Growth in India, like in many other EMDEs, has slowed for over two years. The slowdown in

India was led by domestic structural constraints, while global cyclical conditions added to the

drag. However, as some of the structural constraints are starting to get addressed, activity levels

could improve in H2 of 2013-14 and a moderate-paced economic recovery could start taking

shape towards the end of the year. Better crop prospects due to a good monsoon, initiatives

by the government to speed up project implementation and a pick-up in exports, along with a

reduction in external imbalances has set the stage for recovery but sustained ground-level action,

especially in expediting project implementation is needed to achieve a sustainable turnaround.

Global growth likely to remain sluggish in

the near term

I.1 Global growth appears to be on a

sluggish trail despite an improvement in Q2 of

2013 . The International Monetary Fund (IMF)

in its World Economic Outlook in October 2013

revised global growth for 2013 downwards by

0.3 percentage points to 2.9 per cent. This

downward revision is on account of slower

growth in Emerging Market and Developing

Economies (EMDEs), including in China and

India. EMDEs growth projections have been

lowered by 0.5 percentage points to 4.5 per cent,

while the projections for Advanced Economies

(AEs) stays at 1.2 per cent.

I.2 Although both advanced and emerging

economies face the challenge of slower growth,

there was a distinct improvement in growth in

the major advanced economies during Q2 of

2013. In Q2 of 2013, the US GDP grew at 2.5

per cent (seasonally adjusted annualised quarter-on-quarter growth rate, q-o-q saar),

higher than 1.1 per cent in Q1 (Chart I.1a), due

mainly to growth in exports and non-residential

fixed investments on the one hand and a smaller

decrease in federal government spending on the

other. But the US shutdown for sixteen days

might get reflected in lower GDP growth in Q4

of 2013. The imminent risks to the global

economy from a possible US debt default have

been deferred with the US Government signing

a debt deal on October 17, 2013. However,

issues for the sustainability of the US recovery

going forward remained with headwinds to

investment, slack labour market conditions and

a possible rise in mortgage rates.

I.3 Japan’s economy expanded for the third

straight quarter in Q2 of 2013 at 3.8 per cent.

UK showed improvements for the second

consecutive quarter in Q2 of 2013, growing by

2.7 per cent as against 1.5 per cent in Q1. The

euro area grew by 1.1 per cent (q-o-q saar) in the second quarter of 2013, helped by stronger

growth in the two largest economies, Germany

and France.

Table I.1: Slowdown in growth has been broad-based |

Sector-wise growth rates of GDP (2004-05 prices) |

(Per cent) |

Industry |

2011-12* |

2012-13# |

2012-13 |

2013-14 |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

1. Agriculture, forestry & fishing |

3.6 |

1.9 |

2.9 |

1.7 |

1.8 |

1.4 |

2.7 |

2. Industry |

2.7 |

1.2 |

-0.2 |

0.5 |

2.3 |

2.0 |

-0.9 |

2.1 Mining & quarrying |

-0.6 |

-0.6 |

0.4 |

1.7 |

-0.7 |

-3.1 |

-2.8 |

2.2 Manufacturing |

2.7 |

1.0 |

-1.0 |

0.1 |

2.5 |

2.6 |

-1.2 |

2.3 Electricity, gas & water supply |

6.5 |

4.2 |

6.2 |

3.2 |

4.5 |

2.8 |

3.7 |

3. Services |

7.9 |

6.8 |

7.6 |

7.1 |

6.2 |

6.3 |

6.2 |

3.1 Trade, hotels, transport & communication |

7.0 |

6.4 |

6.1 |

6.8 |

6.4 |

6.2 |

3.9 |

3.2 Financing, insurance, real estate and business services |

11.7 |

8.6 |

9.3 |

8.3 |

7.8 |

9.1 |

8.9 |

3.3 Community, social & personal services |

6.0 |

6.6 |

8.9 |

8.4 |

5.6 |

4.0 |

9.4 |

3.4 Construction |

5.6 |

4.3 |

7.0 |

3.1 |

2.9 |

4.4 |

2.8 |

4. GDP at factor cost |

6.2 |

5.0 |

5.4 |

5.2 |

4.7 |

4.8 |

4.4 |

*: First Revised Estimates. #: Provisional Estimates.

Source: Central Statistics Office (CSO) |

I.4 Among the EMDEs, China’s GDP in

Q3 of 2013 went up by 9.1 per cent (q-o-q saar)

as compared to 7.8 per cent in Q2 and 6.1 per

cent in Q1. Brazil’s GDP growth at 6.0 per cent

(q-o-q saar) for Q2 of 2013 turned out to be

better than expected (Chart I.1b). With the Fed

tapering plans getting delayed, the EMDEs

need to prepare themselves in the interim for

the challenges that may arise.

I.5 The US labour market conditions still

remain weak with unemployment rate dropped

to 7.2 per cent in September 2013, though

additional non-farm payroll employment at

148,000 was also weak. UK labour markets

witnessed unemployment rate of 7.7 per cent

during June-August, down by 0.1 percentage

points from March-May 2013. In case of Japan,

the unemployment rate increased to 4.1 per cent

in August 2013 from 3.8 per cent in July 2013.

The unemployment rate in the euro area also

remained high and unchanged at 12.0 per cent

in August 2013.

The Indian economy faced broad-based

slowdown during Q1 of 2013-14

I.6 The slowdown facing the Indian

economy extended into 2013-14 with growth in

Q1 of 2013-14 falling to a 17- quarter low of

4.4 per cent (Table I.1). The growth slowdown

was broad-based reflecting moderation in the

services and agricultural sectors, and contraction

in the industrial sector.

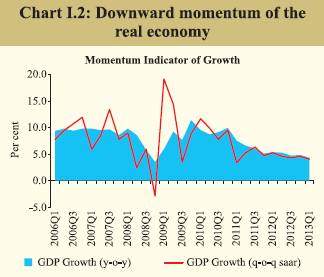

I.7 Since H2 of 2011-12, the seasonally

adjusted annualised q-o-q saar growth rate has

moved in line with declining trends in the year-on-

year (y-o-y) GDP growth rate, confirming

the downward momentum in the real economy

(Chart I.2). The output gap also continued to be

negative (Chart I.3). Supply constraints, high

inflation, cyclical factors and low external

demand contributed to this slowdown.

Agriculture growth expected to be buoyant

I.8 Agricultural production during 2013-14

is expected to record an above-trend growth

(Table I.2). The first advance estimates of

production of foodgrains have placed kharif

foodgrains at 129.3 million tonnes, a 10.3 per cent jump over the first advance estimates of

the previous year and 0.9 per cent growth over

the fourth advance estimate. Oilseeds too are

expected to show a substantial increase.

I.9 A normal and evenly distributed southwest

monsoon reinforced the possibility of a

good crop. Rainfall during June-September

2013 was 6 per cent above normal. Thirty out

of the 36 meteorological sub-divisions that

constitute 86 per cent of the country’s area

received normal or excess rainfall. Deficiency

in rainfall was limited to areas in the East and

North-East and in Haryana. Prospects for rabi

crops are also good with water storage in the

85 major reservoirs as of October 17, 2013

being 16.3 per cent higher than last year’s level. The Reserve Bank’s production weighted

rainfall index for foodgrains for the period

stood at 102 per cent of the normal as compared

to 87 per cent last year (Chart I.4). The same

index for oilseeds (125), sugarcane (109) and

cotton (126) was also higher. An improved

kharif harvest is expected to help ease food

price pressure.

I.10 The current stock of rice and wheat at

53 million tonnes (mid-October 2013) is

sufficient to meet buffer norms and requirements

under the various poverty alleviation schemes

(Chart I.5). These stocks can be utilised better

in the short-run for price management keeping

in view storage constraints that may emerge

following another bumper crop. However, over

the medium-term a reassessment of the food

management strategy may be required keeping

in view the expected higher off-take with the

phased implementation of the National Food

Security Act at the all-India level.

Industrial activity continues to be

constrained by supply bottlenecks

I.11 The index of industrial production (IIP)

for April-August 2013 grew marginally by 0.1

per cent. Contraction of the mining and

manufacturing sectors has been the main factor

in dampening the overall performance of

industrial growth. Excluding capital goods and

the mining sector, IIP grew by 0.5 per cent during the period (Chart I.6). Excluding volatile

items such as ‘cable, rubber insulated’, ‘atrazin’,

‘vitamins’, ‘food processing machinery’, etc.

truncated IIP (96 per cent of IIP) growth in

April-August 2013 was negative at 0.9 per cent

(Chart I.7).

Table I.2: Initial estimates suggest jump in Kharif production |

Progress of Kharif sowing and production |

(Area in million hectares and production in million tonnes) |

Crops |

Sowing October 25 |

Production |

Percentage Change |

Normal

as on

Date |

2013 |

2012 |

2013-14* |

2012-13* |

2012-13@ |

Sowing

2013

(col 3/col 4) |

Production

2013-14

(col 5/col 6) |

Production

2013-14

(col 5/col 7) |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

Foodgrains |

67.6 |

68.7 |

65.6 |

129.3 |

117.2 |

128.2 |

4.7 |

10.3 |

0.9 |

Rice |

36.6 |

38.4 |

37.5 |

92.3 |

85.6 |

92.8 |

2.4 |

7.8 |

-0.5 |

Coarse Cereals |

20.1 |

19.6 |

17.8 |

31.0 |

26.3 |

29.5 |

10.1 |

17.9 |

5.1 |

Maize |

7.3 |

8.2 |

7.5 |

17.8 |

14.9 |

16.0 |

9.3 |

19.5 |

11.3 |

Pulses |

10.9 |

10.7 |

10.3 |

6.0 |

5.3 |

5.9 |

3.9 |

13.2 |

1.7 |

Tur |

3.8 |

4.0 |

3.7 |

3.0 |

2.8 |

3.1 |

8.1 |

7.1 |

-3.2 |

Urad |

2.4 |

2.6 |

2.5 |

1.3 |

1.1 |

1.4 |

4.0 |

18.2 |

-7.1 |

Oilseeds |

17.8 |

19.5 |

17.7 |

24.0 |

18.8 |

20.9 |

10.2 |

27.7 |

14.8 |

Groundnut |

4.6 |

4.3 |

3.9 |

5.6 |

3.8 |

3.1 |

10.3 |

47.4 |

80.6 |

Soyabean |

9.5 |

12.2 |

10.7 |

15.7 |

12.6 |

14.7 |

14.0 |

24.6 |

6.8 |

Sugarcane |

4.7 |

4.9 |

5.0 |

341.8 |

335.3 |

339.0 |

-2.0 |

1.9 |

0.8 |

Cotton# |

11.6 |

11.5 |

11.7 |

35.3 |

33.4 |

34.0 |

-1.7 |

5.7 |

3.8 |

Jute & Mesta## |

0.9 |

0.9 |

0.9 |

11.2 |

11.3 |

11.3 |

0.0 |

-0.9 |

-0.9 |

All Crops |

102.5 |

105.5 |

100.9 |

- |

- |

- |

4.6 |

- |

- |

#: Million bales of 170 kgs each. ##: Million bales of 180 kgs each. -: Not Available.

*: First Advance Estimates. @: Fourth Advance Estimates

Source: Ministry of Agriculture, GoI. |

I.12 While the mining sector has been

declining since 2011-12, the contraction in the manufacturing sector during April-August 2013

was driven primarily by declining outputs of

industries like machinery and equipments;

accounting and computing machinery; basic

metals; fabricated metal products; radio, TV,

communication equipments; and motor vehicles.

The decline in the mining sector’s output,

particularly coal, affected thermal power

generation which decelerated to 1.8 per cent

during April-August 2013 from 8.6 per cent last

year. However, hydro-electricity generation is

expected to be distinctly better this year with

the replenishment of water in reservoirs. Hydropower

has grown by 20.2 per cent y-o-y during

April-August 2013.

I.13 In terms of use-based industries,

consumer durables and basic goods, which

together have a 54 per cent weight in IIP,

dragged its overall growth down (Table I.3).

Core industries show some improvement

over last two months

I.14 Output of eight core industries improved

consecutively for two months with a 3.7 per cent

y-o-y growth in August 2013. The latest data shows a pick-up in core industries’ output led

by steel, cement and electricity. However, on a

year-to-date (YTD) basis, the growth of eight

core industries decelerated to 2.3 per cent during

April-August 2013 from 6.3 per cent in the

corresponding period last year (Chart I.8). The

deceleration in thermal electricity during April-

August 2013 was reflected in a reduction in the

all-India plant load factor (PLF) to 64.1 per cent

from 69.8 per cent last year.

Table I.3: Broad-based industrial

slowdown led by contraction in

consumer durables |

Sectoral and use-based classification of IIP |

(Per cent) |

Industry Group |

Weight

in the

IIP |

Growth Rate |

Apr-

Mar

2012-13 |

April-August |

2012-13 |

2013-14P |

1 |

2 |

3 |

4 |

5 |

Sectoral |

|

|

|

|

Mining |

14.2 |

-2.3 |

-1.8 |

-3.4 |

Manufacturing |

75.5 |

1.3 |

0.0 |

-0.1 |

Electricity |

10.3 |

4.0 |

4.8 |

4.5 |

Use-Based |

|

|

|

|

Basic Goods |

45.7 |

2.5 |

2.7 |

0.5 |

Capital Goods |

8.8 |

-6.0 |

-14.4 |

0.8 |

Intermediate Goods |

15.7 |

1.6 |

1.0 |

2.3 |

Consumer Goods (a+b) |

29.8 |

2.4 |

3.2 |

-1.6 |

a) Consumer Durables |

8.5 |

2.0 |

5.1 |

-11.0 |

b) Consumer Non-durables |

21.3 |

2.8 |

1.6 |

6.6 |

General |

100 |

1.1 |

0.2 |

0.1 |

P: Provisional

Source: Central Statistics Office. |

Moderation in Capacity Utilisation

I.15 Capacity utilisation (CU), as measured

by the 22nd round of the Order Books, Inventories

and Capacity Utilisation Survey (OBICUS) of

the Reserve Bank, recorded seasonal decline in

Q1 of 2013-14 over the previous quarter (http://

www.rbi.org.in/OBICUS22). There is a broad

co-movement between CU and de-trended

Index of Industrial Production (IIP) (Chart I.9).

After a sequential increase in the previous two

quarters, new orders declined in Q1 of 2013-14

both on a q-o-q sequential basis as well as on a

y-o-y basis. Finished goods inventory to sales

and raw material inventory to sales ratios

increased in Q1 of 2013-14 and were higher

than the previous year.

Lead indicators portray a mixed picture on

service sector growth

I.16 The services sector grew at 6.2 per cent

during Q1 of 2013-14 compared to 7.6 per cent

during the same period last year. This was largely due to moderation in the growth of

‘construction’ and ‘trade, hotels, restaurant,

transport and communication’ sectors.

Developments in lead indicators of the services

sector portray a mixed picture. Passenger and

commercial vehicles sales and some segments

of the aviation industry contracted even though

indicators like tourist arrivals, railway freight

revenue and steel production showed signs of

improvement (Table I.4). The Reserve Bank’s

services sector composite indicator, which is

based on growth in indicators of construction,

trade and transport and finance, showed a downturn in Q1 of 2013-14, but a modest pickup

in July-August (Chart I.10).

Table I.4: Lead indicators point towards subdued services sector activity |

Indicators of services sector activity |

(Growth in per cent) |

Services Sector Indicators |

2010-11 |

2011-12 |

2012-13 |

April-September 2012-13 |

April-September 2013-14 |

1 |

2 |

3 |

4 |

5 |

6 |

Tourist arrivals |

10.0 |

9.7 |

2.1 |

1.7 |

4.3 |

Cement |

4.5 |

6.7 |

8.4 |

8.3# |

3.2# |

Steel |

13.2 |

10.3 |

2.5 |

2.8# |

4.1# |

Automobile Sales |

16.8 |

11.1 |

2.6 |

3.5 |

1.2 |

Railway revenue earning freight traffic |

3.8 |

5.2 |

4.1 |

4.8 |

6.2 |

Cargo handled at major ports |

1.5 |

-1.6 |

-2.5 |

-3.3 |

2.3 |

Civil aviation |

|

|

|

|

|

Domestic cargo Traffic |

23.8 |

-4.8 |

-3.4 |

3.8* |

-3.0* |

International cargo Traffic |

17.7 |

-1.9 |

-4.2 |

-4.2* |

-1.7* |

International Passenger Traffic |

10.3 |

7.6 |

5.5 |

3.2* |

11.0* |

Domestic Passenger Traffic |

18.1 |

15.1 |

-4.3 |

-0.8* |

2.3* |

#: Data refers to April-August 2013; *: Data refers to April-July 2013.

Source: Ministry of Statistics and Programme Implementation, Ministry of Tourism, SIAM and CMIE |

Employment Scenario remains weak in

Q1 of 2013-14

I.17 As per the Labour Bureau survey in

eight key sectors, moderation in employment

generation that started in 2012 continued in Q1

of 2013-14 (Chart I.11). The decline in

employment generation was particularly sharp

for the IT/BPO sector, reflecting the global

slowdown and rising protectionism. Sector-wise,

except textiles and leather, no other sector

showed any perceptible improvement in

employment generation during Q1 of 2013 on

a sequential basis.

Moderate recovery expected during H2

mainly backed by pick-up in agriculture

and exports

I.18 The Indian economy is expected to

perform better during H2 of 2013-14 on the back of a good monsoon which has boosted the kharif

prospects. A good crop will have a positive

impact on rural demand, which in turn may help

in improving the subdued industrial and services

sectors. Further, improved kharif harvest is also

expected to help ease supply-side constraints

and hence food price pressure. Exports have

picked up with exchange rate adjustment though

global growth remains slow. On the policy front,

the government has started taking several policy

initiatives in certain sectors, especially

infrastructure, which are expected to improve

the overall investment climate. However, these

actions will take some time to translate into

activity at the ground-level. Therefore,

improvements in activity levels during H2 of

2013-14 are expected to stay modest though

recovery could start shaping towards the end of

the year if the current positive momentum is

sustained.

|