley & Sons, Hoboken. | The Reserve Bank conducted several variable rate repo (VRR) and variable rate reverse repo (VRRR) operations of varying maturities to modulate transient liquidity and align the rates in the overnight segment to the policy rate. Overall, 44 VRR and 7 VRRR auctions were conducted in H2:2025:26. As on March 15, 2026, reserve money (M0) expanded by 5.8 per cent (y-o-y) as against 3.7 per cent a year ago, reflecting expansion in CiC. Adjusted for the CRR change, growth in reserve money stood at 10.7 per cent (6.2 per cent a year ago). As on March 15, 2026, growth (y-o-y) in money supply (M3) rose to 10.7 per cent from 9.4 per cent a year ago with faster growth in aggregate deposits and currency with the public. Aided by CRR cuts, the money multiplier increased to 5.99 as on March 15, 2026, from 5.72 a year ago, notwithstanding an increase in the currency-deposit ratio. II.2 Domestic Financial Markets Money market rates evolved in sync with system liquidity and monetary policy actions. A combination of domestic and global factors drove long-term government bond yields higher. Equity markets and the Indian rupee displayed two-way movements amidst volatile capital flows and evolving global risk perceptions. The West Asia conflict led to accentuated downward pressure for both equity markets and the Indian rupee in March. In the credit market, bank credit grew at a healthy pace. II.2.1 Money Market During H2:2025-26, money market rates moved in tandem with the policy repo rate and evolving liquidity conditions. The weighted average call rate (WACR) – the operating target of monetary policy – largely remained below the policy repo rate until the first half of December 2025. Thereafter, during second half of December and January, the WACR traded above the policy repo rate amidst moderation in liquidity surplus (Chart II.2a). The WACR softened subsequently on the back of several liquidity augmenting measures by the Reserve Bank. The WACR hovered largely within the policy rate corridor during H2: 2025-26, with its spread over the policy repo rate widening from (-)2 bps in October 2025 to (+)4 bps in March 2026. Volatility in the WACR, as measured by the exponential weighted moving average (EWMA)5, rose in December 2025 before moderating in February and March 2026 (Chart II.2b). Overnight rates in the collateralised segment, i.e., tri-party repo and market repo, broadly moved in line with the WACR during H2 (Chart II.3).

Money market activity remained dominated by the collateralised segments (tri-party and market repo), with their share in overnight money market volume standing at 97 per cent. The share of the uncollateralised segment, i.e., the call money market, remained largely flat at around 3 per cent (Table II.3). Mutual funds (MFs) remained the major lenders in tri-party repo, despite their share tapering by 3 percentage points to 65 per cent in H2:2025-26 from H1. In the market repo segment, however, the share of lending by mutual funds increased to 48 per cent in H2 from 40 per cent in H1. The share of foreign banks’ lending in market repo remained steady at 29 per cent in H2. On the borrowing side, public sector banks (PSBs) remained the major players in the tri-party repo, with their share increasing to 32 per cent in H2 from 28 per cent in H1, while that of private sector banks declined to 24 per cent from 28 per cent. PSBs' share in market repo borrowings increased by 2 percentage points to 8 per cent over the same period. | Table II.3: Average Volume and Share in Overnight Money Market | | (₹ lakh crore) | | | 2024-25 | 2025-26 | | H1 | H2 | H1 | Q3 | Q4 | H2 | | Call/Notice | 0.10 | 0.11 | 0.16 | 0.16 | 0.15 | 0.16 | | | (2.12) | (2.18) | (2.78) | (2.72) | (2.40) | (2.56) | | Tri-party Repo | 3.30 | 3.62 | 3.69 | 3.91 | 4.35 | 4.12 | | | (68) | (70) | (66) | (66) | (70) | (68) | | Market Repo | 1.48 | 1.42 | 1.73 | 1.87 | 1.69 | 1.78 | | | (30) | (28) | (31) | (31) | (27) | (29) | | Total | 4.88 | 5.16 | 5.57 | 5.94 | 6.19 | 6.06 | | | (100) | (100) | (100) | (100) | (100) | (100) | Notes: 1. Figures in parentheses denote share of each segment in overnight money market volume. Figures may not add up to total due to rounding off.

2. Data include working saturdays.

Sources: Clearing Corporation of India Limited F-TRAC; and RBI. |

| Table II.4: Tenor wise Break up of CD Issuances | | (₹ lakh crore) | | | 2024-25 | 2025-26 | | H1 | H2 | H1 | Q3 | Q4 | H2 | | Up to 91 Days | 3.93 | 3.74 | 3.55 | 2.07 | 2.33 | 4.40 | | | (73) | (57) | (73) | (62) | (44) | (51) | | 92-180 Days | 0.20 | 0.17 | 0.47 | 0.38 | 0.23 | 0.61 | | | (4) | (3) | (10) | (11) | (4) | (7) | | 181-365 Days | 1.22 | 2.64 | 0.84 | 0.88 | 2.71 | 3.58 | | | (23) | (40) | (17) | (27) | (51) | (42) | | Total | 5.35 | 6.56 | 4.86 | 3.32 | 5.27 | 8.59 | | | (100) | (100) | (100) | (100) | (100) | (100) | Note: Figures in parentheses denote share of each maturity profile. Figure may not add up to total due to rounding off.

Sources: Clearing Corporation of India Limited F-TRAC; and RBI staff estimates. | The term segments of the money market witnessed slower transmission compared to the overnight market, mainly due to intermittent liquidity tightness and increased uncertainty. The rates on certificates of deposit (CDs) edged up especially in Q4 as banks increased issuances to bridge the widening funding gaps amidst the rollover of maturing papers and higher credit offtake. The average spread of CDs and CPs over the policy repo rate widened substantially to 116 bps and 136 bps, respectively, in H2:2025-26 from 36 bps and 60 bps, respectively, in H1. Similarly, the average spread of treasury bills (T-Bills) over the policy repo rate moved from negative to positive territory (Chart II.3). Fresh issuances of CDs increased considerably to ₹8.6 lakh crore in H2:2025-26 from ₹4.9 lakh crore in H1, reflecting widening gap between growth in deposits and credit. Tenor-wise, share of CD issuances at the shorter tenor (up to 91-day) reduced while longer tenor issuances increased in Q4 compared to Q3 as banks sought to lock in funds for longer period to meet higher credit demand (Table II.4). The issuances of CPs in the primary market declined to ₹7.9 lakh crore during H2:2025-26 from ₹8.9 lakh crore in H1, as higher rates led to a shift towards borrowings from banks (Chart II.4a). The risk premia on CPs (spread of 3-month CP rate over 91-day T-bill rate) showed an increasing trend tracking inter alia rising uncertainty in H2 (Chart II.4b).

Non-banking financial companies (NBFCs) dominated CP issuances, with an average share of 38 per cent in H2:2025-26. The share of corporates dropped to 32 per cent in H2 from 49 per cent in H1 (Chart II.5). In terms of maturity profile, the 91-180 days segment had the largest share (53 per cent) in fresh CP issuances, followed by the 31-90 days segment (Table II.5). | Table II.5: Maturity Profile of CP Issuances | | (₹ lakh crore) | | Tenor | H1: 2024-25 | H2: 2024-25 | H1: 2025-26 | H2: 2025-26 | | 7-30 days | 0.63 | 0.51 | 0.43 | 0.66 | | | (8) | (6) | (5) | (8) | | 31-90 days | 2.35 | 2.33 | 3.10 | 1.87 | | | (31) | (28) | (35) | (24) | | 91-180 days | 3.94 | 4.24 | 4.56 | 4.24 | | | (52) | (52) | (51) | (53) | | 181-365 days | 0.64 | 1.11 | 0.86 | 1.16 | | | (8) | (14) | (10) | (15) | | Total | 7.55 | 8.19 | 8.95 | 7.93 | | | (100) | (100) | (100) | (100) | | Outstanding (as at end-period) | 3.98 | 4.43 | 4.88 | 4.60 | Notes: 1. Figures in parentheses denote share of each maturity profile.

2. Figure may not add up to total due to rounding off.

Sources: Clearing Corporation of India Limited F-TRAC; and RBI. | II.2.2 Government Securities (G-sec) Market In the government securities (G-sec) market, yields generally remained under pressure during H2:2025-26 reflecting domestic as well as global factors (Chart II.6). At the beginning of H2, yields softened reflecting the MPC’s downward revision of CPI inflation forecasts for 2025–26 and Q1:2026–27 and a decline in crude oil prices. Thereafter, yields hardened in November and December, tracking rising crude oil prices, hardening US yields and increased FPI outflows.  In January, yields continued to harden before sofenting towards the month-end in response to OMO purchases undertaken by RBI. In February, yields hardened briefly due to higher-than-expected gross market borrowings announced in the Union Budget 2026-27. Subsequently, yields moved with a softening bias as RBI conducted more OMO purchases (Chart II.6). In March, yields hardened again amidst heightened geo-political tensions in West Asia triggering a rise in crude oil prices, and government's decision to cut special excise duty on diesel and petrol. At the shorter end upto one year, yields generally softened during H2:2025-26 buoyed by a policy rate cut in December 2025 and the Reserve Bank's measures for augmenting durable liquidity (Chart II.7). The average trading volume in G-secs and T-bills in H2:2025-26 was lower than H1 (Chart II.8). The weighted average yield (WAY) on traded maturities increased by 21 bps for G-secs, while it declined by 22 bps for T-bills in H2 as compared to H1. The overall dynamics of the yield curve are captured by its latent factors, viz., level, slope and curvature6. Yields have generally hardened across the term structure (Chart II.9a). This was partly attributed to (i) increased market borrowings, (ii) higher issuance of longer-tenor state government securities (SGSs), and (iii) moderation in demand for long-tenor government securities by institutional investors. The average level of yields increased by 51 bps, while the slope of the yield curve steepened by 54 bps, reflecting the hardening bias at the longer end (Chart II.9b). The curvature, on the other hand, also increased by 60 bps. In the Indian context, the level and curvature of the yield curve are found to have more information content on future macroeconomic outcomes than the slope owing to market segmentation and preferred habitat of investors, unlike in AEs (Patra et al, 2022).7 As part of active debt consolidation, the Reserve Bank conducted seven switch auctions of G-secs amounting to ₹1,45,377 crore during H2:2025-26, on behalf of the Government of India. Based on an assement of the evolving demand conditions, the supply of long papers was reduced in H2. As a result, weighted average maturity (WAM) of G-sec issuance in H2 reduced to 17.96 years from 19.65 years in H1. The WAM of the outstanding stock, however, increased from 13.60 years at end-September 2025 to 13.70 years as at end-March 2026, while the weighted average coupon (WAC) declined from 7.20 per cent to 7.17 per cent over the same period. The weighted average spread of cut-off yields on SGS over G-sec yields of comparable maturities was 57 bps in H2:2025-26 (Chart II.10) as against 38 bps in H1. The average inter-state spread of cut-off yields on SGS of 10-year tenor (fresh issuances) was 12 bps in H2 as against 5 bps in H1.

II.2.3 Corporate Bond Market Corporate bond yields increased following G-sec yields as well as due to rising risk premia during H2:2025-26 (Chart II.11a). The risk premia widened for higher and lower rated bonds. The average bond market risk premium (the spread of 3-year AAA corporate bond yields over 3-year G-sec yields) increased from 80 bps to 109 bps for Public Sector Units (PSUs), Financial Institutions (FIs) and banks; from 107 bps to 129 bps for NBFCs and from 105 bps to 112 bps for corporates in H2 (March 2026 over September 2025), amidst mixed corporate earnings in Q3 (Chart II.11b and Table II.6).

| Table II.6: Corporate Bonds - Rates and Spreads | | | Interest Rates

(Per cent) | Spreads (bps)

(Over corresponding risk-free rate) | | Instrument | March 2025 | September 2025 | March 2026 | March 2025 | September 2025 | March 2026 | | 1 | 2 | 3 | 4 | 5 | 6 | 7 | | Corporate Bonds | | | | | | | | (i) AAA (1-yr) | 7.76 | 6.69 | 7.40 | 115 | 100 | 171 | | (ii) AAA (3-yr) | 7.62 | 7.10 | 7.36 | 98 | 105 | 112 | | (iii) AAA (5-yr) | 7.60 | 7.20 | 7.52 | 89 | 86 | 92 | | (iv) AA (3-yr) | 8.43 | 8.20 | 8.22 | 178 | 215 | 198 | | (v) BBB-minus (3-yr) | 12.09 | 11.88 | 11.92 | 544 | 583 | 567 | Note: Yields and spreads are computed as monthly averages.

Sources: Fixed Income Money Market and Derivatives Association of India (FIMMDA); and RBI staff estimates. | Primary issuances of listed corporate bonds in domestic markets declined markedly to ₹3.3 lakh crore during H2:2025-26 (up to February 2026) from ₹4.2 lakh crore during the corresponding period of the previous year due to rising cost (Chart II.12a). Overseas issuances increased to ₹24,568 crore during H2 (up to February) from ₹22,953 crore during the same period last year. Most of the resource mobilisation in the corporate bond market (98.7 per cent) was through the private placement route. Outstanding investments by foreign portfolio investors (FPIs) in corporate bonds stood at ₹1.3 lakh crore as on March 30, 2026, with moderation in utilisation of investment limits to 15.0 per cent (Chart II.12b). Trading volume in secondary market surged to ₹8.2 lakh crore during H2 (up to February 2026) from ₹7.9 lakh crore during the corresponding period of the previous year (Chart II.12c). II.2.4 Equity Market During H2:2025-26, Indian equity markets witnessed bi-directional movements. Markets gained in October-November amidst strong corporate earnings results for Q2 and policy rate cut by the US Federal Reserve. It remained range-bound in December as caution surrounding India-US trade negotiations outweighed positive global cues from policy rate cut by the US Federal Reserve and renewed optimism on AI related developments. After declining in January on fresh tariff warnings by the US and mixed corporate earnings for Q3, markets rebounded with the announcement of landmark trade deals between India and its major trading partners – the European Union and the US. Conflict in West Asia, however, led to a sharp decline in markets since end-February, which completely erased the earlier gains. Overall, broader market indices underperformed the benchmark during H2:2025-26 leading to market normalisation (Chart II.13a). Reflecting this overall performance, the price-to-earnings (PE) ratios for the broader market indices fell sharper than the benchmark in H2. The PE ratio for the benchmark BSE Sensex declined to 19.8 at end-March 2026 from 22.2 at end-September 2025. In contrast, the PE ratio for the BSE 250 SmallCap index fell sharply to 26.3 at end-March 2026 from 34.0 at end-September 2025. The PE ratio for the BSE 150 MidCap index declined to 31.1 from 34.2 during this period. The India Volatility Index, a measure of short-term expected volatility of Nifty 50, increased to 27.9 at end-March 2026 from 11.1 at end-September 2025 amidst global tariff uncertainty and persisting geo-political tensions. While all other sectors declined, metal stocks witnessed a rally led by a rise in the global prices of precious metals (Chart II.13b).  FPIs remained net sellers in the domestic equity market in H2:2025-26. Domestic institutional investors (DIIs), especially mutual funds, acted as a counterbalancing force with net buying and provided resilience to markets (Chart II.14). Resource mobilisation in primary equity markets rose to ₹2.3 lakh crore during H2 (up to February 2026), from ₹2.0 lakh crore in H1 (Chart II.15a). Average flows through systematic investment plans (SIPs) have witnessed a sustained increase in recent years supported by policy initiatives such as the ‘Chhoti SIP’ (Chart II.15b). II.2.5 Foreign Exchange Market The foreign exchange market remained volatile during H2:2025-26, driven by shifting US policies, tariff-related uncertainty, and sharp escalation in geopolitical tensions. The US dollar index witnessed a sustained decline till January, slipping to a multi-year low, weighed down by growing US growth and fiscal sustainability concerns, and uncertainty about the duration of the US Federal Reserve’s rate-cutting cycle. With the onset of West Asia conflict at end-February, the US dollar rose sharply, reflecting the rise in safe haven demand. Emerging market (EM) currencies broadly strengthened on weakening US dollar and improved global risk appetite until January 2026, but fell thereafter amidst rising global risk-off sentiments. The Indian rupee (INR) exhibited two-way movements with a depreciating bias on the back of persistent FPI outflows, elevated corporate dollar demand and rise in global risk-off sentiments in H2. The INR appreciated from early February 2026 on the announcement of interim India-US trade deal agreement, but depreciated in March as the conflict in West Asia intensified (Chart II.16a). While implied option volatility, on average, moderated in H2 vis-à-vis H1, it remained high in the face of ongoing risk-off sentiments and rising geopolitical tensions in West Asia (Chart II.16b). In order to ensure orderly conditions in the foreign exchange market, the Reserve Bank introduced a prudential measure on March 27, 2026 that limited the net open position in INR (NOP-INR) of authorised dealers in the onshore deliverable market to within US$ 100 million at the end of each business day. This was aimed at curbing excessive speculative positioning and mitigating systemic risks.

Overall, the INR depreciated by 6.2 per cent against the US dollar in H2 (Chart II.17). However, despite heightened volatility in global market, the INR remained among the least volatile EM currencies during this period, supported by modest current account deficit and robust foreign exchange reserves. Forward premia exhibited sharp movements during H2:2025-26, reflecting shifting interest rate differentials and evolving global sentiments (Chart II.18). The spike in short-term premia in December was driven by capital outflows, heightened global policy uncertainty, and elevated hedging demand, effectively inverting the forward premia term structure. Forward premia eased significantly from December peak as liquidity conditions eased in the wake of liquidity augmenting measures by the Reserve Bank, including USD/INR buy-sell swap auctions. In March, forward premia shot up, reflecting elevated uncertainty in West Asia. On average, the 1-month forward premia hardened to 2.76 per cent in H2 from 1.95 per cent in H1. The 12-month premia increased to 2.54 per cent from 2.12 per cent during this period.

In terms of the 40-currency real effective exchange rate (REER), the INR depreciated by 3.3 per cent between September 2025 and February 2026, driven by depreciation of the INR in nominal effective terms (Chart II.19a). The depreciation of INR’s 40-currency REER was broadly in line with some major economies (Chart II.19b). Financial Conditions Overall financial conditions8 remained benign during Q3. However, with the outbreak of the West Asia crisis at end-February 2026, financial conditions tightened due to broad based hardening across the entire market spectrum (Chart II.20).

II.2.6 Bank and Non-Bank Credit Bank Credit: Aggregate Trends Bank credit recorded a robust growth during H2; 2025-26, owing to monetary policy easing and strong economic activity. Growth in bank credit of scheduled commercial banks accelerated to 13.8 per cent (y-o-y) as on March 15, 2026 from 11.0 per cent a year ago. Across bank groups, credit growth of foreign banks remained the highest at 14.7 per cent (y-o-y), followed by public sector banks and private banks (Chart II.21a). As on March 15, 2026, public sector banks accounted for the largest share of incremental credit (y-o-y). However, credit growth has accelerated for private banks in recent months leading to improvement in their share in incremental credit (Chart II.21b).

The asset quality of SCBs improved further during 2025-26 (up to December 2025), with the overall gross non-performing assets (NPA) ratio declining to 2.0 per cent in December 2025 from 2.5 per cent a year ago (Chart II.22a). Asset quality improved across all major sectors (Chart II.22b). Banks’ non statutory liquidity ratio (non-SLR) investments (comprising CPs, bonds, debentures and shares of public and private corporates) grew moderately by 2.7 per cent in H2:2025-26 (up to March 15) due to decline in commercial paper holdings (Chart II.23a). Growth in adjusted non-food credit (non-food bank credit plus banks’ non-SLR investments) increased to 13.5 per cent (y-o-y) in Q4:2025-26 (up to March 15) from 10.8 per cent in Q4:2024-25 (Chart II.23b). As on February 28, 2026, excess holdings of SLR securities by SCBs moderated to 6.3 per cent of their NDTL from 7.3 per cent at end-March 2025 as banks brought down their investment portfolio to fund credit demand (Chart II.24).

Bank Credit: A Sectoral Perspective Sectoral trends9 indicate strengthening of credit growth across major segments. Industrial credit growth remained above its long-term average, thereby supporting overall credit expansion. Although personal loans growth remained below its long-term average, it has accelerated recently (Table II.7 and Chart II.25a). Personal loans and services sector continued to drive the overall credit growth (Charts II.25a and II.25b). Within the industrial sector, credit to MSMEs10 segment remained buoyant, recording a marked acceleration and contributing significantly to overall credit growth in H2:2025-26 so far11 (Chart II.26a). The flow of credit to MSMEs was supported by regulatory measures such as the enhanced limit under the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme, introduction of customised credit card scheme for micro enterprises, expansion of digital and fintech lending through the co-lending framework with banks, and the updated definition of MSMEs, among others. | Table II.7: Credit Growth | | (Y-o-y, per cent) | | Sectors/Sub-sectors | Average* | Post-COVID** | Nov-23 | Mar-24 | Sep-24 | Dec-24 | Feb-25 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Jan-26 | Feb-26 | | Bank Credit | 11.1 | 14.8 | 20.7 | 20.2 | 13.0 | 11.2 | 11.1 | 11.0 | 9.5 | 10.4 | 14.5 | 14.6 | 14.5 | | Sectoral Deployment of Bank Credit | | Agriculture (13.0) | 11.4 | 14.2 | 18.1 | 20.0 | 16.4 | 12.5 | 11.4 | 10.4 | 6.8 | 9.0 | 12.1 | 11.4 | 12.3 | | Industry (22.7) | 4.6 | 8.6 | 6.9 | 9.4 | 10.0 | 7.5 | 7.5 | 8.2 | 6.3 | 7.8 | 12.8 | 12.1 | 13.5 | | Micro and Small (5.3) | 9.8 | 17.7 | 17.9 | 15.8 | 14.5 | 9.8 | 9.6 | 8.9 | 19.2 | 22.0 | 30.4 | 31.2 | 30.4 | | Medium (2.2) | 14.4 | 19.3 | 12.9 | 14.2 | 21.4 | 19.8 | 18.0 | 18.5 | 13.2 | 14.5 | 20.4 | 22.3 | 21.0 | | MSMEs (7.5) | 10.9 | 18.1 | 16.4 | 15.3 | 16.5 | 12.8 | 12.1 | 11.8 | 17.4 | 19.7 | 27.3 | 28.5 | 27.5 | | Large (15.2) | 2.8 | 5.3 | 3.7 | 7.2 | 7.5 | 5.5 | 5.6 | 6.9 | 2.0 | 3.0 | 6.9 | 5.5 | 7.8 | | Infrastructure (7.4) | 4.0 | 5.2 | 4.1 | 8.5 | 4.4 | 1.6 | 1.7 | 2.8 | 0.8 | 5.0 | 7.2 | 6.4 | 7.9 | | Services (29.6) | 14.1 | 17.2 | 24.5 | 22.3 | 12.4 | 11.5 | 11.7 | 12.0 | 8.8 | 9.8 | 15.4 | 15.5 | 16.3 | | Services excluding NBFCs (19.7) | 12.6 | 17.6 | 27.5 | 27.3 | 14.0 | 14.1 | 13.5 | 14.4 | 11.7 | 12.7 | 15.6 | 14.4 | 14.0 | | NBFCs (9.9) | 19.6 | 16.6 | 19.2 | 13.4 | 9.4 | 6.5 | 8.1 | 7.4 | 3.1 | 3.9 | 15.1 | 17.8 | 20.9 | | Personal Loans (34.7) | 17.7 | 19.1 | 30.4 | 27.8 | 13.8 | 12.0 | 11.7 | 11.7 | 11.7 | 11.8 | 14.6 | 14.9 | 15.2 | | Personal Loans with unchanged Risk Weight (23.6) | 17.3 | 19.2 | 32.2 | 31.5 | 13.9 | 12.9 | 13.5 | 13.5 | 13.9 | 14.1 | 17.1 | 17.5 | 17.6 | | Housing (Including Priority Sector Housing) (16.9) | 16.7 | 18.8 | 36.7 | 36.5 | 12.6 | 11.1 | 11.1 | 10.7 | 9.6 | 10.1 | 11.1 | 11.1 | 11.0 | | Vehicle Loans (3.7) | 18.0 | 15.2 | 20.6 | 17.6 | 13.9 | 8.8 | 9.6 | 8.6 | 9.2 | 7.3 | 16.7 | 17.1 | 17.1 | | Education (0.8) | 8.5 | 16.2 | 23.0 | 23.7 | 17.6 | 15.8 | 15.3 | 15.1 | 14.4 | 14.0 | 14.8 | 14.0 | 13.7 | | Personal Loans with increased Risk Weight (11.1) | 18.8 | 19.0 | 27.1 | 21.3 | 13.5 | 10.4 | 8.4 | 8.3 | 7.5 | 7.1 | 9.8 | 10.0 | 10.4 | | Credit Cards (1.5) | 24.2 | 21.2 | 34.2 | 25.6 | 18.0 | 15.6 | 11.2 | 10.6 | 7.2 | 3.7 | 1.0 | 1.5 | 1.7 | | Other Personal Loans (8.7) | 20.3 | 18.9 | 27.3 | 22.8 | 13.1 | 8.8 | 7.6 | 7.5 | 7.1 | 7.4 | 11.5 | 11.6 | 12.1 | Notes: 1. Provisional data.

2. *: Simple average of growth from March 2016 to February 2026.

3. **: Simple average of growth from April 2022 to February 2026

4. Figures in parentheses against each sector and sub-sectors denote share in total non-food credit as per the latest data.

Source: RBI. |

Among the major industrial sub-sectors, credit growth of infrastructure sector strengthened in recent months, making a significant contribution to overall industrial credit expansion. Additionally, credit growth in 'basic metal and metal product', 'chemicals and chemical products' and 'all engineering' showed sustained improvement (Chart II.26b and Table II.8).

Within the services sector, 'non-banking financial companies' (NBFCs) remained the largest recipient of bank credit, with lending to them improving following the withdrawal of the additional risk weights effective April 1, 2025 (Chart II.27). Credit to services excluding NBFCs also expanded at a steady pace. Segments such as trade and commercial real estate recorded robust growth (Chart II.27 and Table II.9).

Credit growth in the personal loans segment was driven primarily by housing loans, vehicle loans and loans against gold jewellery during H2:2025-26 (Chart II.28). Both segments of personal loans, i.e., with and without change in risk weights recorded robust growth (Table II.9). The impact of increase in risk weights has gradually moderated across major sectors and subsectors. Sustained economic growth led to increased demand for bank credit. NBFCs Credit12 Credit extended by NBFCs has also strengthened since September 2025, recording sustained double-digit growth. Retail lending continued to drive overall expansion, led by housing and vehicle loans. Industrial credit exhibited steady growth, with higher lending to infrastructure, especially power sector, underscoring the important role of NBFCs in providing formal credit to niche sectors in the economy. NBFCs credit to the services sector also expanded at a healthy pace during H2:2025–26 (up to February) (Chart II.29 and Table II.10).

| Table II.10: Sector-wise Growth in Credit by NBFCs (including HFCs) | | (Y-o-y, per cent) | | Sector | Average* | Feb-25 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Jan-26 | Feb-26 | | NBFCs Credit | 8.7 | 10.6 | 10.6 | 8.8 | 12.4 | 14.0 | 13.9 | 13.7 | | Agriculture and Allied Activities (1.3) | 13.9 | 9.0 | 6.0 | 5.1 | 5.2 | 9.4 | 10.4 | 12.6 | | Industry (38.6) | 10.9 | 9.5 | 9.7 | 10.3 | 10.2 | 9.8 | 8.9 | 8.1 | | of which | | | | | | | | | | Infrastructure (35.4) | 10.1 | 8.7 | 9.2 | 9.1 | 9.4 | 8.9 | 8.0 | 7.1 | | of which | | | | | | | | | | Power (24.9) | 12.5 | 12.3 | 12.2 | 13.3 | 11.5 | 10.1 | 9.2 | 7.8 | | Road (0.9) | 18.3 | 31.4 | 27.7 | 6.7 | 7.6 | 7.6 | 7.7 | 5.4 | | Services (12.2) | 18.8 | 13.8 | 17.4 | 14.2 | 15.8 | 19.6 | 19.4 | 18.8 | | of which | | | | | | | | | | Transport Operators (3.0) | 14.7 | 12.8 | 12.5 | 10.9 | 9.3 | 9.0 | 8.6 | 9.8 | | Trade (2.0) | 25.9 | 26.9 | 25.1 | 18.3 | 13.3 | 16.2 | 15.7 | 22.3 | | Retail Loans (42.6) | 8.7 | 13.6 | 13.1 | 11.0 | 16.6 | 18.1 | 18.7 | 19.2 | | of which | | | | | | | | | | Housing Loans (14.4)** | -5.7 | 4.2 | 4.7 | 0.4 | 9.3 | 10.7 | 10.2 | 10.0 | | Vehicle Loans (10.6) | 18.3 | 17.9 | 16.8 | 14.8 | 14.9 | 14.3 | 14.3 | 14.1 | | Loans against gold jewellery (5.3) | 27.2 | 29.0 | 32.2 | 40.6 | 50.7 | 61.2 | 68.1 | 71.9 | | Consumer Durables (1.0) | 26.1 | 25.2 | 24.0 | 18.8 | 22.2 | 23.3 | 26.4 | 28.8 | | Other Loans (5.3)*** | -10.6 | -4.8 | -8.0 | -19.5 | -4.6 | 4.2 | 4.4 | 3.5 | Notes: 1. Provisional data.

2. *: Simple average of growth from January 2023 to February 2026.

3. **:Housing loans data also include credit from Housing Finance Companies (HFCs).

4. ***:Other loans include credit from NBFCs other than agriculture, industry, services, retail loans, and non-housing loans from HFCs.

5. Data include the impact of change of nature of business of some NBFCs.

6. Figures in parenthesis represent share within total NBFCs credit.

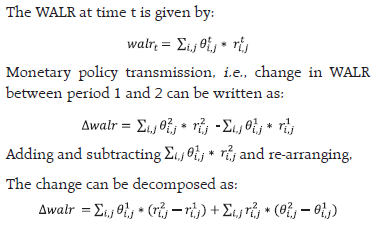

Sources: National Housing Bank (NHB); and RBI. | II.3 Transmission to Lending and Deposit Rates Transmission of the policy rate during the current easing cycle (from February 2025) continued in H2:2025-26 with softening of both lending and deposit rates. The policy rate cut of 25 bps in December 2025 led to a cumulative rate reduction of 125 basis points (bps). The median 1-year marginal cost of funds-based lending rate (MCLR) of scheduled commercial banks (SCBs) declined by 20 bps in H2. The weighted average lending rate (WALR) on fresh rupee loans increased by 5 bps during H2 (up to February 2026), mainly reflecting compositional shift in volume towards sectors attracting relatively higher interest rates, while it declined by 26 bps for outstanding loans. On the deposit side, the weighted average domestic term deposit rate (WADTDR) on outstanding deposits declined by 20 bps in H2:2025-26 (up to February 2026), while it firmed up by 4 bps for fresh deposits (Table II.11). The combination of sustained credit demand and persistent gap between credit and deposit growth led banks to increase their term deposit rates, especially bulk deposit rates, to bridge the funding gap in recent months. In the current easing cycle (up to February 2026), the WALR for outstanding loans declined by 87 bps. For fresh rupee loans, the WALR declined by 89 bps. The interest rate effect, relatively a better measure of pricing, declined by 92 bps, reflecting robust pass-through to fresh lending rates. A lower moderation in WALR vis-à-vis the interest rate effect suggests a shift in composition-mix towards higher interest rate loans across banks and across sectors (Box II.2). The share of the external benchmark-based lending rate (EBLR) linked loans in total outstanding floating rate loans of SCBs increased from 62.9 per cent as at end-June 2025 to 65.4 per cent as at end-December 2025. Consequently, the share of MCLR linked loans declined from 33.8 per cent to 32.0 per cent over the same period. Public sector banks (PSBs) still have a significant proportion of their loans linked to the MCLR (Chart II.30a). Private banks (PVBs) extend a large part of their loans linked to EBLR (Chart II.30b). The bulk of the external benchmark-based loans use policy repo rate as the benchmark. The MCLR and other legacy rates – based on internal benchmarks and having longer reset periods – impede the pace of policy transmission. | Table II.11: Transmission to Banks’ Deposit and Lending Rates | | (Basis points) | | Period | Repo Rate | Term Deposit Rates | Lending Rates | | WADTDR Fresh Deposits | WADTDR Outstanding Deposits | EBLR | 1-Yr. MCLR (Median) | WALR Fresh Rupee Loans | WALR Outstanding Rupee Loans | | Retail Deposits | Retail and Bulk Deposits | Retail and Bulk Deposits | Overall Effect | Interest Rate Effect# | | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | | Tightening Cycle May 2022 to Jan 2025 | +250 | 190 | 259 | 206 | 250 | 175 | 182 | 191 | 115 | | Easing Cycle Feb 2025 to Mar 2026* | -125 | -77 | -97 | -47 | -125 | -60 | -89 | -92 | -87 | | Memo | | H2: 2025-26* | -25 | -6 | 4 | -20 | -25 | -20 | 5 | -14 | -26 | | Dec – 2025 | -25 | -4 | 8 | -5 | -25 | -5 | -43 | -12 | -15 | | Jan – 2026 | 0 | -4 | -1 | -4 | 0 | -5 | 21 | 3 | -2 | | Feb – 2026 | 0 | -3 | -1 | -2 | 0 | 5 | -5 | -1 | -4 | Notes: 1. *: Data on WALR and WADTDR are up to February 2026. #: At constant weight.

2. Data on EBLR pertain to 32 domestic banks.

WALR: Weighted average lending rate; WADTDR: weighted average domestic term deposit rate; MCLR: Marginal cost of funds-based lending rate;

EBLR: External benchmark-based lending rate.

Sources: MPD06 return; and RBI. |